Wall Street closed a strong week with equities advancing, driven by megacap tech gains despite conflicting signals from President Trump on trade negotiations. The S&P 500 surpassed 5,500, marking its longest winning streak since January, propelled by surges in Tesla (+9.8%) and Alphabet. However, market momentum briefly waned after President Trump suggested he would maintain tariffs on China without substantial concessions. Resilience in equities contrasts with persistent challenges: tariff uncertainty, economic slowdown fears, and weak consumer sentiment, with inflation expectations reaching a 30-year high. Bloomberg reported China might suspend its 125% tariff on select U.S. goods, offering a tentative de-escalation sign. Corporate profit margins, buoyed mainly by tech since 2004, are vulnerable to tariff-induced cost pressures. Despite strong spending data, forward-looking indicators suggest slower growth, with economists projecting U.S. GDP expansion at 1.4% in 2025 and a rising recession risk (45% within 12 months). Strategists at Bank of America advise selling into rallies, citing sustained dollar weakness and ongoing capital outflows, particularly from European investors.

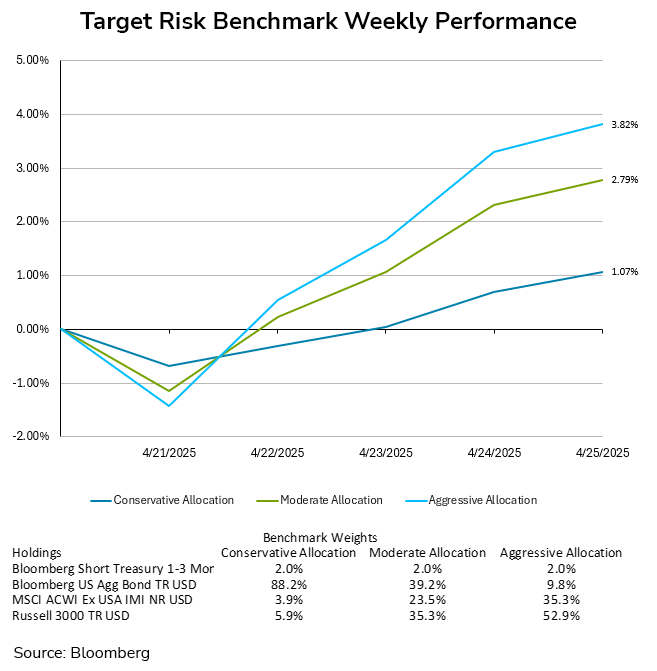

The recovery was broad based across asset classes, offering investors a much needed breather across all risk tolerances. The aggressive target risk benchmark benefited the most with a healthy weekly gain of 3.82%, while the moderate target risk benchmark was not far behind with a gain of 2.79%. The conservative target risk benchmark also benefitted from falling bond yields for the period, finishing the week up 1.07%.

