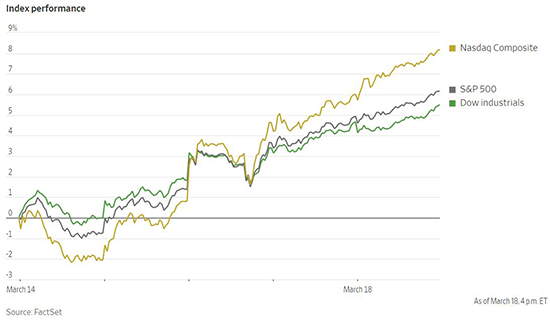

The US Federal Reserve raised the benchmark federal funds rate by 25 bps to the target range of 0.25% to 0.5%, but the first interest rate hike since 2018 was clearly telegraphed well in advance and was in range with expectations. Fed officials now project that rates will rise to near 2% by year end, a radical departure from their stance in December but merely catching up with what markets have already priced in. The median Fed projection for interest rates at the end of 2023 stands at 2.75%, which would be the highest rate since the Great Financial Crisis in 2008. The Fed has ended its program of monthly asset purchases and Fed Chair Jerome Powell indicated that it may begin shrinking the $9 trillion portfolio as soon as May. US stocks rallied strongly to post their best week since November 2020. The S&P 500 gained 5.9% while the Dow Jones Industrial Average rose 5.1%. Meanwhile the Nasdaq Composite surged 7.9%. The yield on the 10-year US Treasury note fell to 2.153% as the yield curve flattened, though it has not yet inverted. The Stoxx Europe 600 gained 5.4% for the week, also its best weekly showing since November 2020.

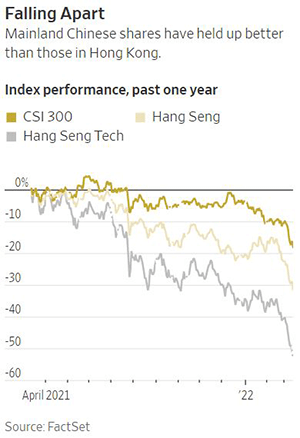

Chinese stocks have suffered a deepening rout in recent weeks as multiple issues have compounded to hammer investor sentiment. The SEC made another step toward delisting Chinese companies from US exchanges according to the 2020 US Holding Foreign Companies Accountable Act. This act bans the trading in the securities of companies who do not allow access to their audit papers for three years in a row, with which so far the Chinese government has refused to comply. This led to further pronounced selling of US listed Chinese companies as well as shares listed in Hong Kong on the Hang Seng stock exchange. This was quickly followed by news that China was locking down the province of Shenzhen for at least a week due to surging cases of the Omicron variant of COVID-19. Shenzhen is a major industrial province of 17.5 million people in close proximity to Hong Kong, which is currently the epicenter of a major outbreak. The province of Jilin with a population of 24 million in the northeast was placed under restrictions as well. This is the first time that China has mandated the lockdown of an entire province since the original outbreak in Wuhan in 2020. This shows the limits of the effectiveness of China’s COVID zero policy. Though stocks listed in the mainland CSI 300 index have generally held up better than offshore stocks over the last year, they sold off as well as investors dumped companies in sectors such as tourism and casinos.

The impact on global markets from Russia’s invasion of Ukraine has been most dramatic in commodities so far. The importance of Russia and Ukraine in producing many basic materials has seen prices surge for agricultural goods, industrial metals, precious metals, and energy. The prices of many of these commodities have since dropped again from their recent highs but remain substantially elevated relative to their level prior to the outbreak of the conflict. Global benchmark Brent crude futures briefly spiked as high as $130 per barrel, fell back into the $90 range, and now trade near $107.93. The possibilities of a ceasefire, lower Chinese demand and higher output from OPEC have all contributed to the volatility. The London Metal Exchange was forced to suspend trading of nickel for a week due to extreme price fluctuations. The wild price swings are causing many market makers to step back from trading. Liquidity is drying up, with the number of open contracts in crude futures dropping to its lowest level since 2015. The limited trading volume is leading to wider spreads and larger margins and is further exacerbating the price swings. The Russian stock market remains closed, but Russian sovereign bonds have suffered massive devaluations as sanctions dramatically increased the risk of default. Russia managed to make a $117 million interest payment last week in US dollars, but it is far from certain that it will avoid default. The probability of default this year implied by credit default swaps ticked lower to 57% from as high as 80% in the week prior.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1602