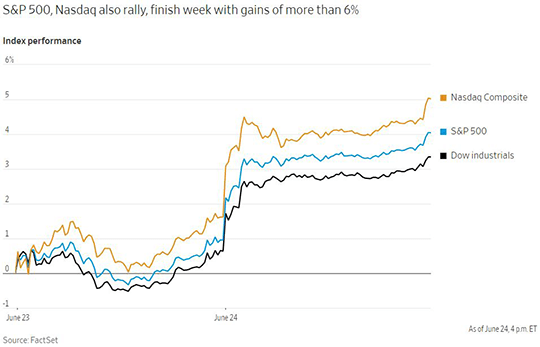

New economic data last week clearly showed that economic activity is cooling in both Europe and the United States. S&P Global produces purchasing managers indexes (PMI) that indicate economic expansion above the level of 50. The US PMI fell to 51.2 last month to hit a low for the last five months. The Eurozone PMI also slowed sharpy to 51.9 from 54.8 in the month prior. Though typically readings so close to contraction would be taken as a negative indicator for markets, in the current environment any cooling in overheated economies is a welcome indicator. That would suggest that central banks might not need to raise rates as aggressively as previously expected to bring inflation under control. US markets rallied strongly following the data release. The S&P 500 finished the week with a gain of 6.5% just after it had fallen into a bear market. The Dow Jones Industrial Average rose 5.4% over the week, while the interest-rate sensitive Nasdaq Composite surged by 7.5%. This shows the high uncertainty in the current market environment as well as the benefits of staying invested when large upside swings can occur in a single trading day. All three indexes gained around 3% on Friday alone.

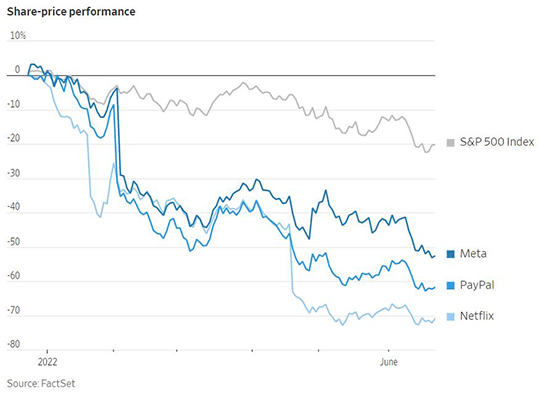

Last week the index provider FTSE Russell rebalanced its indexes, which resulted in some interesting recategorizations of individual stocks. During the period of low interest rates over the last decade, companies with strong growth prospects for the future were bid up to very high price-to-earnings multiples. Technology growth stocks were emblematic of this trend and reached their zenith during the COVID-19 pandemic. However, with the current regime of higher inflation and central bank tightening, the Russell 1000 Growth Index is now down 29% this year as current earnings gain increased importance relative to future earnings. Major technology companies have sold off severely in this environment, with Meta down 50% this year, PayPal down 60%, and Netflix down 70%. Meta now trades at a forward price to earnings ratio of just 12.2, lower than the S&P 500, which currently trades at 15.8 times forward earnings. These companies now trade at such a low valuation multiple that their weights are being decreased in the Russell 1000 Growth Index and they are being added to the Russell 1000 Value Index. This would have been unthinkable a year ago when they were very expensive by traditional valuation metrics. Another notable change is that small energy stocks have appreciated so strongly this year that they are being moved from the Russell 2000 Index up to the Russell 1000 Index of larger capitalization stocks. This will change the sector compositions of the different market capitalization indexes.

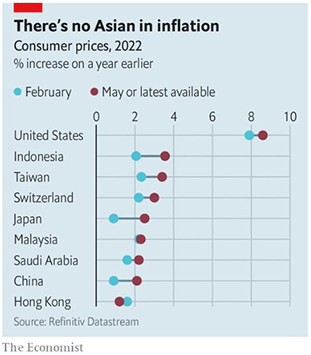

The current bout of rapid increases in prices is global in scope, but inflation is still remarkably calm in certain select regions. The Economist tracks economic indicators for 42 large economies, just 8 of which currently have inflation readings below 4%. Almost all of these countries are in Asia, with the exceptions of Switzerland and Saudi Arabia. One reason for the calmer inflation in the region is due to differences in diet in Asia compared to the West. Many countries depend on wheat as a staple crop, whose market has been severely disrupted by the Russian war in Ukraine. Wheat prices have risen by 17% since the invasion. Asia, in contrast, leans more heavily on rice, which has avoided those disruptions and has risen only by 8% over that period, in part due to higher fertilizer costs around the world. Another idiosyncratic reason is that the Asian staple of pork shot up in price due to a disease outbreak in prior years and has since returned to normal levels, adding a counteracting deflationary force into annual calculations. The other major reason is that the Asian region has been much slower to roll back restrictions related to COVID-19 than the West. Many countries are just now beginning to lift travel and quarantine restrictions. Though the roughly two-month long quarantine and lockdown of Shanghai ended at the beginning of June, there is a high likelihood that similar renewed lockdowns will be enforced by the Chinese government in the future. The uncertainty is having a dramatic effect on depressing retail sales and business investment. Though Asia may have avoided most of the problems of high inflation so far, it is still wrestling with issues of strangled economic activity.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1845