Financial markets experienced another turbulent week driven by headlines over tariffs, recession warnings from the Trump administration amid a slide in consumer confidence and travel activity, and geopolitical risks (Russia/Ukraine conflict). The S&P 500 endured more volatility, dropping into the 10% correction territory before bouncing at the end of the week over diminished prospects of a federal government shutdown. Technology stocks came under pressure as investors are questioning lofty valuations driven by artificial intelligence spending, while global equity funds saw their biggest redemption so far this year. CFRA Research notes that in the prior 24 instances when stocks have fallen at least 10% from the peak while avoiding a bear market of at least a 20% drop, it has taken an average of eight months to reach a subsequent all-time high.

U.S. bond yields were volatile but ended flat from the prior week with 10-year U.S. Treasury yields settling at 4.31%, while commodities saw modest gains, with WTI crude up 0.9% and gold dropped 0.2% although it reached $3,000/ounce at one point. Bitcoin and Ether also recovered, following the prior week’s sell-off.

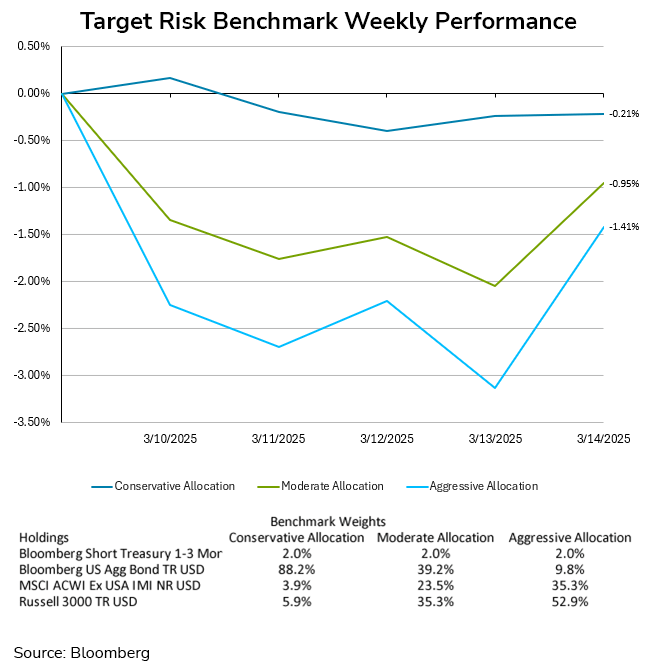

The challenging market environment led to losses across all risk profiles this week. Heightened equity volatility caused aggressive and moderate portfolios to experience sharp fluctuations throughout the week, though a Friday rebound helped limit overall declines. The aggressive target risk benchmark closed the week down -1.41%, while the moderate target risk benchmark posted a -0.95% loss. Rising bond yields added further pressure, resulting in a -0.21% decline for the conservative target risk benchmark. Elevated equity volatility, fueled by concerns surrounding potential tariff implications and persistent inflationary pressures, and rising bond yields were the primary drivers of this week's performance. Investors should remain vigilant and consider their risk tolerance in this evolving market environment.

