US Federal Reserve Chairman Jerome Powell gave a widely anticipated speech on Friday at the Fed’s annual conference in Jackson Hole, Wyoming. Powell used the opportunity to push back against perceptions among some investors that the Fed would pivot from its current path of tightening if it saw a deterioration in the economic data. Instead, Powell emphasized the Fed’s continued commitment to bringing inflation under control, and acknowledged that higher interest rates “will also bring some pain to households and businesses… Those are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

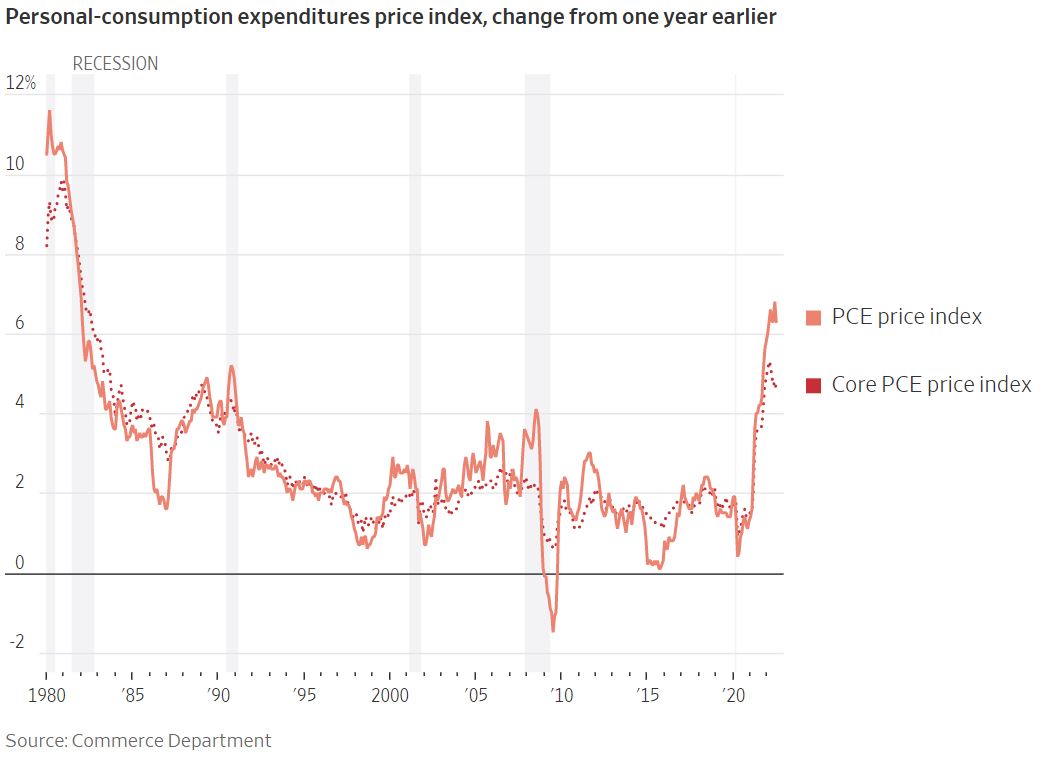

The July data for the Personal Consumption Expenditures Price Index (PCE), which is the Fed’s preferred gauge of inflation, was also released on Friday. The PCE rose 6.3% in July compared to last year, a slight deceleration from June’s 6.8% annual rate. The core PCE data, which excludes volatile food and energy prices, rose just 0.1% in month-on-month terms in July. That represents a welcome slowdown compared to June’s 0.6% monthly core-PCE rate. Powell acknowledged that development but stated that one month’s improvement in the data still “falls far short” of what the Fed “will need to see before we are confident that inflation is moving down.” Powell indicated the Fed would likely continue raising interest rates past the current neutral area to a restrictive level and that, “restoring price stability will likely require maintaining a restrictive policy stance for some time.” He emphasized that any change in the central bank’s stance would have a very high bar to clear, as “the historical record cautions strongly against prematurely loosening policy.”

