After a five-day slump erasing over a trillion dollars in value, U.S. stocks rebounded Friday, with the Nasdaq 100 rising 1.5% and the S&P 500 gaining 1.2%. This recovery followed the longest losing streak since April, triggered by concerns over restrictive monetary policy and volatile market conditions. Stocks surged after Mike Johnson's reelection as House Speaker, which signaled potential Republican support for a pro-business deregulatory agenda. Meanwhile, bond yields climbed, with the 10-year Treasury reaching 4.6%, as Richmond Fed President Tom Barkin advocated for maintaining restrictive rates. Economic data offered mixed signals. U.S. manufacturing modestly improved in December, with the ISM Manufacturing Index reaching 49.3—still below the expansionary threshold of 50—while new orders hit a 1-year high. Corporate developments also drove market moves. Freddie Mac and Fannie Mae approached eight-year highs on plans to exit government oversight, while U.S. Steel dropped 6.3% after President Biden blocked Nippon Steel’s acquisition. The decision, citing national security, emphasized keeping the company American-operated. Additionally, beverage stocks slid following a U.S. Surgeon General proposal for cancer warnings on alcohol labels. In commodities, WTI crude climbed for a fifth consecutive day, reaching $74 per barrel, while gold pared weekly gains. Investors remain cautious, awaiting clarity on economic policies and the potential market impact of Donald Trump’s imminent return to the presidency.

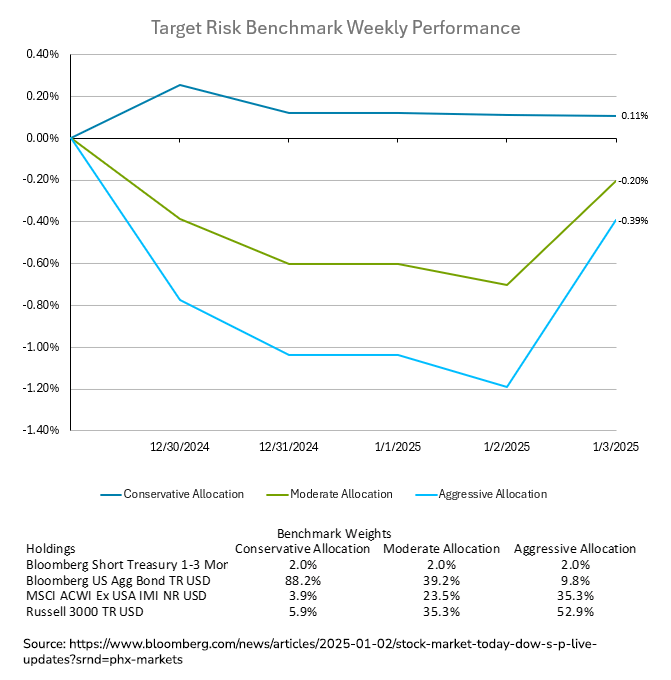

Despite the substantial rally in domestic equities and the smaller rally in international equities on Friday, major stock indexes ended the week with losses, weighing down the returns for aggressive and moderate investors for the week. The aggressive target risk benchmark above trimmed its weekly loss to -0.39%, while the moderate target risk benchmark bounced back to a small decline of -0.2% for the period. The Bloomberg US Aggregate Bond Index saw a respectable gain of 0.39% on 12/30 and drifted lower from there. That led the conservative target risk benchmark to hold onto a small gain of 0.11% for the week.

