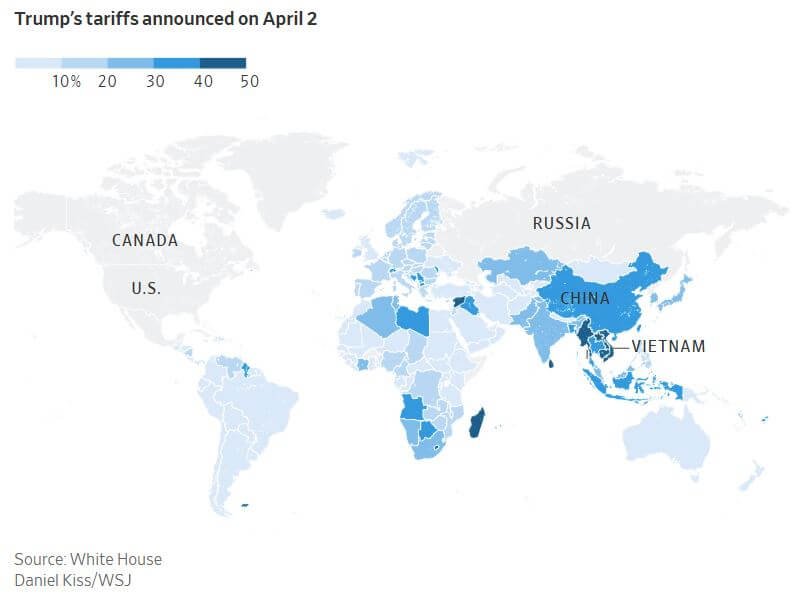

The financial markets have reacted sharply to escalating trade tensions initiated by President Trump’s tariff policies, with stocks experiencing a significant selloff, bond yields declining, and oil prices hitting a four-year low. Federal Reserve Chair Jerome Powell acknowledged that the economic damage from the trade war could exceed initial expectations, raising concerns about higher inflation and slower growth. Despite this, Powell maintained a cautious stance on adjusting interest rates. The S&P 500 recorded its steepest two-day drop since March 2020, losing approximately $5 trillion in value, while the Nasdaq 100 fell into bear market territory. Notably, stocks of major tech companies like Tesla and Nvidia fell, while US-listed Chinese companies such as Alibaba and Baidu also faced declines. Market analysts warn that recession signals are becoming more apparent as trade tensions deepen. Some investors, like Ed Yardeni and Bill Gross, see potential buying opportunities amid falling valuations. The Fed’s future course remains uncertain, with markets pricing in potential rate cuts, reflecting the tension between inflation risks and the possibility of an economic slowdown. While some financial strategists, including JPMorgan’s David Lebovitz, argue that equities are nearing dip-buying territory, others caution that the path to recovery is unclear given the economic uncertainty linked to tariff policies.

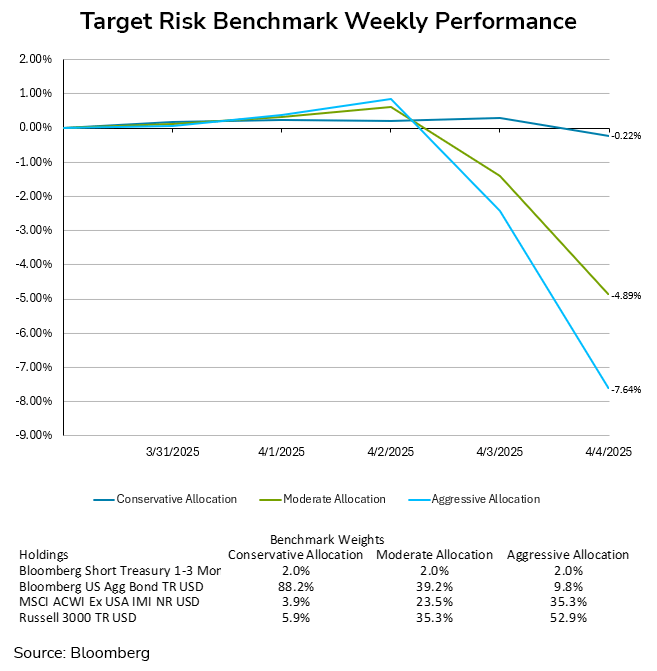

The dramatic plunge in global equities weighed heavily on the returns for aggressive and moderate investors. The aggressive target risk benchmark dropped an eye-watering -7.64% for the week, while the moderate target risk benchmark did not fare much better with a decline of -4.89%. The conservative target risk benchmark held up well with the flight to safety in markets driving down bond yields substantially, limiting weekly losses to just -0.22%.

