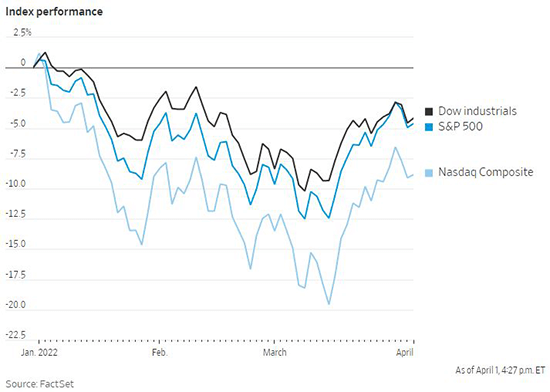

Though US stocks staged a respectable recovery over the second half of March, several major equity indexes suffered their worst performance in two years over the first quarter of 2022. The Dow Jones Industrial Average ended the quarter with a loss of 4.6% while the S&P 500 fell 4.9%. The technology-heavy Nasdaq Composite at one point fell into a bear market with a loss greater than 20% before rebounding to end the quarter with a 9.1% loss. Several of the technology giants including Facebook parent Meta and Netflix suffered substantial losses. The hawkish turn by the US Federal Reserve in the face of surging inflation meant that bonds did not offer refuge, either. The Bloomberg US Aggregate Bond Index, which is largely made up of US government bonds, investment-grade corporate bonds and mortgage-backed securities, fell 6% over the first quarter. Assets that benefitted from surging commodity prices were some of the few seeing positive returns to start the year. The Bloomberg Commodity Index gained 25% in the first quarter while the S&P 500 energy sector gained 38%, its best quarter in history.

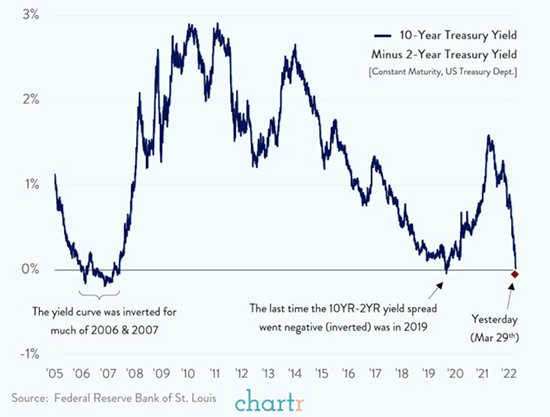

The spread in yields between the 2-Year and 10-Year US Treasury notes is closely watched by market participants. Typically, the yield on the 10-Year is greater than the 2-Year, but at times this relationship flips and the yield curve is said to be inverted. That occurrence is notable as every US recession in the last 50 years has been preceded by an inversion of the yield curve. However, not every yield curve inversion has been followed by a recession, making it an important but imperfect indicator. The yield curve flattened significantly this year and finally inverted briefly on March 29 before inverting again on Friday. However, it is important to note that the current inversion is being driven by short yields rising faster than long yields. It would be more alarming if long yields were falling, which would indicate investors are positioning for slower economic growth. A plausible argument can also be made that the Fed’s massive purchases of fixed-income instruments through quantitative easing have artificially suppressed long-term yields as well. In the absence of that quantitative easing it is possible the yield curve would not be inverted currently by some analysts’ calculations. The March payrolls report showed employers added 431,000 jobs last month, indicating continued strength in the labor market. The unemployment rate fell to 3.6%, just shy of the 50-year low of 3.5% from prior to the pandemic. Though it would be unwise to disregard the inversion of the yield curve altogether, it is unlikely that a recession is imminent given the current environment.

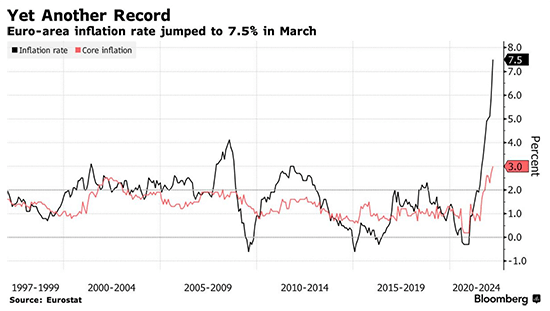

Inflation in the Eurozone surged to a new record high in March. The median estimate in a Bloomberg survey was for an acceleration to 6.7% from February’s 5.9% rate, but figures released Friday showed a material overshoot to a 7.5% increase in the Consumer Price Index. Threats from Russia to turn off natural gas supplies to countries who refuse to purchase in Russian rubles once again jarred energy markets. Energy was the dominant contributor to the higher inflation rate with a 44.7% rise. However, even after excluding volatile food and energy prices, the core inflation rate also reached a new record high of 3%. The Purchasing Managers’ Index produced by S&P Global showed that producer prices hit a four-month high due to rising commodity and energy costs. This is unwelcome news for the region, as the United Nations Conference on Trade and Development halved its growth forecast for Europe to 1.7%. The European Central Bank also cut its growth forecast for the Eurozone to 3.7% from 4.2%. However, they estimate that if the flow of Russian gas was cut off, growth could slow to the range of 2.5% to 3.3% for the year. The ECB now sits in the uncomfortable position of beginning to remove accommodative monetary policy to combat inflation even as threats to regional economic growth build.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1637