Wall Street traders remain concerned about inflation and the Federal Reserve’s reluctance to cut interest rates following economic data that reinforced price pressures. President Trump’s announcement of upcoming tariffs escalated trade tensions, impacting stocks like U.S. Steel and Amazon, which tumbled 4%. Treasury yields rose, and the dollar strengthened. The latest jobs report showed nonfarm payrolls increased by 143,000, with previous months revised upward. Unemployment stood at 4.0%, though measurement changes complicate comparisons. Wages rose 0.5%, fueling concerns that strong wage growth could sustain inflation. Despite a moderating labor market, analysts see resilience in employment, suggesting little immediate urgency for the Fed to lower rates. Fed officials, including Governor Adriana Kugler and Minneapolis Fed President Neel Kashkari, advocate keeping rates steady for now, citing stable employment and slow inflation progress. Some experts, like Neil Dutta at Renaissance Macro, believe rate cuts will eventually be necessary, but the Fed remains cautious. Investors now await the upcoming Consumer Price Index (CPI) report, which may provide mixed signals for inflation policy. Historical trends suggest January’s CPI could surprise to the upside, potentially affecting bond yields. However, a weaker-than-expected reading would be welcomed by markets. Overall, the Fed is expected to remain patient, likely delaying any rate cuts further into the year.

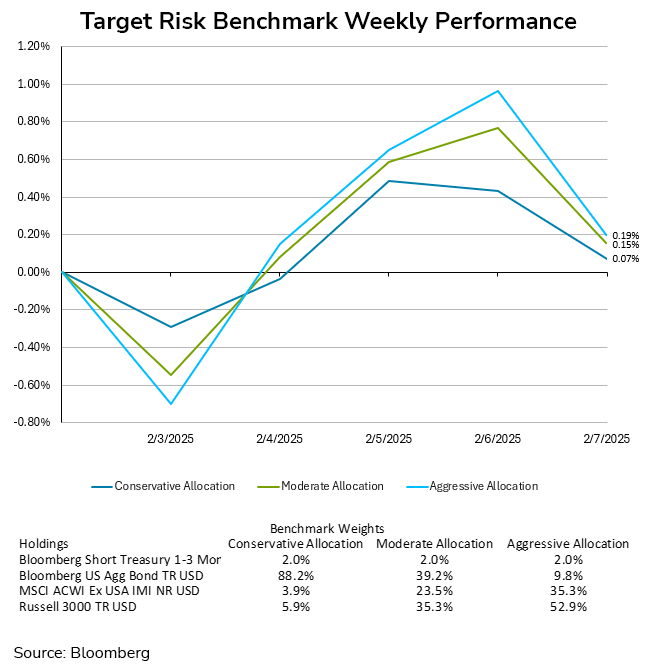

These worries produced intraday volatility across all risk tolerances, though investors ended the week near where they started. The Bloomberg US Aggregate bond index finished the week flat, while the Russell 3000 index of domestic equities finished the week with a small loss. International equities as tracked by the MSCI ACWI ex-USA Index finished the week with a small gain. The aggressive, moderate, and conservative target risk benchmarks performed similarly for the week, ending with small gains of 0.19%, 0.15%, and 0.07% respectively.

