This week’s economic data showed further signs of a slowdown in consumer and business spending, reflecting anxieties over sticky inflation and the prospects of a looming trade war as the U.S. unexpectedly imposed tariffs on automobile imports. As President Donald Trump’s tariff policy expands into the so-called Liberation Day on April 2nd, consumers are growing more worried that the added duties will drive up prices and limit supply. Businesses have been stockpiling goods and inventory to stay ahead of anticipated tariffs. In the midst of this uncertainty, some market observers have noted extreme levels of investor sentiment, which can often serve as a contrarian signal, particularly during stressful moments. Technology and consumer stocks (especially global automobiles) came under increased selling pressure with the former seeing a pullback in growth expectations tied to artificial intelligence investments.

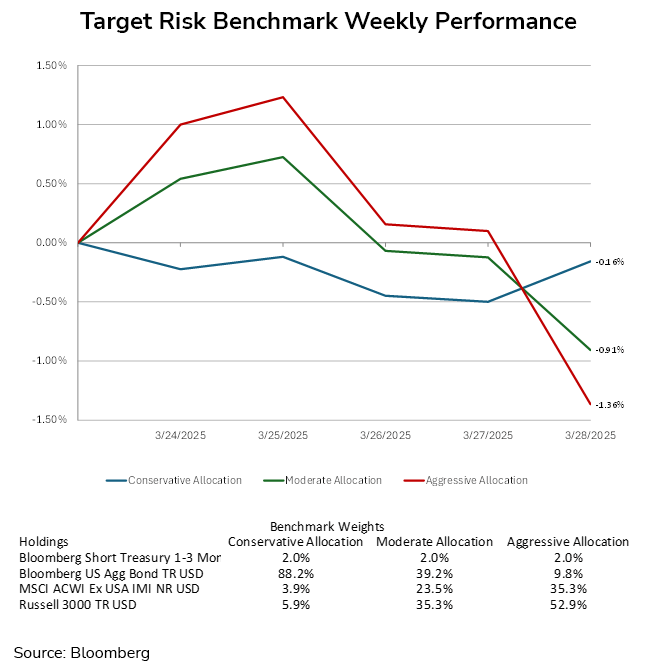

The high volatility in equities continued the roller coaster ride for moderate and aggressive investors for the week with equities having rallied early in the week only to sell off towards the end of the week. The aggressive target risk benchmark finished the week with a loss of 1.36%, while the moderate target risk benchmark lost -0.91%. Conservative investors benefited from the higher fixed income allocation, with the conservative target risk benchmark only losing 0.16% for the week.

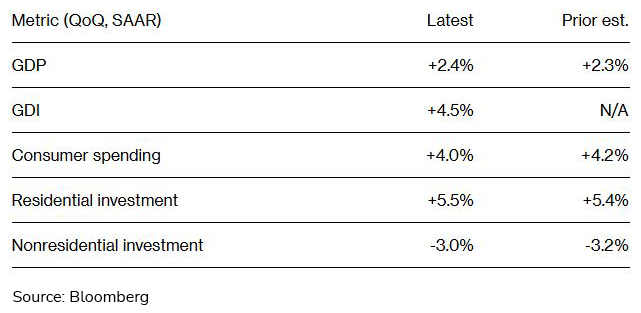

The U.S. economy demonstrated stronger-than-expected momentum in the fourth quarter of 2024, with GDP expanding at a 2.4% annualized rate, according to revised data from the Bureau of Economic Analysis. This upward revision reflects increased contributions from net exports, government outlays, and business investment. Meanwhile, core inflation, measured by the Fed’s preferred PCE index excluding food and energy, was revised down to 2.6%, reinforcing a disinflationary trend. Corporate profitability was a key driver, with after-tax profits surging 5.9% — the largest gain since 2022. Non-financial corporate profit margins widened to 15.9% of gross value added, suggesting firms retain substantial pricing power. This cushion may enable businesses to absorb upcoming tariff-related cost pressures without significantly raising consumer prices. Gross domestic income (GDI), which tracks income generated from production, rose a robust 4.5%, up from 1.4% in Q3. The average of GDP and GDI — often seen as a more accurate measure of economic activity — reached 3.5%, the strongest in a year. Nonetheless, consumer spending growth was slightly revised down to 4%, still indicating resilient household demand. Despite the strong finish to 2024, economists caution that headwinds are emerging. Analysts expect a deceleration in growth in 2025, citing rising uncertainty tied to former President Donald Trump’s trade-centric economic agenda. Early-year data point to a potential contraction in Q1, driven by a surge in imports as firms front-load purchases ahead of expected tariffs. This trend is reflected in a persistently high trade deficit. In labor markets, jobless claims remained stable at 224,000, signaling continued employment strength.

