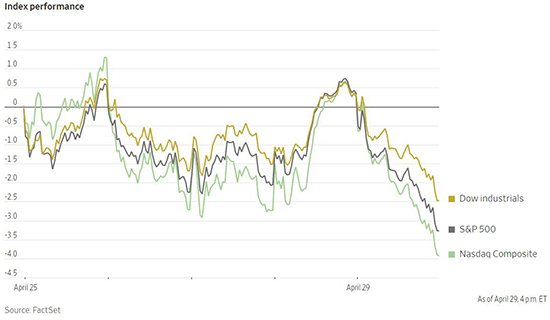

A volatile week of equity trading during this mixed earnings season turned decisively negative on Friday. The Dow Jones Industrial Average ended down 2.5% for the week while the S&P 500 fell 3.3%. The Russell 2000 and Nasdaq Composite both had more severe losses of 3.9% each for the week. The Nasdaq fell more than 13% in April in its worst monthly showing since October 2008. The S&P 500 has now fallen for four consecutive weeks and ended April with losses of 8.8%. Investors have broadly sold off growth and technology stocks in a striking departure from recent years. The mega-cap tech stocks that make up the FAANGs collectively lost more than $1 trillion in market value in April alone as markets moved to factor higher interest rates into stock valuations. The yield on the 10-Year US Treasury note ended the month at 2.885%. This constitutes the most rapid monthly gain in yields since December 2009.

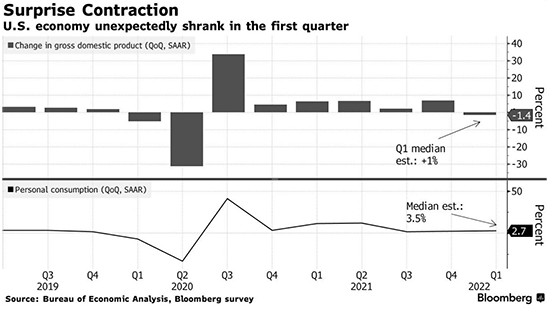

New data released by the US Commerce Department showed that the US economy shrunk by 1.4% at an annualized rate in the first quarter of 2022. This was well shy of the median estimate of 1% growth in a Bloomberg survey of economists. However, this contraction was due almost entirely to a widening in the trade deficit as booming demand for imports outpaced slowing exports. Net exports decreased the GDP figure for the quarter by an annualized 3.2%. Businesses slowed investment in inventories in a natural response to a rapid buildup carried out in the final quarter of last year, which decreased GDP by 0.84% as well. Personal consumption expanded at a 2.7% annualized rate for the first quarter, in an acceleration from the fourth quarter. This accounts for the largest part of the economy and shows continued momentum based on the healthy labor market. In fact, employers increased spending on workers by 4.5% in the first quarter compared to a year ago in the fastest expansion in wages and benefits since 2001. Despite the negative surprise in headline GDP, the consensus among forecasters is for the economy to continue growing in the second quarter of the year and beyond.

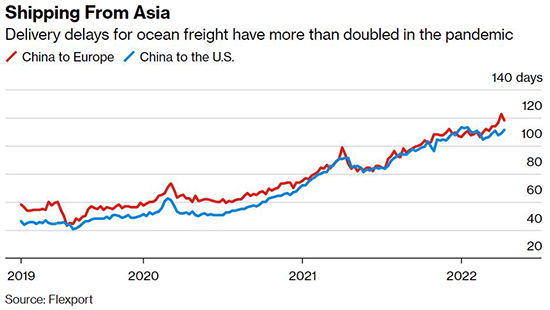

Meanwhile, GDP figures released by the National Bureau of Statistics in China last week showed that the economy grew by an annualized 4.8% in the first quarter. However, that seemingly benign figure does not account for the impact of the stringent lockdowns that were enacted to halt the spread of the Omicron variant of COVID-19 at the tail end of the quarter. The unemployment rate rose by 0.3% to 5.8% in March. Retail sales also dropped more severely than feared last month in an ominous sign for consumer spending. The government policy response has so far been restrained with only limited monetary and fiscal accommodation. The International Monetary Fund cut its growth forecast for China this year to 4.4% and many others are also downgrading projections. The Shanghai Composite and CSI 300 indexes fell by 5.1% and 4.9%, respectively, on April 25 in their worst single-day performance since February 2020. The lockdown of the manufacturing hub and port of Shanghai will also add additional pressure to already strained global supply chains. Shipping delays from Asia to Europe and the US are still hovering near all-time highs.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1705