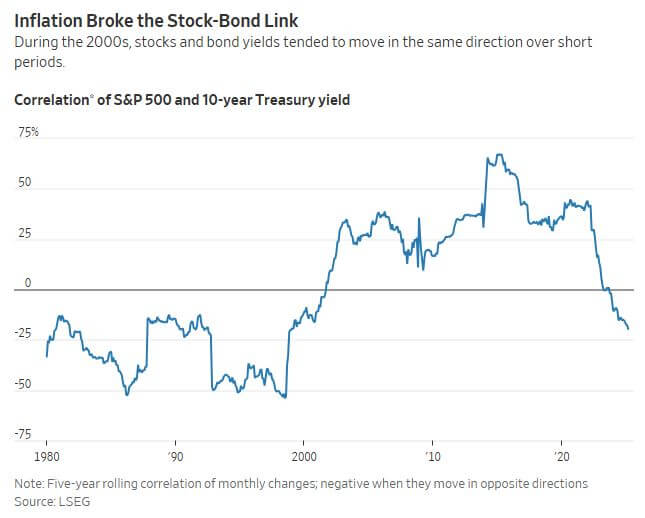

In uncertain economic times, investors look for ways to protect their wealth from a stock market downturn. Traditionally, assets like Treasurys and the U.S. dollar have provided a safety net. However, changing economic dynamics have made finding reliable “market insurance” more challenging, pushing investors toward gold as an alternative. Treasurys, once considered a dual-purpose asset providing both returns and protection, have seen their role evolve due to inflation sensitivity. In the past, Treasurys were reliable during downturns because bond yields typically fell when stock prices dropped, driven by Fed rate cuts. However, with inflation becoming a persistent concern, bond yields now sometimes rise even as stock prices fall, as seen in recent market movements. This shift means that Treasurys are no longer guaranteed to act as a hedge, though they still offer a reasonable yield and can perform well during financial panics. Thankfully, bonds did successfully act as a counterbalance to stocks during last week’s volatility. The U.S. dollar also faces challenges. Historically, it benefited from the “dollar smile” effect, strengthening both in good and bad times. However, the dollar’s current strength, fueled by foreign investments in the booming U.S. economy and tech sector, raises questions about its performance if the economy falters. If a downturn occurs, foreign money could exit, weakening the dollar rather than strengthening it as in previous crises. Gold has recently surged in value, partly as a hedge against inflation and geopolitical risks. While it can perform well during inflationary periods, its past performance shows vulnerability in severe crises when investors liquidate assets to cover debts. Cash remains a short-term secure option, but it doesn’t appreciate during downturns. Ultimately, investors are grappling with a lack of reliable safe havens. While traditional low risk assets maintain some benefits relative to volatile equities, all of them have some questions regarding whether they will hedge risk as effectively as they did in the past.

With the imposition of high tariffs by President Trump, it may be useful to draw comparisons to historical precedents where countries have employed similar strategies to shield domestic industries. Although some cases demonstrate successful industrial growth, such as car manufacturing in Asia and refrigerator production in South America, most experiences with protectionism have led to economic inefficiencies, stagnant growth, and reduced competitiveness. India’s experience illustrates the pitfalls of high tariffs. Following independence in 1947, India adopted an import-substitution strategy, imposing steep tariffs to nurture local industries. However, this approach failed to foster sustainable economic growth. Following a financial crisis in 1991, India significantly reduced tariffs, boosting economic performance. Despite this liberalization, some protectionist policies persist, notably in the textile sector, where high tariffs on synthetic fibers have hindered competitiveness compared to rivals like Bangladesh and Vietnam. Conversely, South Korea presents a rare example where tariffs contributed to economic success. In the mid-20th century, high tariffs protected Hyundai Motors, fostering its development into a global automotive leader. The broader South Korean economy similarly benefited from calibrated protectionism, maintaining global competitiveness while gradually liberalizing trade. This strategy enabled South Korea to transition from a low-income to a high-income economy, culminating in a free-trade agreement with the United States. Argentina, however, exemplifies the negative impacts of prolonged protectionism. Tariffs and import restrictions aimed at building local manufacturing resulted in inefficient industries and high consumer costs. Recent efforts to reduce trade barriers reflect recognition of the adverse economic consequences of such policies.