U.S. stocks had their best week since the November presidential election, with the S&P 500 rising 2.9%, driven by cooling inflation, strong earnings reports, and renewed optimism about the incoming Trump administration. On Friday alone, the S&P 500 gained 1%, led by Nvidia, Tesla, and a 9% surge in Intel following acquisition speculation. Bonds also rallied, with 10-year Treasury yields falling 15 basis points during the week. Trump and China's Xi Jinping discussed trade and other key issues, potentially resetting relations between the two nations. Analysts noted the rally stemmed from oversold conditions, easing inflation, and investor optimism about the post-inauguration period, historically a strong phase for stocks. Major indices saw broad gains: the Nasdaq 100 rose 1.7% on Friday, the Dow Jones added 0.8%, and the Russell 2000 advanced 0.4%. Banks performed particularly well, with a key industry gauge surging 8.2% for the week. Despite risks like concentrated tech valuations, strategists remain optimistic, predicting continued growth in large-cap stocks, particularly in technology, financials, and consumer sectors. Bitcoin climbed to $105,000, while the Bloomberg Dollar Spot Index gained 0.3%. Analysts expect market volatility through earnings season, followed by stronger gains as buybacks resume. Historically, the S&P 500 averaged a 3.7% rise in the three months following inauguration. While challenges remain, such as high valuations and dependency on mega-cap tech, some strategists see U.S. equities as attractive, forecasting 9% earnings growth and an S&P 500 target of 6,600 by year-end.

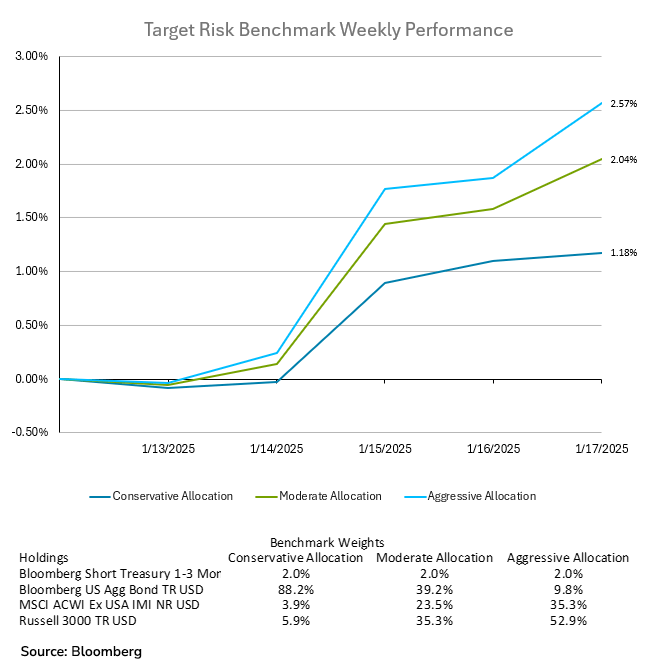

Investors across all risk tolerances participated in the rebound across markets, as seen in the target risk benchmarks below. Both domestic and international equities had significant gains for the week, leading the aggressive target risk benchmark to a remarkable 2.57% return for the week. The moderate target risk benchmark was not far behind with a healthy return of 2.04%. Even the conservative target risk benchmark participated in the rally, benefitting from the large drop in bond yields, finishing the week with a gain of 1.18%.

The December inflation report showed signs of easing price pressures, with core inflation rising 0.2% for the month—its smallest gain since July—below economists' expectations. The overall Consumer Price Index (CPI) increased by 2.9% year-over-year, driven largely by a 4.4% jump in gas prices. While goods prices showed some cooling, services prices—driven by categories like airfares, car insurance, and housing—remained firm. Housing prices, though cooling in private-sector measures, continue to support core inflation in official metrics. U.S. wholesale inflation cooled unexpectedly in December as well, driven by declining food costs and flat services prices, which could ease concerns about persistent price pressures. The Producer Price Index (PPI) for final demand rose 0.2% month-over-month, below economists’ forecast of 0.4%. Excluding food and energy, the PPI was unchanged from November. Food prices declined 0.1%, while energy prices increased 3.5%, contributing to a 0.6% rise in overall goods prices, though goods excluding food and energy remained flat. Commodity prices, including crude oil and corn, also saw gains, continuing upward trends from late 2024. Services prices were flat, showing one of the mildest readings of 2024. Despite these encouraging signs, inflation remains above the Federal Reserve’s 2% target, and the Fed is expected to hold interest rates steady in the short term. This cautious stance reflects uncertainty surrounding President-elect Donald Trump’s economic policies, which include tariffs, tax cuts, and immigration restrictions that could drive inflation higher. Traders adjusted their expectations for future rate cuts, with the probability of multiple cuts in 2025 rising to 51% from 35%. The probability of no rate cuts occurring in 2025 decreased to just 15% from 26%.

