This week, the markets navigated a mix of earnings optimism, central bank anticipation, and geopolitical clarity. Stocks reached fresh all-time highs, buoyed by upbeat Q4 earnings, with the blended growth rate climbing to 12.8% from 11.9%. Sentiment was further bolstered by easing fears around U.S.-China tariffs as President Trump signaled a preference to avoid punitive measures and Beijing ordered state-owned funds to support its stock market. The S&P 500 pared gains on Friday but maintained strength ahead of next week’s earnings from heavyweights like Apple, Tesla, Microsoft, and Meta. Meta's capex hike raised concerns among some traders, reminiscent of the telecom overspend of the early 2000s, but the stock ultimately rebounded after initial jitters. Corporate buybacks, expected to exceed $1 trillion in 2025, are also poised to support the market as windows reopen later this month.

In fixed income, bonds traded sideways as investors looked ahead to a pivotal week of global central bank decisions. The Federal Reserve is expected to hold rates steady, while markets anticipate modest cuts from the ECB, Bank of Canada, and Riksbank. Brazil remains on the opposite trajectory, with aggressive rate hikes stabilizing the real, now the top-performing major currency of 2025. Meanwhile, chatter about a potential bottoming in China gained traction, supported by both improved corporate outlooks and policy tailwinds. As markets digest these developments, the interplay between earnings, policy actions, and global economic dynamics will remain at the forefront.

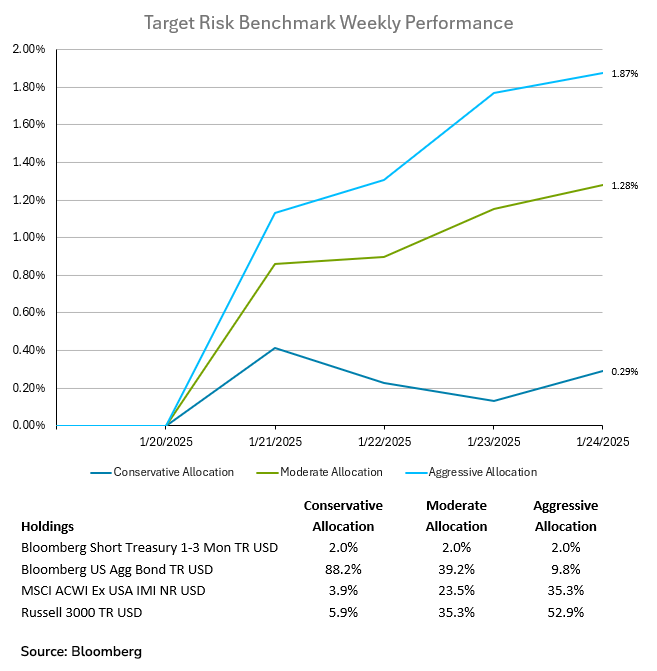

Investors across risk tolerances continued to participate in the rally across markets last week, as seen in the target risk benchmarks below. Equities posted gains for the week, leading the aggressive target risk benchmark to a remarkable 1.87% return for the week. The moderate target risk benchmark was not far behind with a healthy return of 1.28%. Even the conservative target risk benchmark experienced gains while the bond market softened on the week with rates continuing to back up, finishing the week with a gain of 0.29%.

