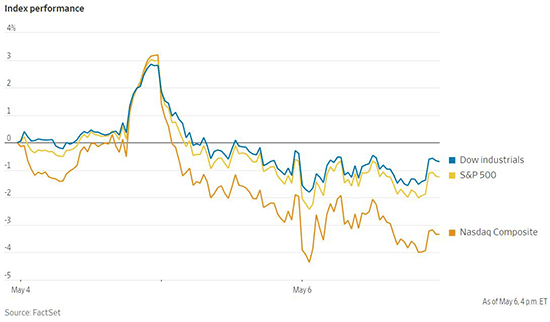

The US Federal Reserve delivered an interest rate hike of 50 basis points at the May Federal Open Markets Committee meeting last week, as widely expected. Though this was the largest upward move in interest rates since 2000, markets initially rallied in relief that the move was not even larger. It was also announced that the Fed would begin decreasing the size of its balance sheet in June at the initial rate of $47.5 billion per month. The pace of quantitative tightening is then planned to increase over three months to $95 billion per month. Fed officials indicated they plan to shrink the $9 trillion balance sheet by roughly $3 trillion over three years. However, stocks rapidly gave up their gains for the week on Thursday and continued lower on Friday. The Nasdaq Composite ended the week down 1.5% while the S&P 500 ended with a loss of 0.2%. The yield on the 10-Year US Treasury note ended the week up decisively at 3.124%.

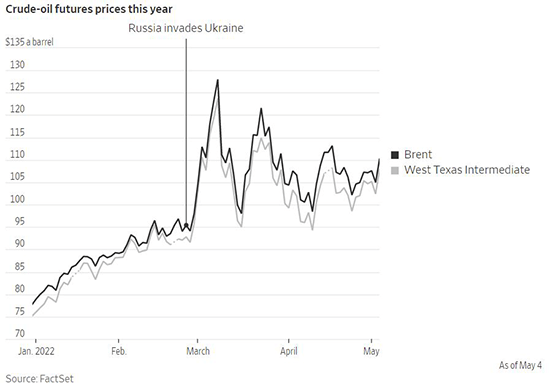

The run-up in crude oil and natural gas prices this year has exacerbated headline inflation figures significantly across the world. The supply of Russian oil and gas is now increasingly in question as the diplomatic fallout from the invasion of Ukraine has worsened in recent weeks. Russia cut off natural gas flows to Poland and Bulgaria due to their refusal to switch payments to rubles. Meanwhile, the European Union last week proposed an embargo on Russian crude which would take effect in six months, while Russian refined oil products would be banned by year end. This marks a significant escalation that would reduce the global supply of oil, as not all of Russia’s oil exports to the EU can easily be rerouted to other countries. Despite surging commodity prices, major US oil firms and natural gas drillers are opting to largely maintain current production levels rather than investing in ramping up production. Investors are pressuring companies to remain disciplined with capital expenditures and focus on returning cash to shareholders via dividends and share buybacks. Regardless, increasing supply would be difficult due to shortages of supplies, equipment and labor. Though this strategy benefits investors in the energy sector, it will make central banks’ task of fighting inflation more difficult.

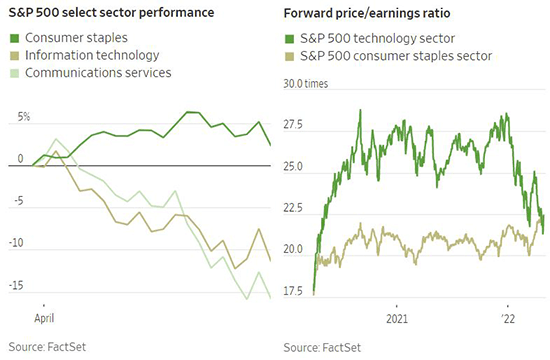

The selloff in the technology and media stocks, which benefitted during the early days of the pandemic, has been dramatic. Share prices of companies like Peloton, Netflix and Shopify have come crashing back to earth under the weight of higher interest rates and slowing growth outlooks. Speculative assets such as non-fungible tokens have not been spared either. Daily traded volumes of NFTs were down 94% over the last 30 days compared to their peak. Investors worried by the heightened volatility are pivoting to previously overlooked defensive sectors such as consumer staples, healthcare and utilities. Morningstar shows that net inflows into defensive ETFs this year have totaled $50 billion, already surpassing last year’s total flows and on pace to eclipse even 2020’s total of $75 billion. Consumer staples companies have performed particularly well, with 90% of companies in the sector beating analysts’ earnings estimates in the first quarter, compared with 80% for the S&P 500 overall. The consumer staples sector was the only one in the S&P 500 with a positive return in April, gaining 2.4% for the month while the full index fell 8.8%. The rush from growth stocks to stable, quality companies that pay dividends has been so pronounced that safety is beginning to look expensive. The consumer staples sector of the S&P 500 recently traded at a higher forward price/earnings ratio than the technology sector in an inversion of the typical relationship between the sectors.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1723