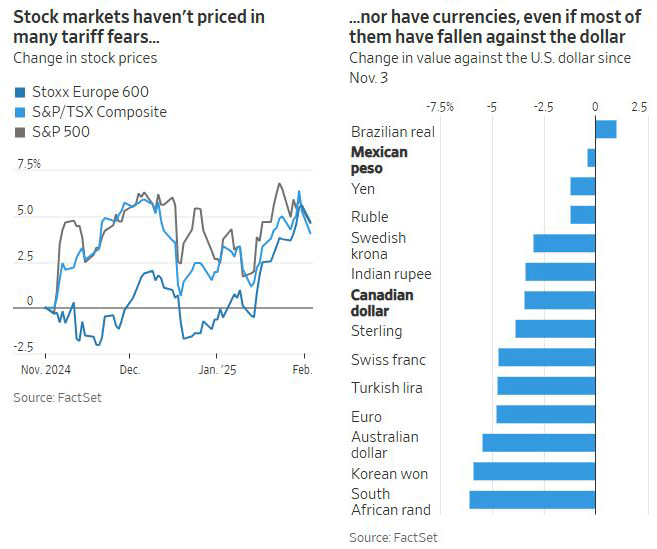

Investors who have dismissed President Trump’s trade war threats as mere posturing have so far been correct, but this assumption could be risky. Last Monday, both Mexico and Canada secured a one-month delay on new 25% U.S. tariffs by agreeing to strengthen border enforcement and crack down on fentanyl smuggling. Despite initial market declines, stocks largely stabilized, and the Mexican peso and Canadian dollar rebounded. This reinforced the belief that Trump’s tariff threats are primarily negotiation tactics rather than serious economic disruptions. Historically, Trump’s trade policies focused on specific industries and were phased in gradually. However, his current approach is far more aggressive, potentially raising U.S. tariff rates to their highest levels since the 1930s. This escalation could harm domestic growth, increase inflation, and destabilize global supply chains in unpredictable ways. Unlike past negotiations with China, coercing democratic allies like Canada may prove more difficult. Canadian leaders across the political spectrum have united against U.S. pressure, with some responding by boycotting American goods and canceling contracts. Prolonged uncertainty could also deter business investment, much like Brexit did in the U.K. While tariffs can sometimes boost domestic productivity, Trump’s broad-based duties lack a clear economic strategy and could backfire, particularly on industries reliant on imported components. With markets largely unshaken, there is a danger that the administration will push further, assuming minimal economic fallout. Given the S&P 500’s high valuation, the shift from "America First" to "tariffs first" poses a growing risk for investors.

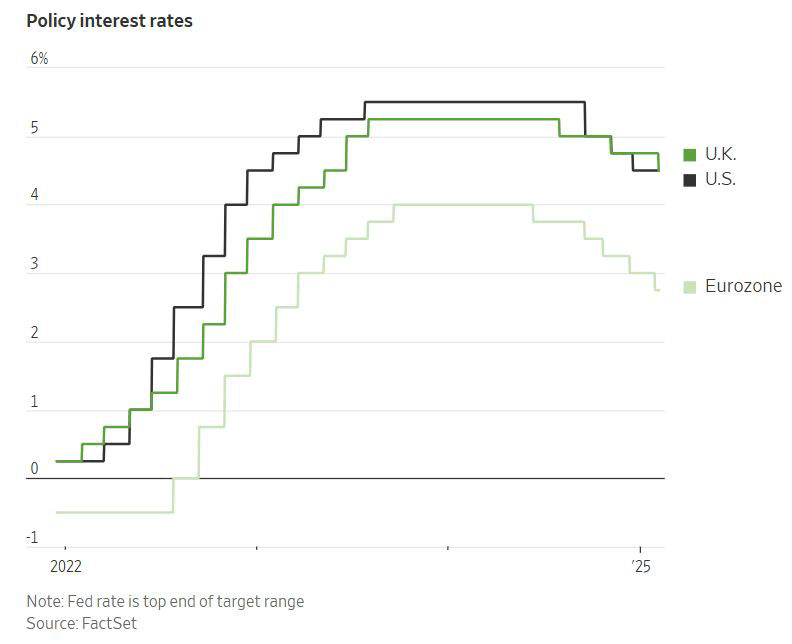

The Bank of England (BOE) cut its key interest rate by 0.25 percentage points to 4.5%, its third reduction since August, amid weak economic growth, persistent inflation, and uncertainty over U.S. tariffs. The bank lowered its U.K. growth forecast to 0.75% for the year, significantly trailing the U.S.’s projected 2.25% growth. BOE Governor Andrew Bailey signaled a cautious approach to further cuts while monitoring economic developments. The interest rate cut led to a 1% drop in the British pound against the dollar, while the FTSE 100 stock index rose 1.6%. Two policymakers even supported a larger 0.5% cut, suggesting the possibility of more aggressive easing ahead. Markets anticipate rates could drop to 3.75% by year-end. The BOE remains concerned about the economic impact of U.S. trade policy, particularly Trump’s newly announced tariffs on Canada, Mexico and China. While the Fed has held rates steady, the European Central Bank has continued its rate-cutting cycle. A weaker pound is adding to inflationary pressures by raising import costs, complicating the BOE’s efforts to balance growth and price stability. Despite the Labour government’s promise to boost spending, the BOE expects only a gradual impact on economic growth. Inflation is projected to peak at 3.7% this summer before easing toward its target by 2027. Bailey emphasized the uncertainty surrounding U.S. trade policies, warning that global economic fragmentation from tariffs could further weaken growth.