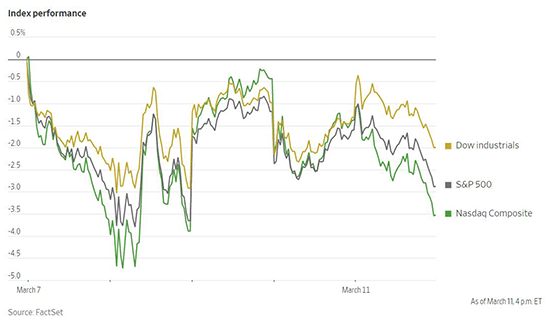

Market turbulence continued last week as US stocks swung between large gains and losses day to day before falling to end the week. The Dow Jones Industrial Average lost 2%, marking its fifth consecutive week of losses, while the S&P 500 fell 2.9% and the Nasdaq Composite dropped 3.5%. That marks the fourth week of losses over the past five weeks for both. The Nasdaq Composite moved into bear market territory on Monday, defined as a drawdown of 20% from its prior high. Losses have been broad-based across most sectors year to date, with energy being the only sector to record a gain so far this year. Trading was choppy in the bond market as well, with the yield on the 10-Year US Treasury note erasing the prior week’s fall and ending the week up near 2%. Commodity prices also saw dramatic whipsaws with oil, nickel, wheat, and others all witnessing double-digit moves over the week.

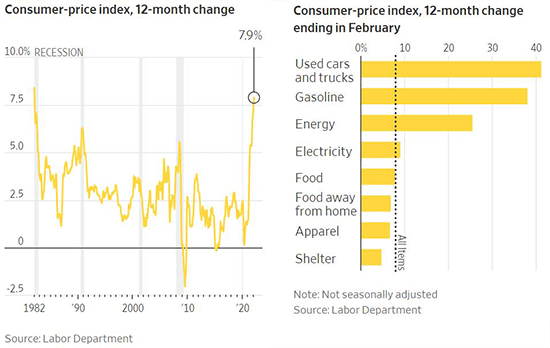

The US Consumer Price Index continued to accelerate to 7.9% in February, reaching the fastest rate of inflation since 1982. The decision by the US and UK to ban imports of Russian oil will further pressure tight energy markets and stoke inflation. Oil briefly traded as high as $139 per barrel before falling back near $110 after the United Arab Emirates announced it was in favor of producing more oil. The national average price for regular gasoline hit $4.173 per gallon last week, beating the previous record high set in 2008. While energy prices were a major factor in the February inflation figure, price pressures are increasingly broad-based. Excluding volatile food and energy prices, the core Consumer Price Index rose 6.4% in February, an increase from the 6% annual rate reported in January. The Federal Reserve meets on Tuesday and Wednesday this week to vote on whether to raise interest rates to control inflation. Fed-funds futures currently imply a 96% probability of a 0.25 percentage point rate hike.

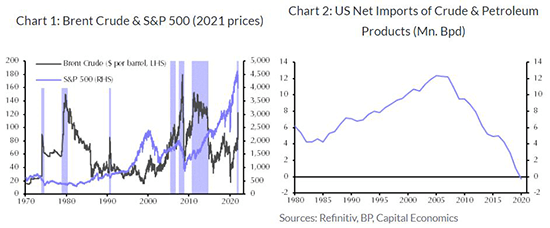

The current surge in oil prices may be concerning for investors who draw parallels with the oil price shock of 1973 to 1974. During that time, US support for Israel in the Yom Kippur War resulted in an embargo by the Organization of Petroleum Exporting Countries on oil exports to the US. Oil prices spiked to a dramatic degree and the S&P 500 fell roughly 45% from peak to trough in the following drawdown. However, there are important differences between that period and the current economic environment. During that period, markets were also grappling with the collapse of the Bretton Woods monetary system, an aggressive tightening cycle from the US Federal Reserve, and a recession in the US. Today the US economy is growing strongly and is 70% less oil intensive relative to 1965. The US is also currently roughly balanced between the production and consumption of oil and petroleum products, meaning that the economic impact from lower consumer demand may be partially offset by higher oil production revenues. These factors together make a recession induced by high oil prices less likely. Other oil price shocks such as in 1979 and 1990 did not witness plunges in US equities either. Though high oil prices may have a small negative impact on the US economy this year, it is unlikely that oil alone would precipitate a crash in US equities similar to 1973.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1584