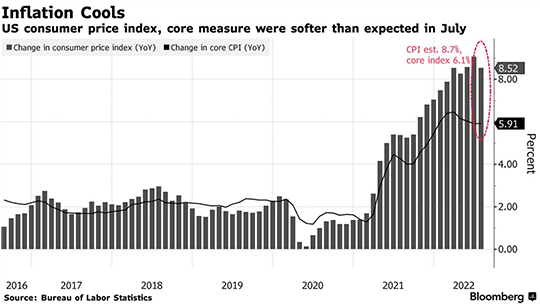

The US Labor Department released updated Consumer Price Index data for July last week showing that inflation slowed more than had been forecast. The headline CPI figure came in at 8.5% compared to a year ago. That is a deceleration relative to the June CPI reading of 9.1% and lower than the consensus forecast. The core CPI figure, which takes out the volatile fluctuations of food and energy prices, came in at 5.9% compared to a year ago, matching the prior month’s annual rate. However, when looking at core CPI in a month-on-month basis, it showed a welcome slowdown. Core CPI rose only 0.3% in July compared to the prior month, less than June’s 0.7% monthly increase. Energy played a large part in the decrease in the headline inflation rate, with gasoline falling 7.7% in July. The prices of hotels, airfares and used cars all dropped compared to the month prior. However, food costs rose 10.9% compared to a year ago, the largest annual increase since 1979. Still, experts forecast that grocery costs are likely to cool in the coming months.

Producer Price Inflation also slowed to 8.9% in July compared to 11.3% in June, indicating that some supply chain pressures may be finally starting to ease. While some of the hallmarks of the “transitory” inflation related to the pandemic slowed, stickier components such as housing continued to rise. Housing costs account for one-third of CPI and two-fifths of core CPI. Housing costs rose 5.7% compared to last year and pushed up overall CPI by fully 1.9% for the month. Thankfully inflation expectations still do not seem to be becoming entrenched with consumers. A recent survey by the Federal Reserve Bank of New York showed respondents’ future inflation expectations fell in July. Clearly the Federal Reserve has a long way to go before it can declare victory over inflation, but this report was a welcome first step in the right direction.

Stocks continued their rally last week as investors speculated that the US Federal Reserve may be able to slow the pace of interest rate increases if inflation continues to moderate from its current high level. The first good news on inflation in months opened the door to the possibility that the Fed may only hike by 50 basis points at its next meeting, though yet another 75-basis point rate hike remains in play. The S&P 500 and Nasdaq Composite both rose for the fourth straight week, recording their longest streak of gains since last November. Meanwhile the Cboe Volatility Index (VIX) slid back below 20 last week, marking the eighth consecutive week of declines in equity volatility. With the second quarter of earnings season winding down, the blended earnings growth rate for the S&P 500 came in at 6.7%. However, that benign aggregate figure is being propped up by the volatile energy sector, which saw earnings rise by 299% for Q2 compared to last year. Excluding the energy sector leaves the rest of the S&P 500 with a decline in earnings for Q2 of 3.7%. This suggests that the recent equity rally is being driven more by perceived shifts in monetary policy rather than equity fundamentals. Investors will be intently waiting for more clarity from the Federal Reserve at its annual conference in Jackson Hole later this month.

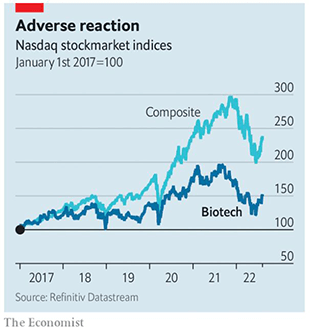

Though equity indexes have rallied broadly in recent weeks, specific sectors are facing unique headwinds. Biotechnology is one industry that benefitted from the COVID-19 pandemic as the world scrambled to develop effective vaccines. However, demand for those vaccines is now waning as fewer people remain unvaccinated. BioNTech indicated that sales fell by 40% in the second quarter. Biotechnology startups are also disproportionally affected by higher interest rates. The value presented by the potential future earnings of a successful medical treatment are worth less as interest rates rise. Those earnings are also highly uncertain, as there are no guarantees that a potential treatment will be successful. Private funding for biotech ventures is down this year, as are the number of initial public offerings in the sector. The sector has sold off this year, though lower valuations may create opportunity for skilled active managers. The semiconductor industry is another sector that benefitted from the COVID-19 pandemic. The shift to remote work and quarantines resulted in increased demand for smartphones, computers and data centers, all of which depend on semiconductors. Despite continued chip shortages, Micron Technology, Nvidia, Intel, and Advanced Micro Devices all reported that demand turned sharply lower in the second quarter. Semiconductor companies have been investing in increased capacity and the US Congress just passed a $52 billion stimulus package to increase production as well. Analysts with Citigroup note that it is possible that a large supply will come to market just as demand is waning, resulting in a glut. Though semiconductor stocks did participate in the July rally, they have since sold off sharply.