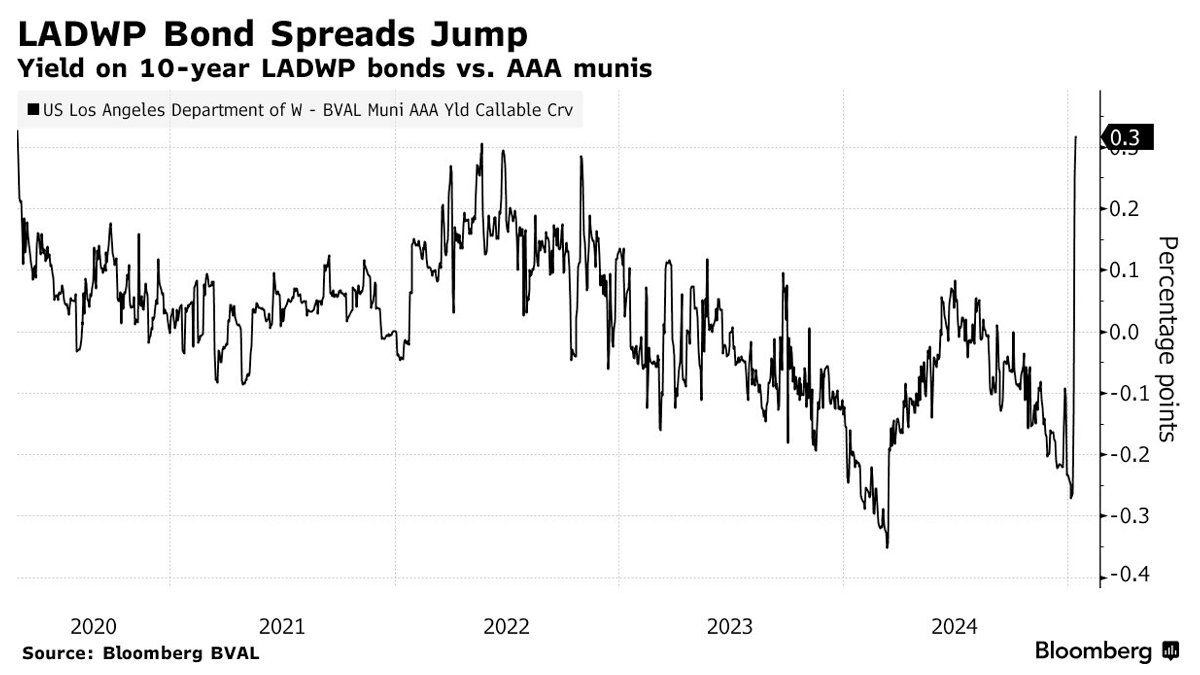

The recent Los Angeles fires have disrupted the municipal bond market, with the Los Angeles Department of Water and Power (LADWP) at the center of investor concerns. Historically resilient to natural disasters, municipal bonds have been shaken as LADWP’s credit rating was downgraded following the Palisades Fire, which destroyed over 2,000 structures and caused significant human and economic losses. The utility’s $18 billion in outstanding debt is now under scrutiny, with a planned debt sale delayed amidst rising costs and potential liabilities. Investor anxiety stems from LADWP’s perceived inadequate fire preparedness. Unlike utilities like PG&E, LADWP does not preemptively shut off power during windstorms, a policy now questioned given the fire’s scale. Furthermore, lawsuits allege insufficient water supply during the firefighting effort. The absence of an insurance fund for public utilities amplifies the financial risks for LADWP, potentially leaving ratepayers to shoulder the burden of damages and infrastructure upgrades. The disaster has broader implications for municipal bonds, emphasizing the increasing risks of climate-related events. LADWP’s bonds, once trading stronger than AAA-rated credits, have seen credit spreads widen sharply. LADWP’s challenges are compounded by its historical scandals and aging infrastructure, which could lead to sustained higher costs for ratepayers. A 2019 audit projected $42 million in annual wildfire-related losses for LADWP, a figure likely to rise as climate risks escalate. This event serves as a wake-up call for the municipal bond market, highlighting the financial vulnerabilities of public utilities in an era of intensifying natural disasters. Analysts caution that while the market has reacted strongly, the full extent of liabilities and long-term impacts remains uncertain.