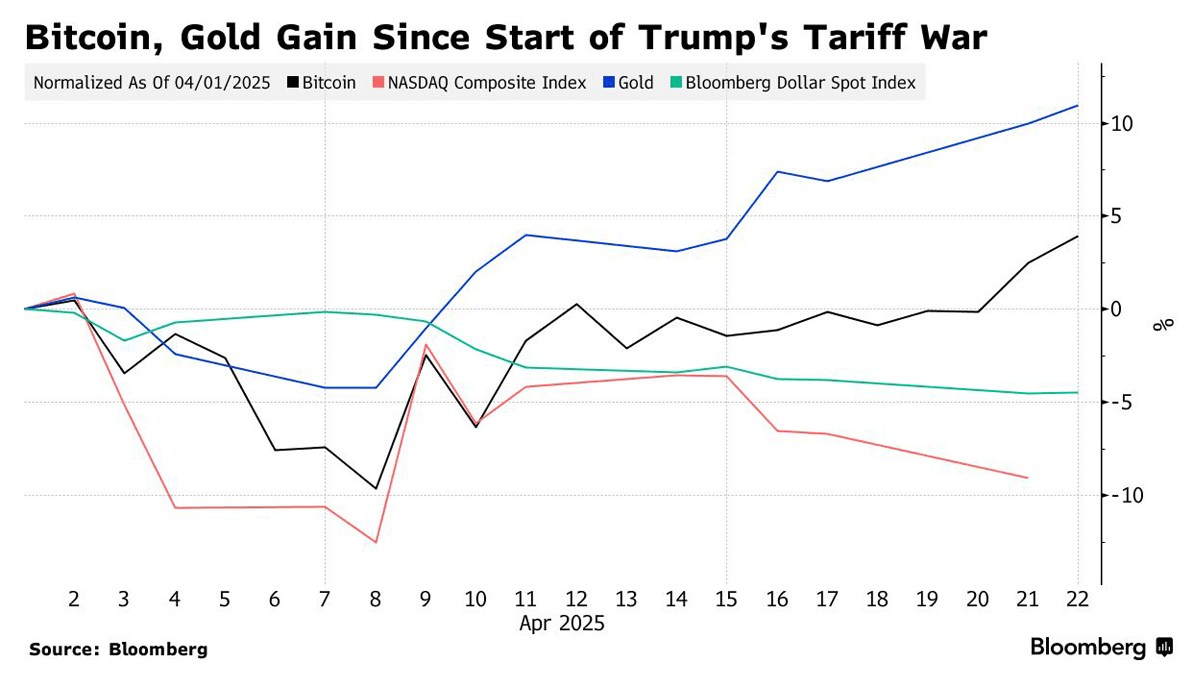

Gold retreated from a record high of over $3,500 an ounce last week as traders locked in profits following a rapid 10% rally this month. Overbought technical conditions also contributed to the pullback; the 14-day relative-strength index rose above 78, surpassing the 70 threshold that signals a potential reversal. The surge in gold was initially driven by escalating investor anxiety over President Trump’s repeated attacks on Federal Reserve Chair Jerome Powell, which threatened central bank independence and spurred a broad selloff in U.S. assets. Amid declining confidence in traditional safe havens such as Treasuries—due to both recent bond selloffs and concerns over U.S. fiscal health—gold has emerged as a preferred refuge. Analysts at Jefferies described it as “the only true safe haven left.” Despite the pullback, gold remains up nearly 29% year-to-date, outperforming most major asset classes. Goldman Sachs projects that gold could rise to $4,000 by mid-2026, citing growing demand for non-dollar safe haven assets. While short-term corrections are likely due to the market’s overbought condition, the medium-term outlook remains bullish amid ongoing economic instability and global uncertainty. For investors looking for exposure to precious metals, Freedom Investment Management offers several options, including EQIS Precious Metals ETF, iSectors Precious Metals, and the 3D Physical Precious Metals Model.

Bitcoin surged past $90,000 last week, sparking optimism that the digital asset is decoupling from its traditional correlation with U.S. tech stocks. Rising nearly 23% from its April 7 low, the cryptocurrency has shown increased resilience amid broader market volatility driven by President Trump’s new tariff regime. This rally positions Bitcoin closer to gold in investor behavior for now, acting as a hedge in times of geopolitical and monetary uncertainty. Analysts attribute this move to several key factors. The weakening U.S. dollar and mounting investor skepticism over the Fed’s independence—exacerbated by President Trump’s recent criticism of Chair Jerome Powell—have created a favorable environment for alternative assets like Bitcoin. Additionally, investor anticipation surrounding the President’s proposed Strategic Bitcoin Reserve (SBR), set for a Treasury review within two weeks, is contributing to bullish sentiment. Supporting the rally, U.S.-listed Bitcoin ETFs absorbed $381 million in inflows—the largest since January. Bitcoin’s latest rally reflects growing market confidence in its role as a store of value, particularly as geopolitical instability and monetary policy uncertainty shake traditional markets. The coming weeks—especially developments around the SBR—will be pivotal in cementing this shift. For investors looking for exposure to Bitcoin, Freedom Investment Management offers the iShares Bitcoin ETF.

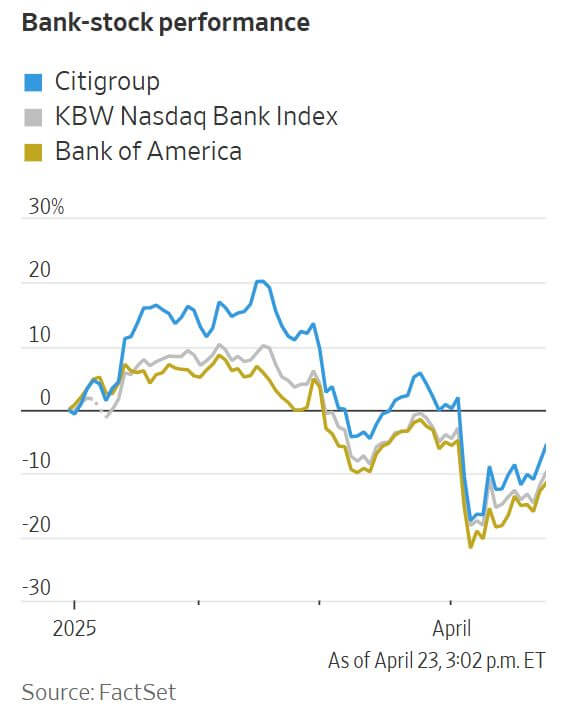

Despite rising public concern over inflation and economic uncertainty, major U.S. banks report that consumer behavior does not yet reflect significant distress. In the first quarter of 2025, Bank of America, Citigroup, and JPMorgan Chase all recorded increased consumer spending, particularly through credit and debit cards. Bank of America’s CFO Alastair Borthwick emphasized that continued consumer expenditure underpins a still-robust U.S. economy. JPMorgan observed that some spending may have been preemptive, as consumers attempted to avoid future price hikes. While consumer sentiment sharply declined in April, driven by market volatility and recession fears, bank executives caution against overinterpreting short-term trends.

In contrast, corporate clients are showing signs of retrenchment. Citigroup CFO Mark Mason highlighted that companies are fortifying balance sheets and frontloading imports in anticipation of further disruptions. M&A activity has slowed, and capital markets remain challenging. Major credit card issuers are bracing for an economic slowdown, taking proactive steps to manage rising financial risk. Despite strong consumer spending and solid earnings in Q1, companies such as JPMorgan Chase, Citigroup, Synchrony, and U.S. Bancorp are shifting strategies in anticipation of potential deterioration in consumer credit quality. Rising delinquencies—now back to pre-pandemic levels—have prompted JPMorgan and Citigroup to bolster their loan-loss reserves. Synchrony is tightening lending criteria, while U.S. Bancorp is reorienting its credit card business toward wealthier consumers to mitigate exposure to more vulnerable segments. The rationale: the top 10% of earners now account for nearly half of U.S. consumer spending, offering greater stability in uncertain conditions. Spending on discretionary categories such as travel and entertainment is slowing, while minimum payment rates are climbing—both indicators of increasing financial stress. With the potential headwinds facing the cyclically sensitive financial sector, investors may wish to consider reducing exposure to financials until uncertainty subsides regarding the economic outlook.