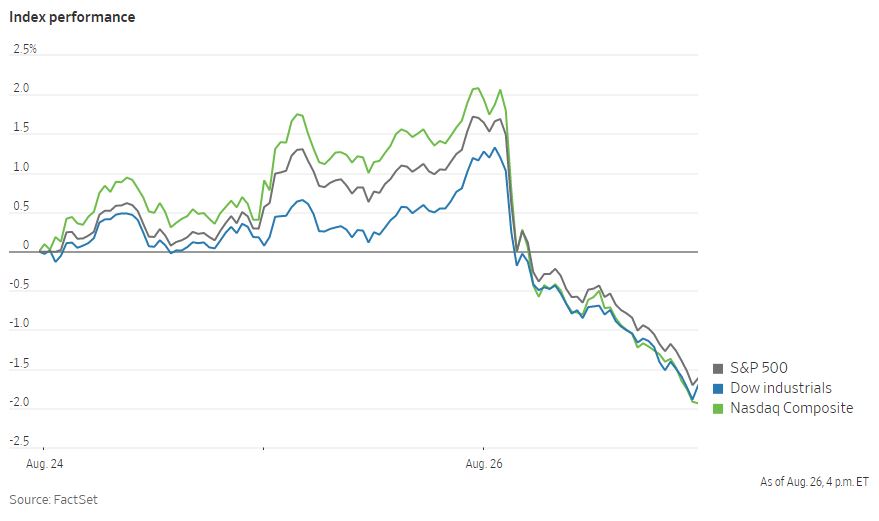

Though many market participants had expected the Fed to stand firm, US assets sold off as the Fed quashed overly optimistic hopes for a pivot. The Dow Jones Industrial Average fell roughly 3% on Friday following Powell’s comments. The S&P 500 closed down 3.5% on Friday while the Nasdaq Composite lost 4.9%. All three indexes fell more than 4% for the week. The losses in the S&P 500 were broad with all 11 sectors down on Friday, and technology falling the most. The yield on the 10-Year US Treasury note rose to 3.045% on Friday from 3.023% on the day prior. The yield on the 2-Year US Treasury note, which is more sensitive to Fed policy, rose to 3.419% from 3.372% on Thursday. Earlier in the summer, derivatives markets diverged from the Fed’s indicated expectations for the path of interest rates, with swap prices implying that interest rates would top out at 3.3% in early 2023. After a reassessment in recent weeks, the prices of swaps now implies that rates will be above 3.8% by May 2023, much closer to the Fed’s own projections. Following Powell’s speech, futures markets implied roughly even odds between a hike of 50 basis points and 75 basis points at the Fed’s next policy meeting in September. Investors will now be awaiting updated employment and CPI figures in the coming weeks.

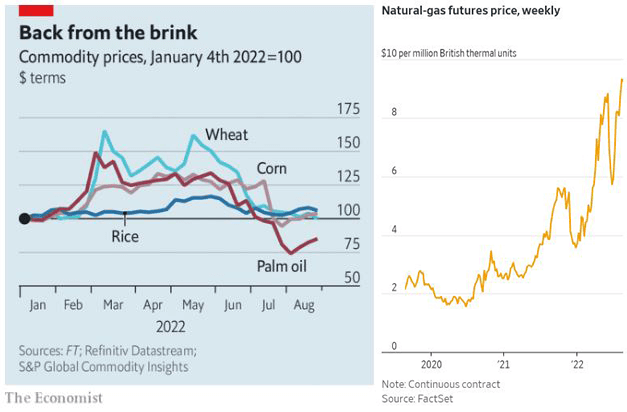

While global central banks pull the policy levers at their disposal to rein in inflation, commodities prices remain beyond their control. The current environment for commodities remains mixed with an undetermined impact on the path of inflation. Agricultural commodities have been one welcome bright spot in recent months. The prices of staple crops such as wheat and corn soared following Russia’s invasion of Ukraine back in February, as both those countries are major exporters of those goods to the rest of the world. The prices of many of those agricultural commodities have since collapsed to their pre-war levels as fears of shortages have proven to be overblown. Russia is on course to deliver a record harvest of wheat this year and a deal has been brokered for Ukraine to resume agricultural exports. While agricultural commodities may take some pressure off inflation, the outlook for fossil fuels is more uncertain. The scramble among European countries for alternatives to Russian natural gas is having ripple effects around the world. US natural gas futures surged again last week to a 14-year high. This is the most expensive natural gas has been in the US since the wide rollout of hydraulic fracturing technology greatly increased US gas production. The strong demand for exports of natural gas to other markets is weighing on domestic supplies, with inventories currently low for this time of year. Markets for crude oil have not been as tight due to expectations for lower demand as global economic growth slows. However, the Organization of Petroleum Exporting Countries is beginning to mull the idea of cutting production levels to help prop up the price of oil. That briefly sent the price of global benchmark Brent Crude back up over $100 per barrel last week. Though a worst-case scenario for commodities markets may have been avoided so far, it is still too early to sound the all clear.