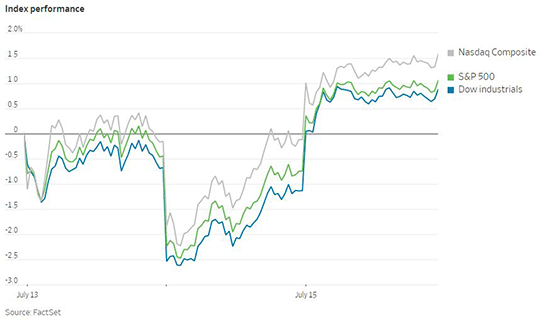

US equities sold off throughout the week as the second quarter earnings season began in an environment of apprehension regarding the trajectory of the global economy. The US Commerce Department released updated retail sales figures for the month of June on Friday, indicating that consumer spending rose 1% last month. This shows that the primary engine of the US economy is holding up so far despite high inflation. The preliminary estimate for the University of Michigan survey of consumer sentiment showed a small improvement from its recent all-time low. Equities rallied in relief to finish the week. The S&P 500 cut its weekly losses to 0.9% while the Nasdaq Composite finished down 1.6%. Financials rallied the most on Friday, recouping some of their decline following disappointing releases by several major US banks earlier in the week. Analysts currently are estimating that US corporate earnings grew by 4.2% in the second quarter. The S&P 500 currently trades at roughly 16 times projected earnings over the next 12 months. That is much closer to its long term average than the level of 21.5 times earnings at which it started the year.

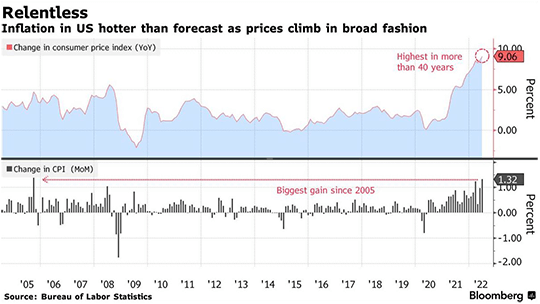

The US Labor Department released updated data last week showing that the US Consumer Price Index (CPI) rose by 9.1% in June compared to a year earlier. Inflation increased by 1.3% in June compared to a month earlier, the most rapid monthly increase since 2005. This is the fourth month in a row that the annual inflation rate has topped the consensus forecast by economists and marks another new high for the past four decades. Large increases in food, gasoline and electricity all helped push up the headline inflation figure. Core CPI, which excludes volatile food and energy prices, rose 5.9% compared to a year ago. The annual and month-on-month core CPI rates were both comparable to the rates seen in May. There are some early indications that several sources of headline inflation pressure may ease in the coming months. Gasoline prices have fallen in July and a recent decline in commodity prices may see grocery prices cool as well. Retailers currently have a glut of inventory which may result in discounts in the prices of goods, though that has not been seen in the data yet. Unfortunately, rising housing costs will likely continue to push up core services inflation for a while yet. The Federal Reserve Bank of San Francisco estimates that higher shelter costs may increase CPI by 1.1% through this year and next. There are, however, limits on how much higher rent can go. An analysis by Redfin showed that rents were up by 14% in June compared to a year earlier. Though this rate is still high, that is the slowest rate of increase since October, suggesting that landlords are seeing declining demand with higher rents.

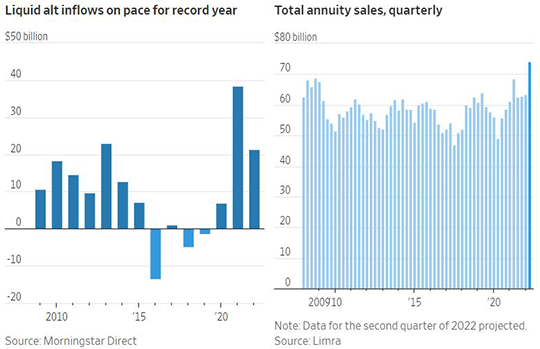

The selloff in both stocks and bonds this year has led investors to broaden their allocations beyond traditional asset classes. Liquid alternative funds and ETFs are one area of the market that has seen inflows this year. Liquid alternatives include a wide array of strategies that often utilize derivates such as futures and options to attempt to provide diversification by generating returns with low correlations with traditional assets. Morningstar Direct shows that inflows into liquid alts this year through the end of May have totaled $21 billion, on pace to beat least year’s record inflows of $38.3 billion. EQIS offers access to several liquid alternative strategies, including the American Beacon AHL Managed Futures Fund and the Catalyst Millburn Hedge Strategy Fund. Annuities are another asset class that has attracted a surge in inflows so far this year. Fixed-rate annuities do not decline in value when interest rates increase, in contrast to bonds. The yields offered on fixed-rate annuities are now significantly higher compared to last year as well. Annuity sales are projected to have reached $74 billion in the second quarter of this year, which would beat the prior quarterly record that occurred during the financial crisis of 2008.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

LF1880