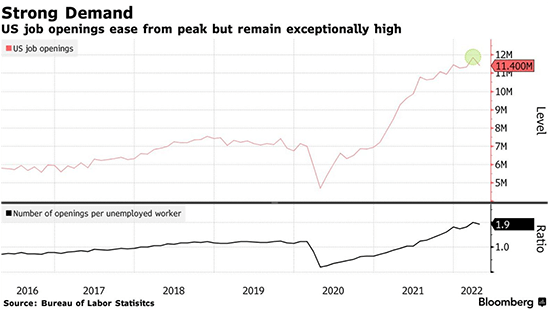

The US economy continues to run hot, but a growing number of economic indicators suggest that at the very least it is no longer accelerating. The labor market is very tight by historical standards, but in recent weeks several measures have leveled off. The Labor Department’s Job Opening and Labor Turnover Survey (JOLTS) showed that US job openings decreased to 11.4 million in April from 11.9 million in March. There were roughly 1.9 jobs available for every unemployed worker in April, a very high level but also a slight decrease from March. Employers created 390,000 new positions last month, a robust rate but the slowest pace of job growth in over a year. Wage growth cooled in May to 5.2% from 5.5% in April. The housing market is also showing some initial signs of levelling off. Dramatically higher mortgage rates are slowing the volume of housing sales. Existing home sales fell 5.9% in May from a year earlier in a continuation of April’s 2.4% decrease. The housing supply chain is also starting to normalize. Lumber futures for July delivery are down 52% from the recent high in March. Though those are both welcome trends, home prices are still rising for now. Home prices rose 14.8% in April compared to a year earlier to a record high of $391,200 on the national level. It is still too soon to determine if US inflation has peaked, but if these trends continue that would be a step in the right direction for the US Federal Reserve.

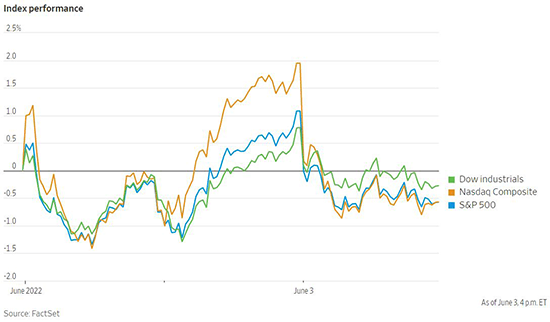

Though US stocks rose at one point last week, by Friday’s close they had given up those gains and ended the week with a loss. The Dow Jones Industrial Average, Nasdaq Composite and S&P 500 all had losses of around 1% for the week. Several US Federal Reserve officials reiterated their generally hawkish stance, reinforcing the likelihood of interest rate hikes of 50 basis points in coming meetings. US economic data still appear strong, giving credence to the possibility that the economy can withstand further interest rate increases. Looking at the month of May overall, the strong bounce in the last week of trading saw the S&P 500 avoid bear market territory and claw back to roughly flat for the period, though it was down 13.3% for the year through May 31. The DJIA also finished May roughly flat and was down 9.21% for the year through the end of the month. Breaking down US and European companies into their sensitivity to bond yields for the month of May is illuminating. According to Bloomberg, stocks that generally perform better with higher bond yields saw positive earnings revisions and price performance during May, while those that prefer lower yields saw earnings downgrades and negative performance for the month. The yield on the 10-year US Treasury note rose for the week and is now back up to 2.955%.

The European Union announced a new round of sanctions on Russia last week that lay out harsher terms than were expected. The EU came to an agreement on banning imports of Russian crude oil and refined fuel via ships, which account for more than two-thirds of current imports. There was an exclusion made for imports via pipeline to appease the holdout of Hungary to come to the negotiating table. However, other nations including Germany and Poland will discontinue pipeline imports by the end of the year. The embargo would cover roughly 90% of Russia’s oil exports to Europe by year end. The agreement also includes a ban on European companies from insuring Russian oil cargos on ships as well. These companies underwrite insurance for the vast majority of the shipping industry, which will make it difficult for Russia to divert these exports to other destinations. In response, OPEC+ agreed to increase production by 648,000 barrels per day in July and August. Though that represents a 50% increase from the prior arrangement, the production boost stops short of making up for the loss of Russian oil on international markets. The price of oil futures surged in response and will likely contribute to higher inflation, particularly in the Eurozone. This complicates the situation for the European Central Bank, as inflation in the Eurozone accelerated in May to a new record high of 8.1%.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1782