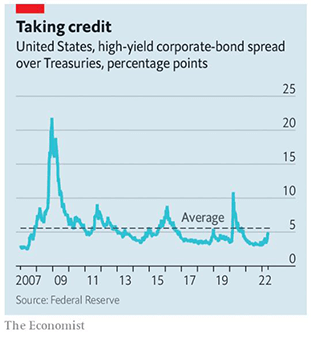

Despite the broad sell-off in the bond markets this year, the fundamentals of corporate credit markets remain sound. Their current state can generally be characterized as a return to normal conditions following a period of extraordinary government support. The credit spread of US high-yield bonds relative to risk-free US Treasury bonds has risen from 3% to around 5% since December, but still remains below its long-term average. The credit spread is still far smaller than its spike in the spring of 2020 or during the Great Financial Crisis of 2008. In addition, only 4.5% of US high-yield borrowers will need to repay their debt before 2024, meaning that pressure from higher interest rates will remain limited. Credit rating agency Moody’s estimates that the global default rate will rise to 3% over the next 12 months. That is higher than the 1.9% default rate experienced over the prior year through April, but still below the historical average of 4.1%. The most recent monthly survey by the National Association of Credit Management showed that financial conditions in April were tighter than those in late 2021, but overall remained looser than any other period going back to 2004.

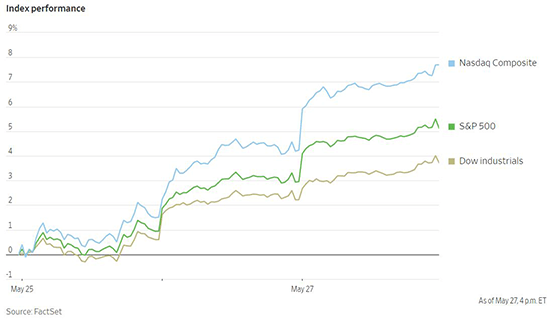

US stocks enjoyed a reprieve last week from continued selling pressure. The Dow Jones Industrial Average finally snapped what had been eight weeks in a row of losses while the S&P 500 ended seven weeks of losses. Global equity funds received around $21 billion in flows in the week to Wednesday as investors returned to buy the dip, the largest inflows to equities in 10 weeks. In another welcome development, the US Federal Reserve’s preferred gauge of inflation, the personal-consumption expenditures price index, eased slightly to 6.3% in April from 6.6% in the prior month. The yield on the 10-Year US Treasury note fell Friday to 2.741% as investors weigh concerns about inflation against worries over economic growth. Inflation breakevens, which are inflation expectations implied by bond markets, have also eased significantly in recent weeks. The US dollar also weakened relative to a basket of 16 other currencies, pausing its relentless strengthening trend this year. Though this reversal in sentiment may bring relief, there is always the risk that this rally could be a short-term pause in a longer down trend. Global fund managers remain cautious and have increased their cash allocations to the highest level since September 11, 2001.

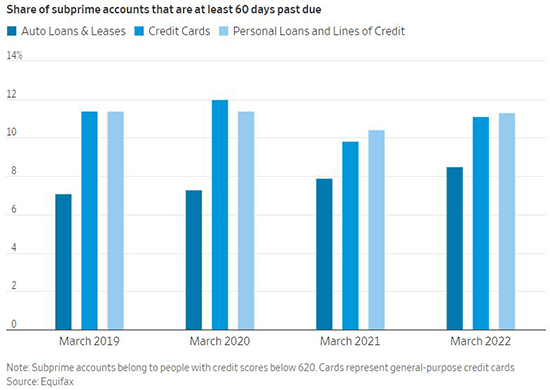

Consumer spending rose again last month by 0.9%, rising for the fourth straight month in an indication that US consumers remain healthy. However, the saving rate fell to 4.4% from 5% in March, touching its lowest rate in 14 years. Still, U.S. Bank reported that higher-income consumers in particular still have significant excess savings from which they can continue to draw to maintain spending. An analysis of consumers with low credit scores shows the first signs of stress with rising inflation. Consumers with low credit scores are falling behind on payments on credit cards and car loans. Delinquencies on subprime car loans and leases in February hit the highest level since 2007. Despite this relative deterioration in the riskiest segment of consumer credit, many lenders are referring to this increase in subprime delinquency rates as an inevitable return to normal conditions after government support artificially created the healthiest consumer lending environment on record. Some lenders have even stated that their loan delinquency rates remain below their level from the first quarter of 2020. Fewer Americans are considered subprime now than before the pandemic began. Last year, just 15.5% of US adults had credit scores lower than 600, while that figure was 18.6% in 2020. It is also important to note that mortgage lenders have kept relatively strict lending standards and there is currently little stress in the subprime mortgage market.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1770