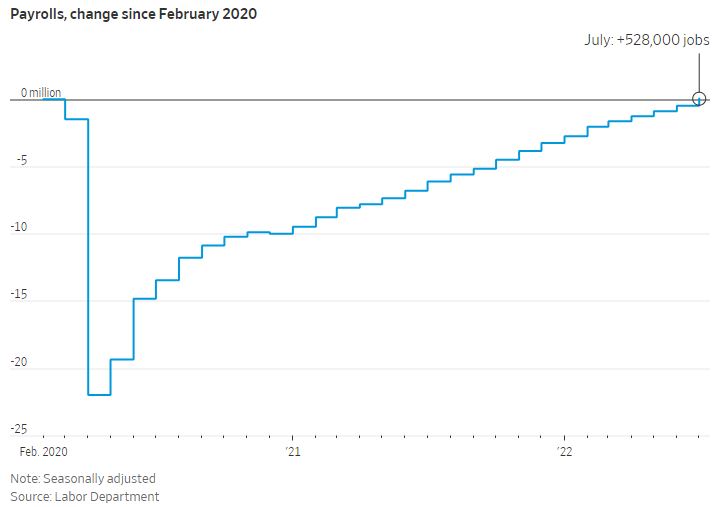

The July nonfarm payrolls report on Friday came in far above estimates, jumping up to 528,000 new positions added for the month. That was above all estimates and roughly double the consensus estimate for 250,000 jobs. The June figure was also revised upward to 398,000 jobs added. The US economy has now recovered all of the jobs lost during the pandemic, in aggregate terms. The unemployment rate has dropped to the 3.5% low last seen in the spring of 2020, matching a 50-year low. Average hourly earnings rose 5.2% last month relative to a year ago in a concerning sign for inflation. Interestingly the labor force participation rate ticked down slightly to 62.1% from 62.2% in June, showing that some potential workers are still not keen to return to the workforce despite high wages, limiting available supply. Hiring was robust across all sectors, with leisure and hospitality, health care and professional services all adding positions. Notably, even interest-rate sensitive sectors such as construction and finance still added workers despite the rapid pace of interest rate hikes from the US Federal Reserve. That makes a stark contrast from recent headlines of layoffs by companies such as Walmart and Ford. The number of available positions did fall in June to 10.7 million from 11.3 million in the prior month, the largest monthly drop in unfilled job openings since April 2020. This indicates that the excessive demand for workers is starting to come down to a degree, but demand for workers is likely to continue to outstrip supply for a good while yet.

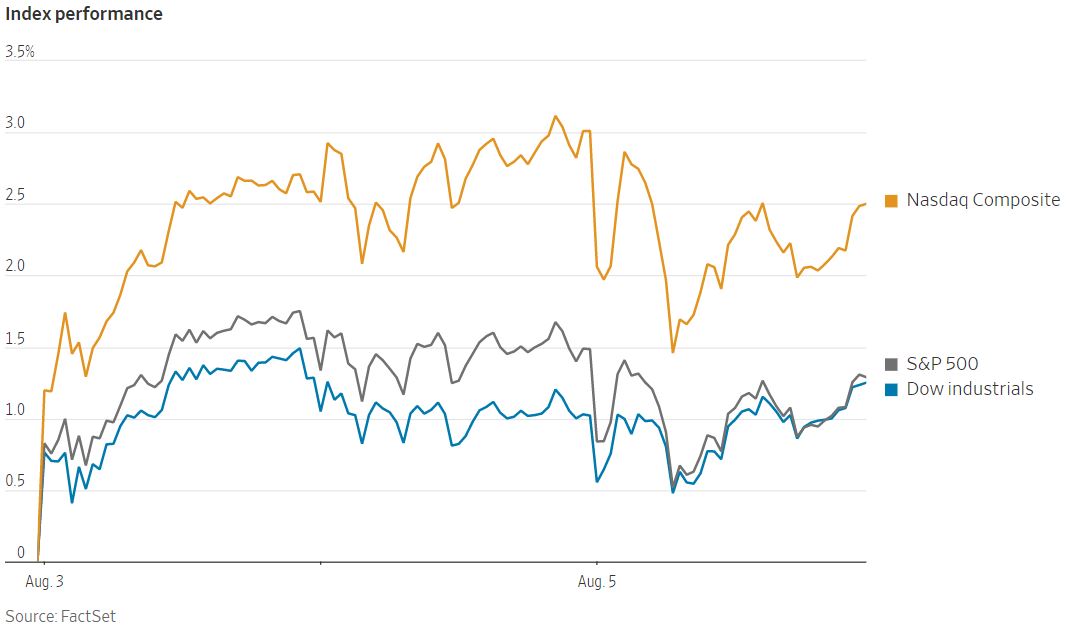

The red-hot jobs report challenges the recent narrative that the economy was slowing based on two consecutive quarters of GDP contraction for the US economy. Stocks and bonds both rallied in July, due in part to the possibility that the US Federal Reserve might ease off the aggressive pace of monetary tightening if the economic data started to cool along with inflation. In this environment, strong economic data may be seen as negative for financial assets, as that may force the Fed to raise interest rates faster and farther to quench inflation. The higher the Fed is forced to raise rates, the more difficult a soft landing for the economy becomes. US stocks fell in the immediate aftermath of the jobs report before paring losses to end the day on Friday. Despite the rocky trading session, the S&P 500 still managed to record its third straight week of gains. Bonds sold off as well on Friday, with the yield on the US 10-Year Treasury note surging to 2.838% from 2.674% the day prior. That yield level is roughly 26 basis points higher than it was on Monday, showing the continued volatility in bond markets this year.

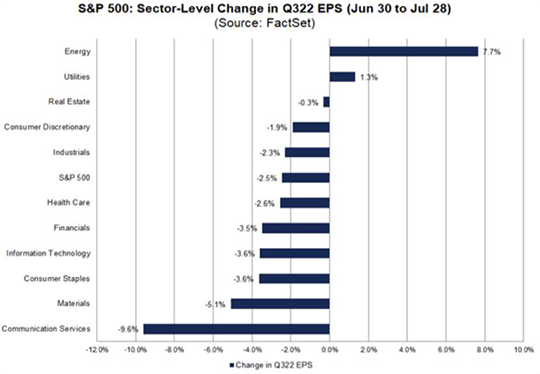

The S&P 500 rallied strongly during the beginning of the second quarter earnings season as corporate profits held up better than had been feared. The roughly 9% rally in the S&P 500 over the last three weeks has been the best start to a quarterly earnings season since 1997. However, forecasts for future earnings per share estimates are being revised downward. Analysts often reduce EPS estimates during the first month of a quarter, but EPS estimates for the third quarter of 2022 were lowered in aggregate by 2.5% over the course of last month, a greater reduction than average. Over the past month, only the energy and utilities sectors have had upward revisions in earnings estimates for Q3, with energy being revised upward by 7.7% and utilities by 1.3%. Q3 EPS estimates for the communication services sector have seen the most severe downward revision at 9.6%. Bottom-up fundamental earnings estimates for the fourth quarter were also revised downward by 2.4%. Looking forward to 2023, EPS estimates for the full calendar year have been revised downward by 2.7% since the end of Q1. The forward 12-month price to earnings ratio for the S&P 500 now stands at 17.1, a significant increase in the valuation multiple relative to its level of 15.8 at the end of June. Earnings will be critical for the trajectory of the stock market, as higher interest rates will put downward pressure on valuation multiples, all else equal.