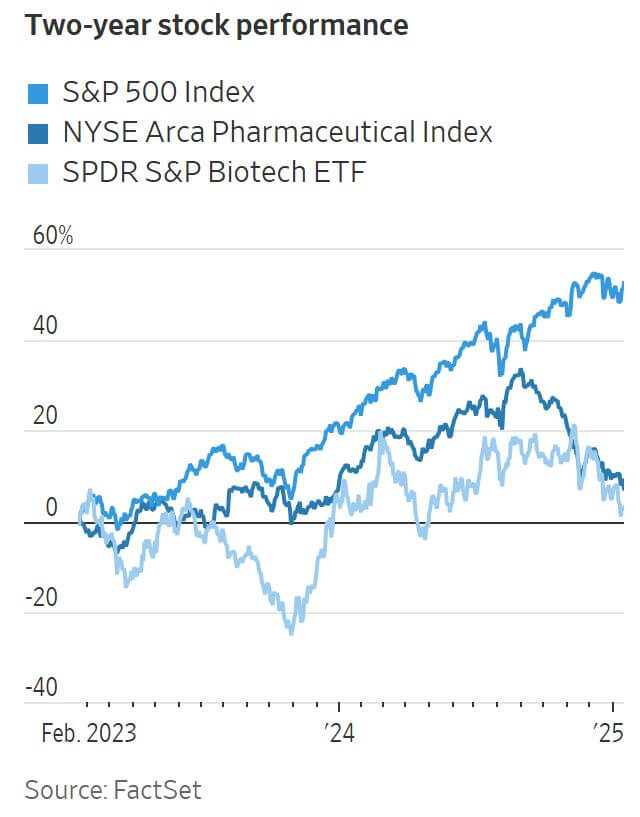

The biotech and pharmaceutical sectors have endured a challenging two years, with market dynamics and political shifts amplifying industry pressures. While Wall Street focused on the AI boom, drugmakers saw their valuations decline, trading at a discount to the broader market. The SPDR S&P Biotech ETF remained stagnant in 2024, underperforming innovation-driven sectors like tech. The Biden administration’s Medicare drug-price negotiation law dealt a significant blow to the historically influential pharma lobby, creating a difficult policy environment. However, the industry is cautiously optimistic as Donald Trump takes office. At the JPMorgan Healthcare Conference, executives noted potential benefits from Trump’s promises to reduce taxes and address pharmacy-benefit manager (PBM) practices, which inflate drug prices. Despite initial concerns over Robert F. Kennedy Jr.’s appointment as Trump’s top health official, many in the industry believe his influence might be moderated, with vaccine skepticism giving way to other policy focuses. Trump’s unpredictability is seen by some as a welcome change from the Biden administration’s consistently unfriendly policy stance. Key concerns persist, including the continuation of Medicare drug-price negotiations under the Inflation Reduction Act (IRA), which targets high-spending drugs like Ozempic. Industry hopes hinge on potential modifications to the IRA under a friendlier administration. While uncertainty surrounds Trump’s policies, the industry finds solace in a less overtly antagonistic administration. Valuations like the NYSE Arca Pharmaceutical Index trading below historical averages suggest some pessimism is already reflected, leaving room for upside if policy shifts align favorably.

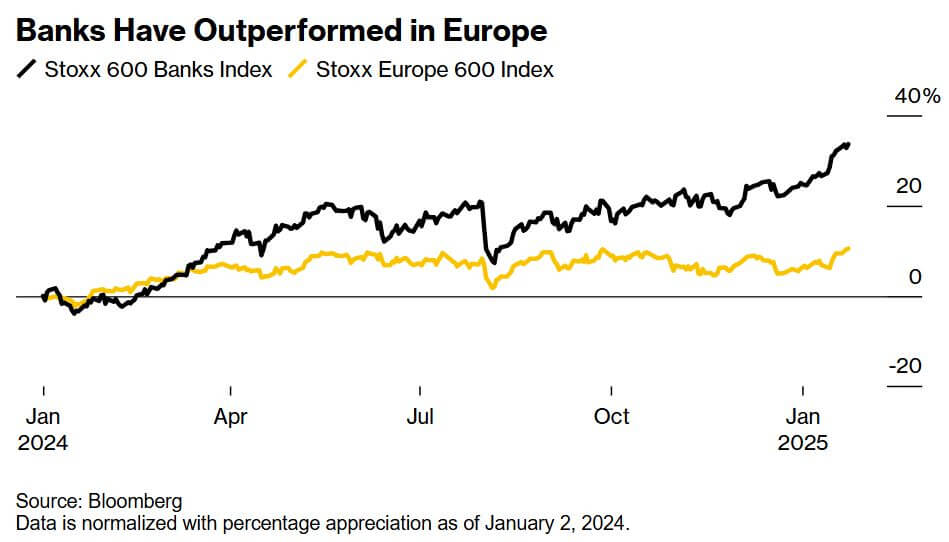

The European banking sector is poised for significant transformation, driven by favorable market conditions and strategic decisions by governments and private equity firms to divest their stakes. Elevated interest rates have bolstered bank earnings, with European banking stocks outperforming all other sectors in 2024 and projected to deliver an 8% average price return in 2025, according to analysts. Despite these gains, valuations remain attractive compared to U.S. counterparts, presenting an opportunity for further value creation. Several governments, including Ireland, Iceland and Hungary, are planning to exit crisis-era stakes in banks, aiming to strengthen public finances and reduce state interference. Notable moves include Iceland's renewed plan to divest its 42.5% stake in Islandsbanki Hf and Ireland’s consideration of a significant selloff in AIB Group Plc. These actions follow successful disposals in Greece, Germany, and Italy last year. In the UK, the government continues to trim its holdings in NatWest Group Plc, which have fallen below 10%. Private equity-backed banks are also preparing for initial public offerings (IPOs), signaling the end of a multi-year drought in banking listings. Key players include Lone Star Funds, considering options for Novo Banco SA, and Nordic Capital, evaluating an IPO for NOBA Bank Group AB. These moves reflect rising investor confidence, as returns on equity exceed 10%, particularly for restructured banks. However, challenges persist. Merger and acquisition activity, such as UniCredit’s unexpected bid for Banco BPM SpA, has disrupted some government plans. Additionally, European banks face competitive pressure from U.S. counterparts, potentially exacerbated by regulatory easing in the U.S. Analysts emphasize the need for further banking union reforms in the EU to strengthen the sector’s global standing. The outlook remains strong, supported by robust lending volumes and resilience in profitability, positioning European banks for continued growth into 2025 and beyond.