One of the keys to successful long-term investing is to minimize friction on the portfolio, which primarily comes in the form of expenses such as trading costs, operating expenses, other fees, and taxes. Always competing with the incentive to decrease friction by leaving a portfolio alone is another key to successful long-term investing, and that is to ensure the portfolio characteristics and behavior are consistent with the investment objectives, time horizon and risk tolerance of the investor. This argues for regular rebalancing back to the target weights the investor selected.

Potential causes of a portfolio deviating far from target allocations go beyond market drift impact to include interest and dividends, as well as deposits and withdrawals of cash or securities transfers. But in most cases, drift occurs as individual holdings in a portfolio appreciate or depreciate in value and over time deviate from the initial target allocations. For instance, a holding or strategy that started with a 5% allocation can eventually make up much more than 5% of a portfolio if it has considerably outperformed other assets. A decision must be made whether or not, and in what way, to rebalance a portfolio as it drifts from target.

EQIS employs relative change to trigger a portfolio rebalance and does not arbitrarily rebalance portfolios on a calendar basis. If the actual weight for any strategy drifts from the target weight to the degree that the relative change limit is reached on the upside or downside, a portfolio rebalance is triggered.

Money in or out of the portfolio will often trigger a rebalance. When a portfolio has a cash flow event, the allocation is partially rebalanced, effectively achieved by buying the most underweight sleeve(s) with new contributions or selling the most overweight sleeve(s) for withdrawals. Incoming funds get invested in the sleeve furthest below target until it reaches the intended target weight. If excess incoming funds remain after the sleeve furthest below target is rebalanced, then the system invests incoming funds in the sleeve next furthest below target. The reverse occurs for withdrawals, with funds withdrawn from the sleeve furthest above target.

Additionally, portfolios may be rebalanced upon request by the advisor with trading authority via limited power of attorney or instruction from the investor. Conversely, EQIS will adhere to standing client instruction to not rebalance an account1 and omits from rebalancing all non-model holdings and reserve cash.

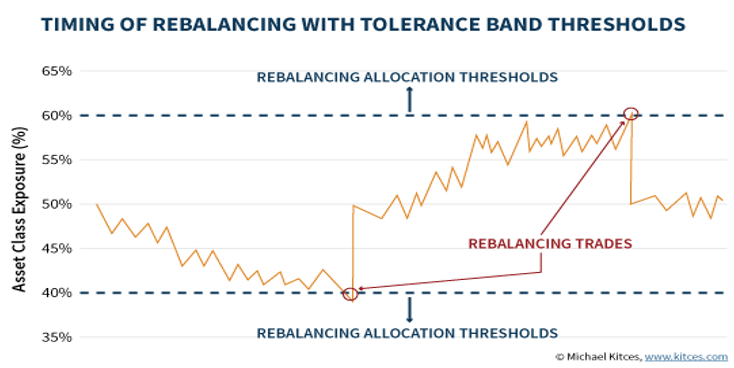

Thresholds allow for a portfolio to benefit from the outperforming asset class without the portfolios total risk elevating beyond the investor’s tolerance. The result of establishing minimum and maximum weights before rebalancing is triggered is that it forms allocation tolerance bands, as illustrated below. In the following chart, a portfolio that was targeting 50% in equities will now trigger a rebalancing trade if the allocation falls below 40% or rises above 60%. Anywhere in between those thresholds and the portfolio remains a buy-and-hold strategy, allowing outperformers to run. When either tolerance threshold is breached to the upside or downside, a sell or buy is triggered, controlling risk.

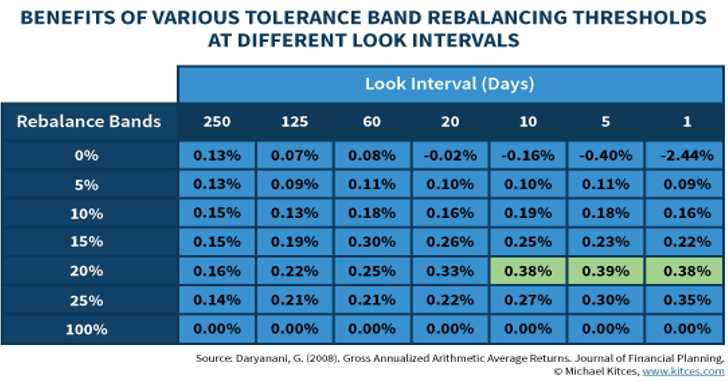

Another notable benefit of this approach is that since only the investment that crosses the threshold needs to be rebalanced, in a multiasset-class portfolio the tolerance band approach will reduce the volume of rebalancing trades. While conceptually the idea of establishing target allocation tolerance bands for rebalancing is relatively straightforward, the question still arises about exactly what the optimal threshold levels would be for those tolerance bands. A 2007 study in the Journal of Financial Planning by Gobind Daryanani entitled “Opportunistic Rebalancing” studied rolling 5-year periods from 1992 to 2004 and found that the optimal rebalancing threshold was at a relative threshold of 20% of the investment’s original weighting, allowing investments to deviate above and below target a reasonable amount without triggering a buy or sell trade. The study also revealed that there should be no limit to the frequency of rebalancing (Look Interval) and instead the investor should “look constantly.”

1 Standing client instruction to not rebalance accounts are only permitted for advisor-built models.

This is intended for informational purposes only and is not an offer to sell securities or provide investment advice. EQIS does not provide tax or legal advice. Investment strategies carry varying degrees of risk to include total loss. The representations and opinions herein are the opinions and view of EQIS and are believed to be reliable but are not guaranteed by EQIS. Other sources may be available which contradict EQIS’s opinion, process, and methodology.

LF1671