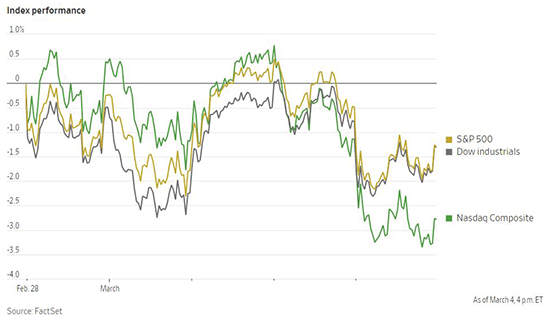

The escalating war in Ukraine and intensifying sanctions levied on Russia continued to drive heightened market volatility last week. US equity indices swung between losses and gains before dropping Friday to end the week down. The Dow Jones Industrial Average declined by 1.8% for the week while the S&P 500 fell 1.7% and the Nasdaq Composite dropped 3%. Though Russian oil and gas exports have not been sanctioned directly at this point, traders are already reluctant to engage with Russia and an auction of Russian Urals crude drew no bids. West Texas Intermediate crude oil traded above $116 last week in response, its highest level since 2008. The geopolitical tensions sent investors to the safety of government bonds. The yield on the US 10-Year Treasury note dropped to 1.712% by Friday in its largest one-week decline since the height of the pandemic panic in March 2020. European stocks fared much worse, with the Stoxx Europe 600 index falling 7% last week and closing at its lowest level in nearly a year.

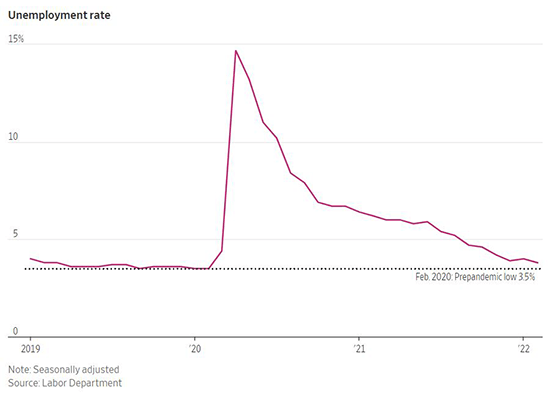

Updated data is showing that the US weathered the winter surge of the Omicron variety of COVID-19 relatively well and that economic activity has rebounded in recent weeks. OpenTable Inc. reported that US restaurant seating increased to 6% above its pre-pandemic level last month after dropping off during winter. US hotel occupancy is up and airport traffic reached 2.15 million people at the end of February, compared to only 1.19 million at the same time in 2021. Consumer spending was up by 7.2% in the first two weeks of February compared to last year overall. The increased spending on services relative to goods may also help to alleviate some of the supply bottlenecks that have been plaguing the economy. The US Labor Department’s employment release Friday also showed that employers hired a seasonally adjusted 678,000 workers in February, beating estimates and marking the fastest clip of job creation since last summer. The jobless rate fell to just 3.8%, drawing near to the pre-pandemic low of 3.5%. Leisure and hospitality exhibited the strongest growth, though job gains were broad based. Wages grew 5.1% in February, a slower pace compared to 5.5% in January, indicating that the labor shortage may be beginning to ease. IHS Markit estimates that higher oil prices due to the conflict in Ukraine will lower economic growth by 0.4% this year, but still expects US GDP to expand by 2.5% for 2022.

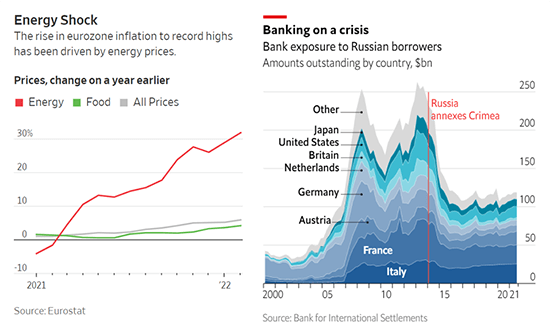

While the United States is relatively insulated from the impact of sanctions on Russia, Europe has several direct linkages with the Russian economy which may weigh on the region in the coming months. The Eurozone imports roughly 40% of its natural gas from Russia, and the outbreak of the conflict has seen the price of European natural gas more than double in just the last two weeks. The European Union reported Wednesday that inflation rose to a record high of 5.8% in February compared to the year prior. The high energy costs and inflation may depress both output and consumer spending. The sanctioning of the Russian Central Bank and exclusion of select Russian banks from the SWIFT banking system will likely dramatically decrease European exports to Russia by cutting off trade financing. Though foreign lenders decreased exposure to Russia significantly following the invasion of Crimea in 2014, foreign financing still stands at $121 billion. Most of those loans are on the books of European banks, posing a remote possibility of financial contagion. Capital Economics currently estimates that the conflict will likely lower European GDP by around 0.5%, but that there is downside risk for a slowdown by as much as 2%. Though their current base case is not for a recession, they recently cut their 2022 GDP forecast from 3.5% to 2.8%.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1570