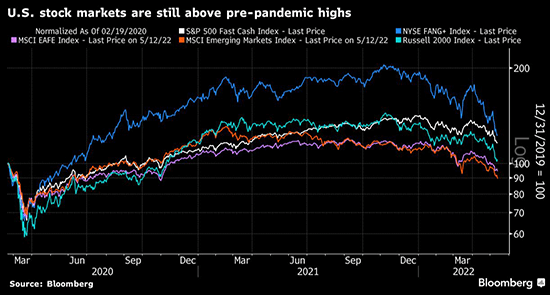

Beleaguered stock indexes finally rallied on Friday after falling through Thursday, limiting losses for the week. The Nasdaq Composite rallied 3.8% on Friday alone, trimming losses to 2.8% for the week. The Dow Industrial Average fell 2.1%, marking its seventh straight weekly loss and its longest losing streak since 2001. The S&P 500 had fallen 19.92% from its prior peak at one point on Thursday, just shy of the psychologically significant marker of a 20% fall that denotes a bear market. The 2.4% rally for the S&P 500 on Friday cut losses for the week to 2.4%. Though a 20% decline would technically indicate a bear market, there is nothing particularly meaningful about that indicator. Even after the selloff this year, US stocks remain above their highs from prior to the pandemic.

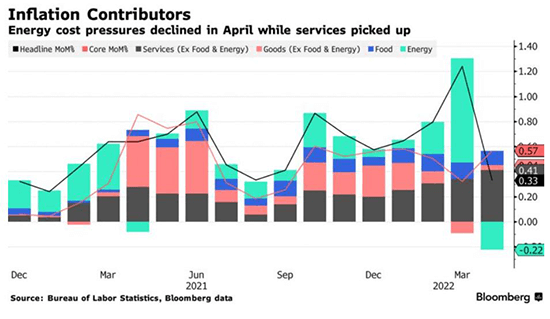

The US Labor Department’s Consumer Price Index (CPI) data last week for the month of April indicated that the headline inflation rate cooled slightly to an 8.3% annual rate, down slightly from its 40-year peak of 8.5% in March. The first decline in headline inflation in eight months was mostly attributed to an easing of gasoline prices as crude oil remains rangebound. The core CPI, which strips out volatile food and energy prices, rose at an annual rate of 6.2%. However, when comparing the figures to the prior month, core CPI rose 0.6%. This was well ahead of both Bloomberg’s median projection of 0.4% and greater than headline month-on-month figures of 0.3%. This is a worrying sign that inflation is broadening from goods inflation related to supply chains to more persistent factors. Services prices excluding energy rose 0.7% in April relative to March, marking the most rapid one-month increase for services since 1990. Housing costs account for nearly one-third of CPI and rose 4.8% from a year ago, a rate not seen in decades. Meanwhile, the Producer Price Index rose at an annual rate of 11% in April, also moderating slightly from the March rate of 11.5%. The University of Michigan survey of US consumer sentiment unexpectedly declined in the wake of the inflation report to its lowest level since 2011.

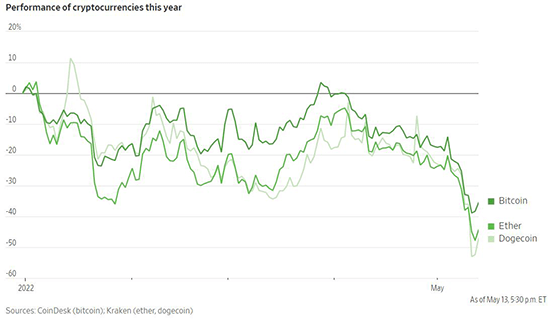

Cryptocurrencies have been treated by investors more like a risk asset than a diversifier this year. The 40-day correlation of Bitcoin with the Nasdaq 100 index of technology stocks has risen to 0.82 recently, near an all-time high. As technology stocks have come under pressure from rising interest rates, cryptocurrencies have sold off alongside them. Last week, cryptocurrencies endured an intense bout of selling due to issues related to the major stablecoin TerraUSD. Stablecoins are designed to maintain a fixed rate of exchange in contrast to other cryptocurrencies, and are a key part of the infrastructure to facilitate transactions. The algorithmic stablecoin TerraUSD was intended to maintain a peg of $1 USD via a mechanism with its sister token Luna. However, that peg broke down last week, with TerraUSD falling to as low as 10 cents Friday before recovering to roughly 14 cents. Luna tumbled by 99% from $60 on Monday to less than half a cent by the end of the week. The unravelling sent ripple effects through crypto markets, with the largest stablecoin Tether also being dragged down briefly by spreading fear before stabilizing. Bitcoin and Ether both recovered on Friday but remain down 13% and 20%, respectively, over the last five business days.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1739