On Friday, the February Personal Consumption Expenditure (PCE) report further confirmed signs of consumer spending slowdown and sticky inflation. Real consumer spending rose just 0.1% as economists had been expecting a bigger bounce from weather-induced weakness in January. Notably, U.S. consumers cut back on travel and leisure as well as on restaurants, while increasing spending on durables such as automobiles to stay ahead of anticipated tariffs. The Fed’s preferred inflation measure, core PCE, rose 0.4% month-over-month and 2.8% over the last year, remaining stubbornly above the Fed’s 2% inflation target. Fed official comments point towards remaining on the sidelines before resuming interest rate cuts until they see the full extent of tariff policies and the effect on consumer prices.

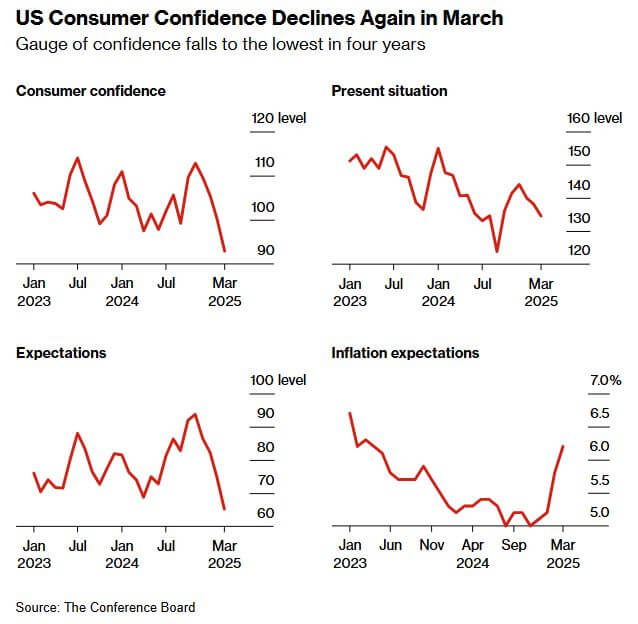

In March, U.S. consumer confidence dropped to its lowest level in four years, driven by concerns over rising prices and economic uncertainty amid the Trump administration’s expanding tariffs. The Conference Board's index fell 7.2 points to 92.9, below economists’ expectations. The outlook for the next six months plummeted nearly 10 points to 65.2—its lowest in 12 years—while current conditions saw a smaller decline. This slump in sentiment reflects growing fears of inflation and recession, with inflation expectations reaching a two-year high. Despite weak survey data, “hard” economic indicators such as low unemployment and improved manufacturing in February suggest the economy remains stable. However, optimism about future income has sharply declined, and expectations for personal finances hit their lowest point since July 2022. Economists and Federal Reserve officials are watching to see whether this negative sentiment translates into reduced consumer spending. Despite the bleak mood, buying intentions for big-ticket items like electronics and appliances rose—possibly as consumers aim to beat potential tariff-related price hikes.

The job market is flashing warnings signs as well. In February, median wage growth for job stayers rose to 4.4%, surpassing the 4.2% increase for job switchers, according to the Federal Reserve Bank of Atlanta. This reversal signals a cooling labor market, with layoffs rising and job seekers facing more competition. White-collar workers, in particular, are holding on to their jobs amid uncertainty. The rate of workers changing employers is also at a near four-year low, suggesting reduced mobility. While job openings and low unemployment still reflect a degree of labor market resilience, rising job cuts and economic volatility—partly due to Trump-era trade policies—are fueling recession concerns. Historically, job stayers have seen stronger wage growth following economic downturns, as seen after the 2001 and 2008 recessions, indicating a possible return to that pattern.