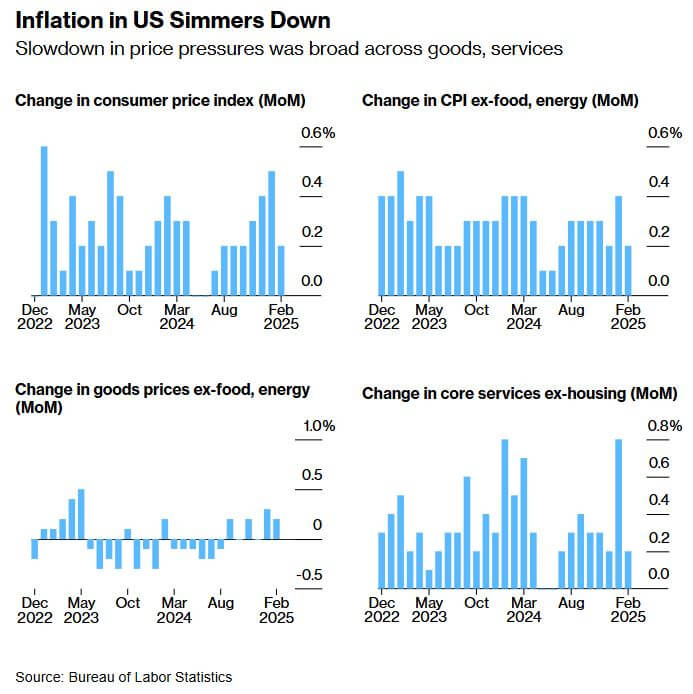

The latest Consumer Price Index (CPI) report indicates a cooling trend in inflation, with February’s annual increase at 2.8%, down from 3% in January. Core inflation, excluding food and energy, also eased to 3.1%, marking its lowest level since 2021. However, despite this moderation, the report offers little comfort to businesses, consumers, and Federal Reserve policymakers due to looming tariff concerns. While Wall Street initially responded positively, investor optimism waned as analysts emphasized that the inflation slowdown might not be as reassuring as it appears. The report largely predates the effects of newly imposed tariffs, which economists fear could reaccelerate inflation and limit the Fed’s ability to cut interest rates. Goldman Sachs has already raised its inflation forecast for the fourth quarter, reflecting concerns that trade policy could sustain upward price pressures. Consumer sentiment has also weakened, with a nearly 10% decline in the University of Michigan’s February survey, signaling anxiety about economic conditions. Consumer spending in January registered its sharpest monthly drop in four years. Meanwhile, key price components such as shelter costs continued to ease, but rising rents in parts of the U.S. suggest potential future inflationary pressure. Airline fares fell significantly, but Delta Air Lines reported softening domestic demand. Food inflation remains a challenge, particularly with egg prices reaching record highs due to bird flu-related shortages. While food and energy prices are excluded from core inflation metrics, their volatility can shape consumer inflation expectations. With inflation still exceeding the Fed’s 2% target, policymakers face a complex challenge. If tariffs sustain inflationary pressures, the Fed may be constrained in its ability to cut rates, balancing economic stability against the risk of further price increases.

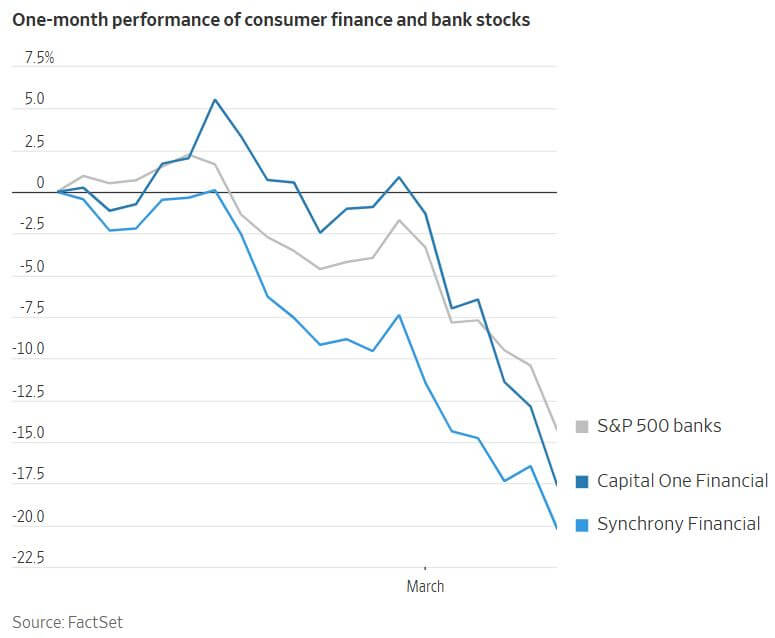

American consumers have long supported the U.S. economy with their spending and credit usage, but concerns are rising that they may be reaching their limits. Consumer lending stocks, including American Express, Capital One, Discover, and Synchrony Financial, have dropped significantly, reflecting fears of rising debt stress. Historically, spikes in late payments have triggered market concerns, though these were often limited to certain borrowers, especially those who took on excessive debt in 2021-2022 during stimulus-fueled lending booms.

Now, many of those bad debts are being processed, and Moody’s expects a slight decline in credit card and auto loan charge-offs later in 2025. However, fresh concerns include growing inflation-adjusted debt burdens, with average household credit card debt surpassing $10,000 for the first time since 2009. Additionally, fears of a recession, potential job losses, and rising costs from tariffs are making investors uneasy. Lenders primarily assess risk through employment trends—so as long as people have jobs, they tend to keep up with payments. However, changing debt priorities may also impact the financial landscape. Mortgage debt has become the top repayment priority, as homeowners strive to keep their low-interest-rate properties. This shift suggests credit card and auto loan repayments may take a backseat during financial strain. A particularly concerning trend is the rise in delinquencies among high-income consumers. While their late payment rates remain low, they have doubled since 2023, signaling growing financial stress. This group, which has the most flexibility in spending, could sharply reduce discretionary purchases if financial pressures mount. Despite strong household balance sheets overall, consumer confidence is shaky. A Fed survey found that Americans perceive a growing risk of missing debt payments, the highest concern since 2020. If these fears materialize, consumer spending could retract sharply, making lenders a crucial economic indicator to watch.