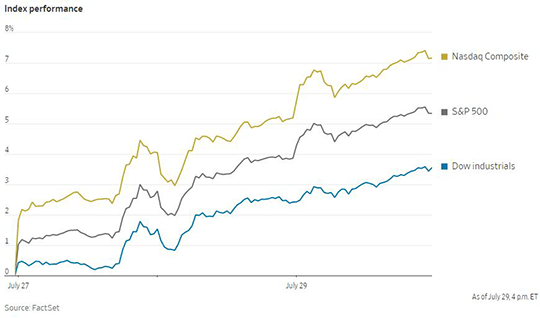

US stocks rose for three straight days last week after the latest meeting by the US Federal Reserve. The S&P 500 ended July up 8.9%, clawing back a significant amount of its losses from earlier this year. Last week was an important one for corporate earnings, with many major large-cap companies reporting results for the second quarter. The selloff in stocks this year was already pricing in a significant slowdown and many major companies have reported earnings that were not as bad as feared. Fully 75% of companies that have reported earnings so far this quarter have beat estimates. Walmart and Procter & Gamble stood out as indicative of the cost pressures facing consumer goods and fell as a result. However, large technology companies including Amazon and Apple reported surprisingly strong revenues, powering the Nasdaq Composite higher. Energy producers including Chevron and Exxon Mobil also posted strong earnings, which resulted in their stock prices being bid higher as well. The yield on the 10-year US Treasury note ended the week down at 2.634%. It is important to note that the yield curve between the 2-year and 10-year Treasury notes has stayed inverted for some time in July. An inverted yield curve has historically been a reliable predictor of future recessions. Some investors have expressed skepticism over whether stocks can hold onto their gains from this relief rally.

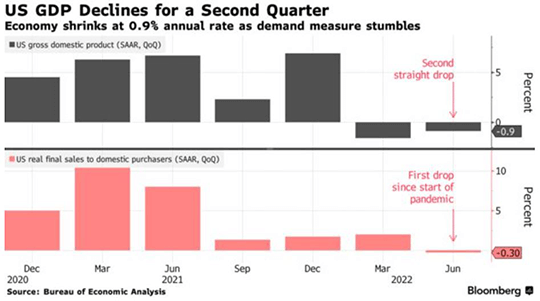

The US Federal Reserve raised the federal-funds rate again last week by 75 basis points. The benchmark interest rate now stands at a target range of 2.25% to 2.5%. The next day, the US Commerce Department released its preliminary estimate for US GDP in the second quarter, showing that the economy contracted at an annualized rate of 0.9%. This is the second consecutive quarter of contraction after economic activity declined at an annualized rate of 1.6% in the first quarter, in large part due to the negative impacts of both trade and inventories. The effects of those components can be stripped out to calculate US real final sales to domestic producers, which is an important gauge of underlying demand in the economy. That figure showed a decline of 0.3% in the second quarter, marking the first drop since the start of the pandemic. Though two consecutive quarters of negative economic growth is sometimes used as the barometer of a recession, the official determination of a recession is made by the National Bureau of Economic Research, which incorporates a wider range of factors. Fed Chairman Jerome Powell stated, “I do not think the US is currently in a recession. There are just too many areas of the economy that are performing too well.” Though typically an economic contraction would be taken as a negative, the Fed took the view that this was a positive development in that the efforts to cool the overheated economy and rein in inflation are beginning to have the desired effect. The Fed also indicated that it may slow the pace of rate hikes if the economy continues to slow. Markets counteractively rallied immediately after the Fed decision on the possibility of slower future rate hikes.

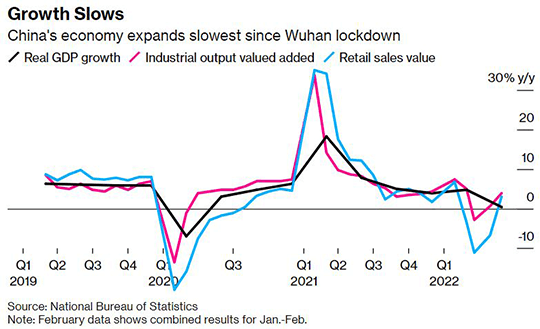

International markets do not present much better prospects for economic growth than the US. The European Union released economic figures for the second quarter that surprised to the upside last week. Second-quarter GDP growth for the Eurozone clocked in at an annualized rate of 2.8% in an acceleration from a 2% annual rate in the first quarter. However, the pronounced risk of a severe energy shortage if Russian natural gas supplies are cut off significantly dampens optimism moving forward. That would open the door to a sharp recession accompanied with high inflation due to soaring energy prices. Eurozone inflation rose to 8.9% in July, and there are estimates that energy prices could push inflation as high as 11.2% in the fourth quarter, meaning that the European Central Bank would have little latitude to ease and support the economy. The Chinese economy looks unlikely to provide much relief either. Chinese GDP rose just 0.4% in the second quarter as major economic hubs such as Shanghai were locked down to halt outbreaks of COVID-19. Though those lockdowns have since been lifted, the government’s zero-tolerance policy toward COVID-19 and the lack of vaccinations throughout the country mean additional waves of lockdowns are entirely possible. The government has stood firm in declining to provide additional stimulus measures, as that policy lever has resulted in the excesses in the property market that the country is still grappling with. Government officials have effectively abandoned the official 5.5% GDP growth target for the year as a result. Goldman Sachs has since revised its growth forecast for China for the year down to 3.3%.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

LF1901