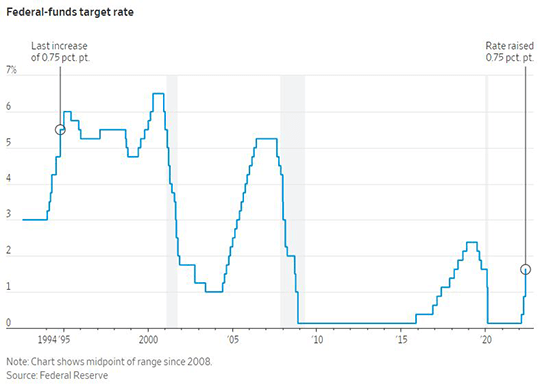

The US central bank raised the benchmark federal funds rate last week by 0.75%, the largest increase in interest rates since 1994. The fed funds rate target range now stands at 1.5%-1.75%. The Fed had consistently communicated that it would likely be hiking interest rates by 50 basis points, but inflation unexpectedly rose in May to an 8.6% annual rate, its fastest clip in 40 years. The market had already adjusted expectations following the release of the inflation report, sending the yield on the two-year US Treasury note up by 0.7% in the five days through Tuesday. The Federal Open Markets Committee voted 10-1 in favor of the larger move in interest rates. Fed Chairman Jerome Powell also left the door open for the possibility of another interest rate increase of 75 basis points for the July FOMC meeting. All Fed officials indicated they expect the benchmark rate to be at least 3% by the end of this year, and more than half indicated they expected rates might stand as high as 3.375%. The Fed now projects that interest rates may peak in this hiking cycle at 3.75% by the end of next year, up a full percent from projections as recent as March. It was also implied that these aggressive moves to tighten monetary policy will take a toll on the economy, with the unemployment rate estimated to rise to 4.1% in 2024 from its current level of 3.6%.

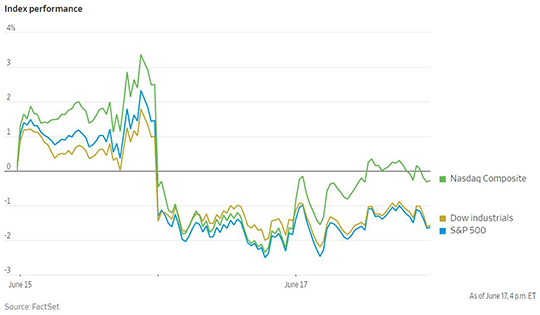

Though it will take some time for rapidly tightening monetary policy to begin to take an effect on the hot economy, the reaction from forward-looking financial markets was much quicker. The average rate on the typical 30-year fixed-rate mortgage surged to 5.78% last week. That marks both its highest level since 2008 and the fastest weekly increase in mortgage rates since 1987. The average interest rate on credit cards also soared past 20% in response to higher benchmark rates. The yield on the US 10-year Treasury note also spiked up to nearly 3.5% at one point, before settling back down to 3.222% to end the week. The increased likelihood of an economic recession took a significant toll on equities as well. The S&P 500 fell 5.8% last week in its greatest weekly decline since the onset of the COVID-19 pandemic back in March of 2020. After repeatedly rallying at the 20% decline point in recent weeks, the S&P 500 broke through that resistance level and is now officially in a bear market, dropping 22.9% year to date. The Nasdaq Composite and Dow Jones Industrial Average both fell 4.8% for the week. Small market capitalization stocks were punished even more severely for the worsening economic outlook. The Russell 2000 equity index fell 7.6% last week.

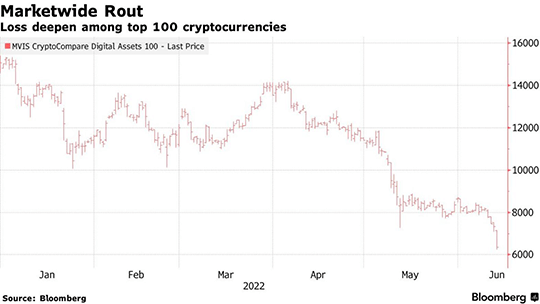

The notoriously volatile cryptocurrency market was not spared from the turmoil seen in other asset classes last week. The general risk-off sentiment seen across markets in the wake of the Fed decision was compounded by idiosyncratic risks specific to the crypto sector. The crypto lending platform Celsius Network LLC, which is one of the largest crypto platforms, announced on June 12 that it was halting all withdrawals, swaps and transfers. Celsius paid out interest rates of up to 18.6% annually for cryptocurrencies deposited on its platform. However, those high interest rates were made possible by lending out those assets to market makers and other exchanges as well as investing those funds in risky decentralized-finance projects. Now investors are belatedly realizing that cryptocurrency platforms lack the customer protections of a traditional bank as liquidity dries up. The halting of transfers by Celsius prompted a panic that saw investors pull assets from other crypto platforms and continue to sell digital tokens. The cryptocurrencies bitcoin and ether are now down 54% and 70%, respectively, so far this year. The total market value of the top 100 cryptocurrencies fell below $1 trillion last week, when as recently as November it stood at $3 trillion. Major crypto companies including Crypto.com, BlockFi, and Coinbase Global all announced significant layoffs this week as market sentiment for the sector worsens.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1809