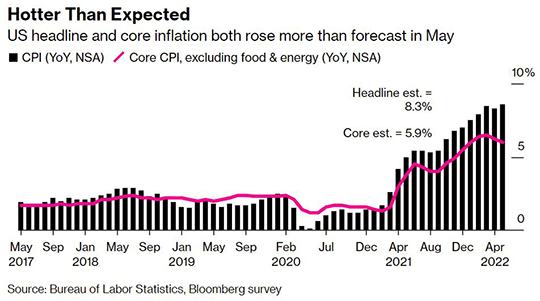

US consumer inflation accelerated again in May to an annual rate of 8.6%, once again setting a new record for the highest in the past four decades. This surpassed most economists’ expectations and dashed initial hopes that inflation had peaked after slowing slightly in April. The increase in the Consumer Price Index last month was driven largely by a 34.6% increase in energy compared to a year earlier and an 11.9% increase in the price of groceries. The increase in energy prices was the largest since 2005 while the rise in groceries was the most since 1979. Rent was also a large contributor to services inflation with an annual increase of 5.2%, the largest annual increase since 1987. Core CPI, which excludes volatile food and energy prices, rose at an annual rate of 6%, matching the rate of the prior month. Though the inflation overshoot was an unwelcome surprise, there are other indicators that suggest inflation may still ease in the second half of the year. One key indicator that has pressured supply chains is the price of semiconductors used in electronics. A futures contract measuring the price of semiconductors is down 14% from the middle of last year. The spot rate for shipping containers has also declined 26% from its high of last fall. North American fertilizer prices are also down 24% from their record high in March, which should help ease food prices. Though an improvement in supply chain bottlenecks should ease inflation pressures eventually, consumer prices are likely to remain above central bank targets for many months to come.

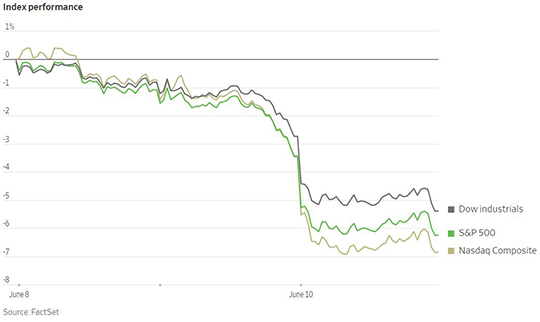

Markets sold off violently on Friday due to concerns that the US Federal Reserve may be forced to act more aggressively to reign in stubbornly high inflation, which would increase the risk of tipping the US economy into a recession. The Nasdaq Composite ended the week with a loss of 5.6% while the S&P 500 was down 5.1%. The selling was broad based, with all 11 sectors in the S&P 500 seeing losses for the week. Energy held up the best with a decline of 0.9%, with WTI crude oil futures reaching as high as $123.18 last week. Consumer staples also held up relatively well with a decline of 2.6%. Financials, information technology, real estate, and consumer discretionary all suffered weekly losses greater than 6%. Investors also sold bonds, with the yield on the two-year US Treasury note reaching 3.047%, its highest level in more than a decade. The market had previously priced in hikes of 50 basis points in June and July, but quickly moved to price in another 50-basis-point increase in September. The yield on the 10-year US Treasury note rose for the week as well and now stands at 3.16%.

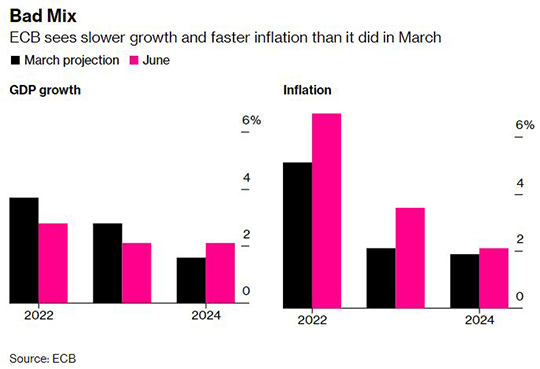

The European Central Bank communicated plans last week to raise its key policy interest rate by 25 basis points in its upcoming meeting in July. This will mark the first interest rate hike in the Eurozone in more than a decade, where the deposit rate is currently -0.5%. ECB President Christine Lagarde also indicated that a 50-basis-point rate hike is likely for September. The ECB has been slower to respond to inflation than central banks in other countries such as the US. That in part reflects the fact that the European economy is not running as hot as the US, which was boosted by more expansive fiscal stimulus throughout the pandemic. Wages are currently rising roughly twice as fast in the US compared to Europe and the unemployment rate remains higher in Europe. Headline inflation in the Eurozone hit a record of 8.1% in May, though much of the increase in consumer prices can be attributed to soaring energy costs due to sanctions enforced on Russia. Excluding volatile food and energy prices, core inflation rose 3.8% last month. That is a significantly lower core inflation rate than the 6% in the US but is still well above the target rate of 2%. The ECB also announced it would end its program of bond purchases on July 1, though it stopped short of announcing any plans to follow the US Federal Reserve and begin selling assets from its balance sheet. Traders adjusted to the announcement and markets now imply 150 basis points in interest rate increases in Europe by December. The ECB faces a difficult balancing act moving forward as the growth outlook weakens while inflation forecasts for the region are increasing.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1795