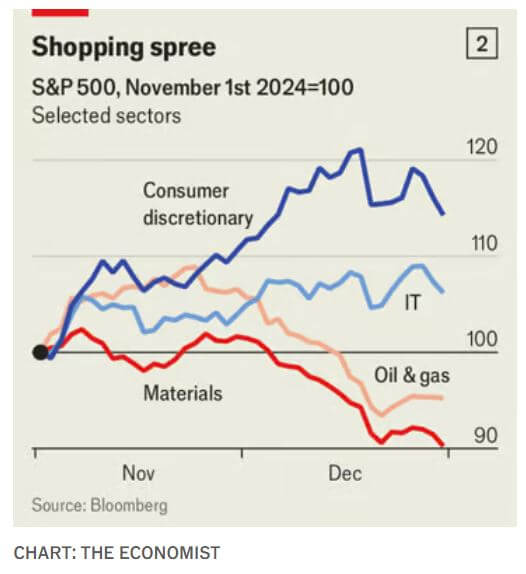

As Donald Trump’s second inauguration approaches, investors are shifting from speculating on his policies to reacting to their imminent implementation. Markets have been driven by uncertainties surrounding tariffs, fiscal policies, and their implications for growth, inflation, and asset prices. Conversations with analysts reveal that while tariffs are widely anticipated, the extent of retaliation and economic impact remains unclear. Most doubt large-scale deportations but express concern over potential inflationary effects from stricter immigration policies. Investors worry that Trump’s fiscal plans, including tax cuts and increased borrowing, could destabilize Treasury markets and drive yields higher. The 10-year Treasury yield has already risen to 4.6%, with most of the increase attributed to a rising term premium, reflecting fears of inflation and fiscal excess. These pressures could constrain the Federal Reserve, keeping interest rates elevated and potentially stoking market volatility. Currency markets signal skepticism toward Trump’s expressed desire for a weaker dollar. The greenback has strengthened, driven by safe-haven demand and expectations of reduced dollar outflows due to tariffs. Meanwhile, the Mexican peso and Canadian dollar have suffered, reflecting concerns over export-focused tariffs. In equities, U.S. firms continue to outperform global peers, with investors betting on robust corporate profits. Consumer discretionary, IT and financial sectors have thrived, buoyed by expectations of tax cuts and lighter regulation. However, industries such as oil, gas and materials have struggled, hindered by external constraints like low oil prices and tariff-driven cost increases. As Treasury yields rise and equity markets diverge, investors brace for potential turbulence. While bondholders’ fears of inflation and fiscal laxity weigh heavily, the interplay of policy announcements and market reactions will likely define the economic narrative of Trump’s second term.

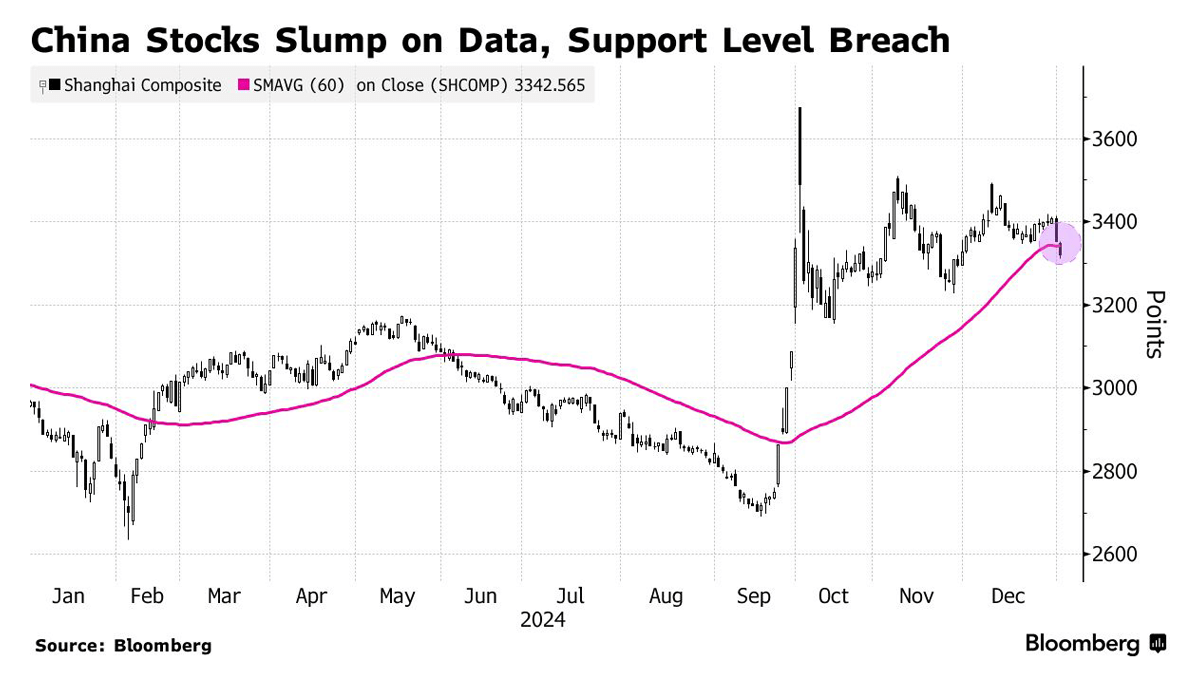

Chinese stocks experienced their worst start to a year since 2016, with the CSI 300 Index dropping 2.9% and the Hang Seng China Enterprises Index falling 3.1% on the first trading day of 2025. Investors are grappling with weaker-than-expected manufacturing data and the looming threat of increased U.S. tariffs. The Caixin manufacturing survey fell short of estimates, and Donald Trump’s impending return to the U.S. presidency added to market anxieties. Technical factors contributed to the losses, with the CSI 300 falling below its 60-day moving average, triggering further selling. Large financial stocks trading ex-dividend also weighed on benchmarks. Despite clearer stimulus signals from Beijing during December’s policy meetings, investor sentiment remains cautious, with concerns about China’s fragile economic recovery and medium-term deflationary risks. In 2024, Chinese stocks posted a rare annual gain of 15%, driven by a late-September stimulus surge. However, the market has since been range-bound, as traders await more robust stimulus measures. Beijing has pledged increased public borrowing and spending in 2025 to boost consumption, but significant actions are not expected until March’s annual legislative sessions. Global funds turned net sellers of Chinese equities in November, reversing previous inflows. Bond markets also reflected economic uncertainty, with China’s 10-year bond yields hitting record lows despite the central bank injecting liquidity. Equity trading volumes surged in Hong Kong but remained subdued in mainland markets, indicating hesitation among traders. Some market analysts suggest limiting exposure to Chinese stocks amid these uncertainties. While stimulus measures may offer hope, concerns about external pressures, such as tariffs, and internal economic fragilities persist, leaving investors cautious as they position for 2025.