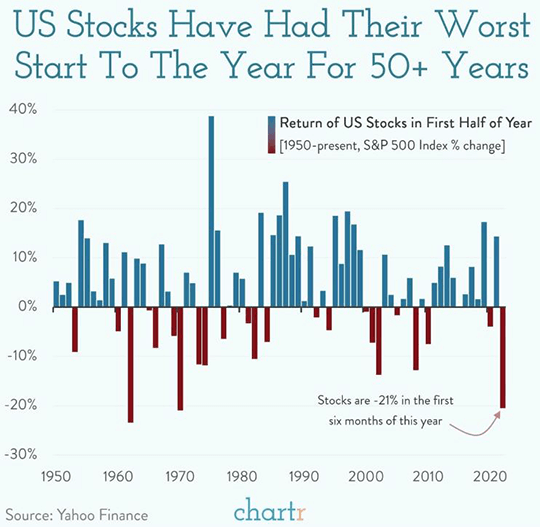

The first half of 2022 will go down as a historically difficult period for US equities. The S&P 500 fell 20.6% to start the year, making this the worst first half of a year for that index in 52 years. This is of course a completely arbitrary time period however, with no predictive power for what will occur during the second half of the year. In fact, historical data shows that of the 23 times that US equities fell in the first half of the year, they rose during the second half of the year 12 times, or roughly 50% of the time. The third quarter of the year started off with a reprieve for equity investors. The S&P 500 rose 1.9% for the week while the Dow Jones Industrial Average gained 0.8%. The Nasdaq Composite gained 4.6% last week as investors sought out discounted shares among technology companies. US short selling rose by $20 billion in June, a significant decrease compared to the $61 billion in equities shorted in May. The smaller increase in short selling last month suggests relatively fewer investors now expect equity shares to fall further from their current level.

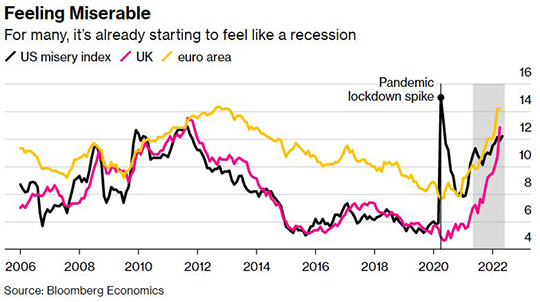

Fears are growing that the US may enter a recession as the Federal Reserve raises interest rates to combat high inflation. S&P Global Market Intelligence estimates US GDP contracted by an annual rate of 1.5% in the second quarter, while the Federal Reserve Bank of Atlanta GDPNow tracker estimates that economic output fell 1%. Still, many fundamental economic indicators remain relatively healthy. The US Labor Department released data for June last week, showing that employers added 372,000 jobs last month. The unemployment rate remained at the low 3.6% it has held for the past four months. Wages rose 5.1% compared to a year ago, a strong pace of wage growth but a slight slowdown compared to prior months. This paints the picture of a labor market that remains healthy but may not be quite as tight as it was this spring. Consumers increased spending by just 0.2% in May in the slowest advance in months, but spending is not yet contracting. The personal savings rate fell to 5.4% in May, which is below the average from the past decade. However, US households built up $2.7 trillion in extra savings by the end of 2021, so they still have a significant cash cushion to draw down to maintain spending. However, consumer’s capacity to spend and willingness to spend are not the same. Consumer confidence as assessed by surveys is already deeply negative. The “misery” index, which combines unemployment and inflation, has surged over the last year. Morose consumer expectations could turn into a self-fulfilling prophecy if they cut back on spending, as consumer spending accounts for 70% of the US economy.

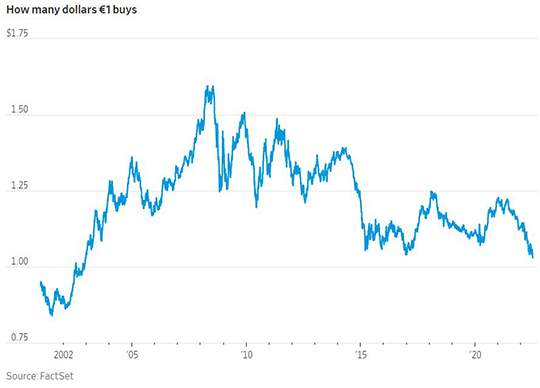

While the outlook for the US economy is uncertain, it may be darker for Europe. This is reflected in the strong US dollar, which has appreciated this year due to the underlying strength of the US economy and concerns in international markets. The ICE US Dollar Index, which measures the US dollar against a broad basket of currencies, has appreciated by 11% year to date. The US Federal Reserve moved more quickly to reign in high inflation than the European Central Bank. The ECB has moved slower as it faces a weaker regional economy that did not benefit from fiscal stimulus to the extent that the US did. The acute energy crisis facing Europe due to threat of being cut off from Russia could worsen from an inflationary shock into a growth shock if energy prices strangle manufacturing. Germany may be facing natural gas rationing this winter, and already recorded its first trade deficit since 1991 as manufacturing exports slow. The euro is rapidly approaching parity with the US dollar and many investors expect that it may fall even lower than that. The weak euro will depreciate the value of foreign earnings by US multinationals, which account for 14% of revenue in the S&P 500. However, it is arguably worse for euro-denominated assets. The Stoxx Europe 600 Index has fallen 15% this year in euro terms, less than the YTD fall in the S&P 500. However, after accounting for the deprecation of the euro, it has fallen farther than the S&P 500 in dollar terms. The weak euro also will make inflation worse, as it will make imports such as energy more expensive, as they are commonly priced in dollars.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1863