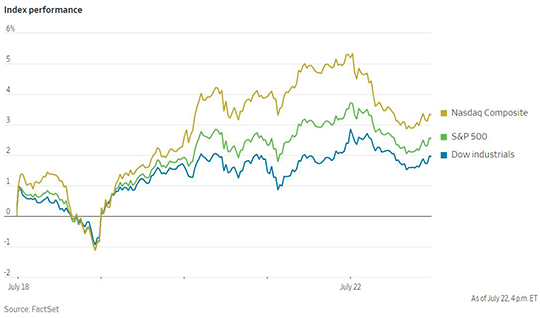

US stocks held on to gains for the week despite slumping on Friday. The S&P 500 rose 2.55% for the week, marking its best showing since June. Communication services and technology stocks were the worst performers on Friday, with Meta Platforms falling 7.6% and Alphabet falling 5.6%. Companies that delivered second-quarter earnings that were not as bad as analysts had feared rallied this week, including Netflix and Tesla. S&P 500 companies are still beating earnings estimates so far for the second quarter, though by only 3.6%, below the five-year average of 8.8%. The projected net profit margin for the S&P 500 for Q2 currently stands at 12.4%. This is lower than earlier estimates for the quarter and the net profit margin from a year ago, but still stands above the five-year average of 11.2%. The two sectors that are expected to report higher net profit margins for Q2 compared to last year are energy and materials. However, all other sectors are projected to see declining profit margins due to cost pressures. US government bonds rallied on Friday, with the yield on the 10-Year US Treasury note falling to 2.781%.

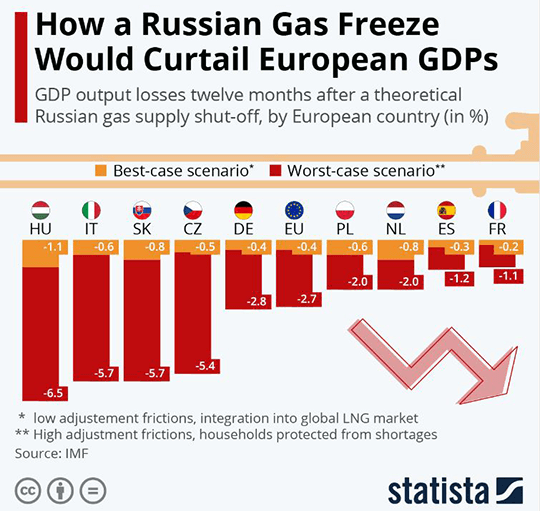

The European Central Bank (ECB) raised its key policy interest rate by 50 basis points last week. This was a larger increase than had been communicated previously, showing the depth of the ECB’s concerns with inflation. The policy rate now stands at zero after eight years of negative interest rates. Economists now forecast that the ECB will raise its interest rate to 1% by the end of this year and 1.5% by the end of 2023. The European economy is facing significant headwinds, making the environment more difficult for the ECB to navigate than the US Federal Reserve. One complication facing the ECB is the uneven economic strength for different countries within the Eurozone. Italy is one major economy saddled with slow growth and high debt. The resignation of the Italian prime minster Mario Draghi recently added to the political risks facing the cohesion of the Eurozone. That has seen the spread of Italian government debt over benchmark German bonds soar above 2%. The ECB announced a new program to support stressed peripheral economy debt in tandem with the rate hike in an attempt to head off investor concerns, though its efficacy remains to be seen. The other major issue facing Europe is its reliance on Russian energy exports. Concerns over the possibility of being cut off from Russian energy has driven energy prices up this year and exacerbated inflation. Many were relieved when Russia resumed delivery of gas through the Nord Stream pipeline last week after it was shut off for scheduled maintenance. However, delivery through the pipeline remains well below full capacity at only 40% utilization, leaving a high degree of uncertainty. The IMF recently estimated that if Europe was cut off completely from Russian gas exports, Eurozone GDP would be set back by a full 2.7% in a year’s time.

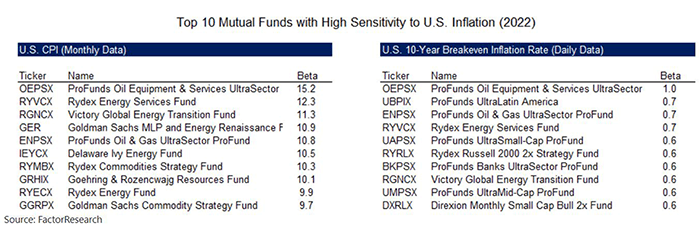

The bout of high inflation sweeping through the global economy has resulted in significant losses across most asset classes this year. However, there are some assets that have a high positive correlation with inflation. These assets thus tend to appreciate when inflation rises, in contrast to most other financial assets, making them an effective hedge against inflation. FactorResearch investigated the mutual funds and ETFs with the highest betas to inflation, as measured by the US Consumer Price Index (CPI) and the US 10-Year Breakeven Inflation Rate (BEIR). The mutual funds with the highest beta to CPI generally either provided exposure to energy sector stocks or diversified commodities futures. Meanwhile the mutual funds with the highest correlation to the BEIR included a more diverse set of strategies, including regional exposure to Latin America, US small and mid-cap stocks, and notably banks. The analysis of ETFs with the highest correlations to inflation showed that their focused, undiversified nature led them to have even higher sensitivity than the mutual funds. These included direct exposure to crude oil, as well as leveraged exposures to energy, shipping, Brazil, and gold miner equities. It is important to note that a strategy with a high beta to inflation may also exhibit high volatility. A relatively small position in a strategy with a high correlation to inflation may effectively hedge an entire portfolio’s exposure as well.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

LF1888