The bond market concluded the week with robust gains as weaker-than-expected U.S. retail sales reinforced expectations of Federal Reserve rate cuts. Treasury yields declined, with the 10-year yield dropping below 4.5%, marking its fifth consecutive weekly gain—the longest streak since mid-2021. Money markets have now fully priced in a Fed rate reduction by September. January’s retail sales saw the steepest decline in nearly two years, falling 0.9% after a strong 0.7% increase in December. Analysts attributed the drop to consumer caution following a robust holiday spending season. While some, like TradeStation’s David Russell, view this as supportive of rate cuts, others, such as Wells Fargo’s Gary Schlossberg, argue that persistent inflation offsets the case for early monetary easing. The broader economic landscape remains uncertain. While declining bond yields fueled a stock rally, concerns persist over consumer spending and inflation. Some strategists caution against overinterpreting a single data point, emphasizing that sustained weakness in consumer demand could pose risks. Goldman Sachs analysis suggests that market movements are increasingly driven by company-specific rather than macroeconomic factors, a trend expected to persist in 2025.

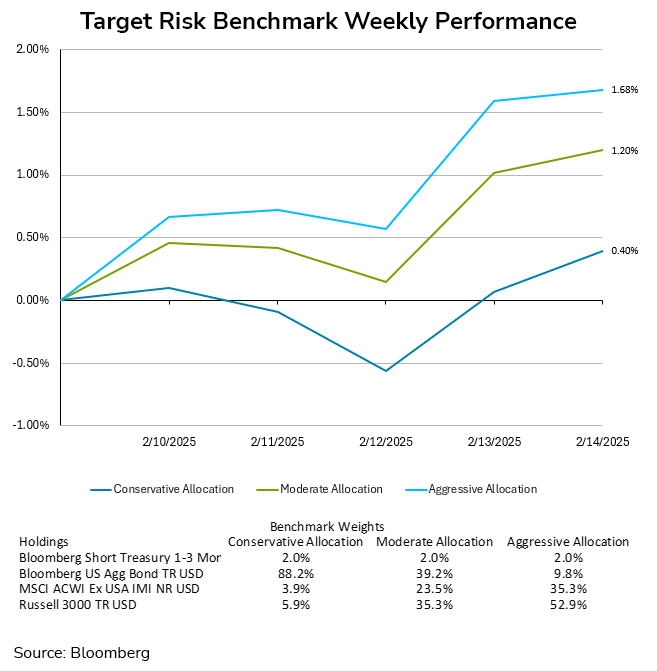

The broad-based rally to end the week boosted returns for investors across all risk tolerances. The aggressive target risk benchmark benefitted the most, with a gain of 1.68% for the week. The moderate target risk benchmark was not far behind with a return of 1.2%. The conservative target risk benchmark recovered from its earlier decline following the release of January CPI numbers, finishing the week up 0.4%.

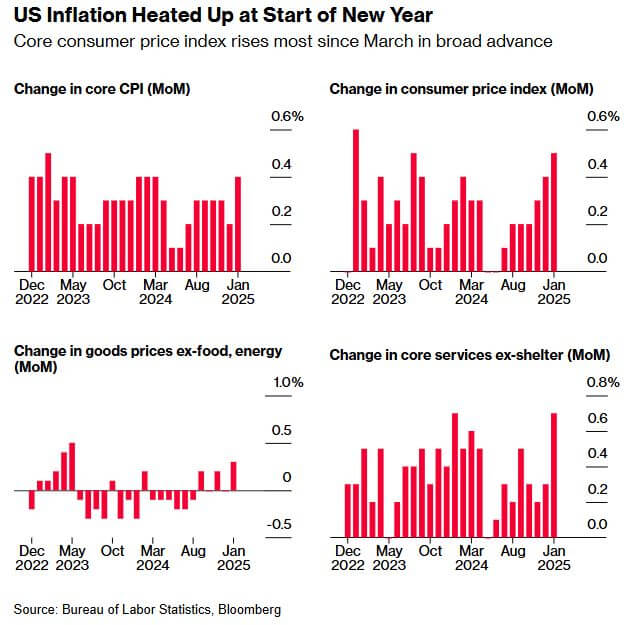

U.S. inflation accelerated at the start of 2025, diminishing the likelihood of multiple Fed rate cuts. The January Consumer Price Index (CPI) rose at the fastest pace since August 2023, driven by increases in grocery, gas, and housing costs. Core CPI, excluding volatile food and energy prices, climbed 0.4%, surpassing expectations, with notable contributions from car insurance, airfare, and a record surge in prescription drug prices. Shelter costs, the largest component of services, rose 0.4%, accounting for nearly 30% of CPI’s overall increase. U.S. wholesale prices also rose more than expected in January, signaling persistent inflationary pressures ahead of Trump administration tariffs. The producer price index (PPI) for final demand increased 0.4% from the prior month, following an upwardly revised 0.5% rise in December. Year-over-year, PPI advanced 3.5%, surpassing forecasts. However, the silver lining was that the components of PPI that feed into the Fed’s preferred PCE measure of inflation were relatively mild. Economists at Morgan Stanley and Goldman Sachs revised down their core personal consumption expenditures (PCE) inflation projections, though estimates remain above the Fed’s 2% target. This inflationary trend, partly attributed to seasonal price adjustments, signals that disinflationary progress has stalled. The Fed is now expected to maintain its current policy stance, reinforced by a robust labor market and uncertainty surrounding the Trump administration’s tariff policies, which have already influenced inflation expectations. Fed Chair Jerome Powell acknowledged that while inflation has moderated, the central bank's work is not yet complete.

President Trump’s tariff policies have made an immediate impact on the economy, creating uncertainty for businesses, workers, and trade partners. While some businesses support the Trump administration’s pro-manufacturing agenda, many are struggling to adapt. In a move to reshape U.S. trade policy, President Trump announced 25% tariffs on steel and aluminum imports, eliminating previous exemptions for key allies such as Canada, Mexico, Japan, and South Korea. These tariffs, set to take effect on March 12, are part of Trump's broader protectionist agenda aimed at boosting domestic production and countering what he calls unfair foreign subsidies, particularly from China. The President’s approach is reminiscent of his first term when he imposed similar tariffs in 2018. While those measures increased investment in domestic steelmaking—leading to a 6% rise in capacity, they did not result in significant production growth or job creation. The number of workers in steel mills remains below 2019 levels, and fresh aluminum output has declined to its lowest level in decades. Despite the tariffs, the U.S. continued importing high-value metal products, such as packaging steel and seamless tubes, due to a lack of domestic production capacity.

While U.S. steel producers such as U.S. Steel, Nucor, and Cleveland Cliffs have benefited, with rising stock prices, manufacturers that rely on these metals face higher costs. The National Foreign Trade Council criticized the move, warning that it will increase input costs for American manufacturers and hurt competitiveness. Analysts predict that the tariffs could push steel prices in the U.S. from $755 per ton to over $900, eliminating America’s cost advantage over Europe. Ultimately, while the tariffs may provide short-term gains for U.S. steelmakers, they risk harming the broader economy by raising costs for manufacturers, straining international trade relations, and potentially triggering retaliatory measures from key allies. The long-term impact remains uncertain, but President Trump's aggressive trade policies are likely to reshape global supply chains and metal markets for years to come.