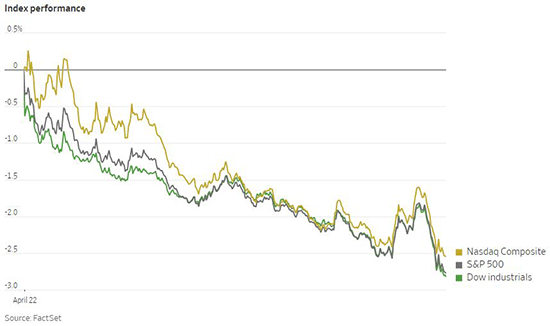

Hawkish rhetoric from the US Federal Reserve weighed on stocks last week, with selling pressure on Friday sending many equity indexes to a third consecutive week of losses. The S&P 500 fell 2.8% for the week, while the Russell 2000 fell 3.2% and the Nasdaq Composite fell a further 3.8%. The Dow Jones Industrial Average posted its worst one-day drop on Friday since October 2020 with a fall of 2.8%. With around a fifth of companies in the S&P 500 reporting results for the quarter so far, around 80% have beat analyst estimates for earnings, according to FactSet. Nine out of eleven sectors in the S&P 500 fell last week, with the worst losses occurring in communication services, energy and materials. Among individual companies, Netflix had a remarkably difficult week. The company’s share price tumbled by 35% after reporting that it had lost subscribers over the first quarter. The yield on the 10-Year US Treasury rose significantly early in the week before settling down to 2.905% on Friday, still near multi-year highs.

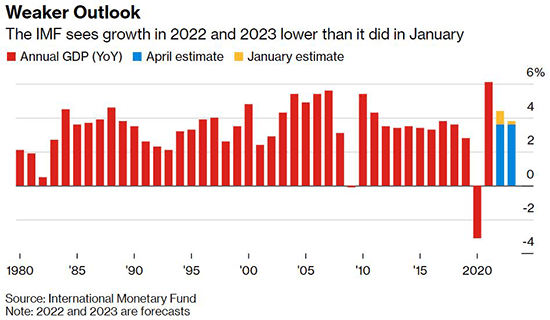

The International Monetary Fund released an update to its World Economic Outlook last week, in which it cut forecasts for economic growth and raised forecasts for inflation. The updated estimates call for global economic growth of 3.6% this year, a significant revision downwards from the 4.4% projection called for in January. The estimate for economic growth in 2023 was revised downward by a smaller amount to 3.6% from 3.8% in the prior forecast. The fallout from the war in Ukraine had a material impact on the euro area, with 2022 growth cut to 2.8% from 3.9% earlier this year. The US received a smaller downgrade for this year to 3.7% from 4%. Meanwhile, continued lockdowns in China due to COVID-19 resulted in a cut in the forecasted growth rate for this year down to 4.4% from 4.8%. Overall, the IMF now forecasts 2022 growth of 3.8% in developed economies and 3.3% in emerging markets, a reduction for both regions. Unfortunately, the IMF also raised its forecasts for inflation this year to 5.7% in developed markets and 8.7% in emerging markets. That is an unwelcome development, but inflation is still expected to moderate next year to 2.5% in developed markets and 6.5% in emerging markets.

The yield on US 10-Year inflation-protected Treasuries (TIPs) briefly traded in positive territory last week for the first time in two years. This shows that the large rise in the nominal US 10-Year Treasury note has been driven primarily by higher real yields, rather than significantly higher inflation expectations. Swaps currently imply that markets are pricing in around 140 basis points of hikes over the next three Federal Reserve meetings. This equates to at least two hikes of at least 50 basis points. The last time the Fed carried out hikes of 50 basis points in consecutive meetings was all the way back in 1984. Positive real interest rates are indicative that markets are normalizing as the extraordinary monetary support of the last two years is withdrawn by central banks. Years of negative real yields meant investors were locked into losses by investing in safe government debt, pushing them towards risk assets such as credit and equities. A return to positive real yields would offer investors an alternative to investing in risk assets. This undermines the case for expensive stocks such as in the technology sector, and a Bloomberg gauge of dollar-denominated investment-grade corporate debt has fallen more than 12% so far this year. Positive US real yields also increases demand for the US dollar, which has strengthened against many currencies in the past month, particularly the Japanese yen.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only. The representations and opinions herein are the opinions and views of EQIS. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. This information should not be relied upon as research or investment advice. EQIS does not provide legal or tax advice.

LF1692