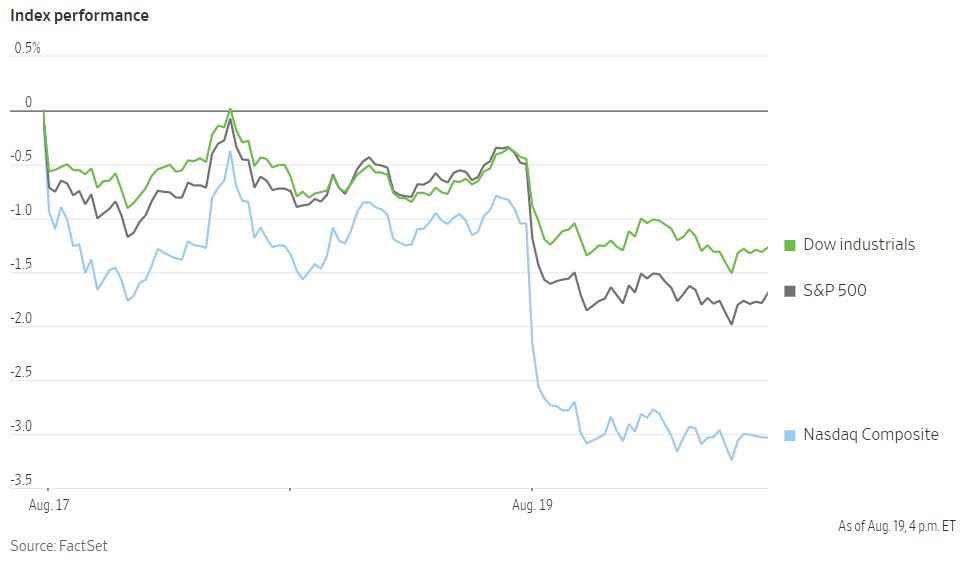

The US Commerce Department released retail sales data last week for July, showing that spending was flat for the month. That was a positive result overall, considering that spending at gas stations fell 1.8% as gasoline prices fell back below $4 per gallon over the month. Gasoline spending typically constitutes roughly 10% of retail spending. Stripping out the impact of gasoline and autos, retail spending rose 0.7% last month. However, the good news from continued consumer spending was ultimately outweighed by resurgent fears over the path of interest rates. Minutes were released of last month’s monetary policy meeting of the US Federal Reserve, showing that officials thought that it might be appropriate to slow the pace of rate hikes if inflation continues to moderate. Officials also noted that they may be forced to continue raising rates further if inflation remains stubbornly high. Though that shouldn’t have come as a surprise to anyone, the rally in US assets stumbled to end the week. The S&P 500 fell 1.1% on Friday, while the Nasdaq Composite dropped 1.9%. Both indexes declined for the week, snapping their prior streak of four consecutive weeks of gains. The yield on the 10-year US Treasury note rose to 2.978% on Friday.

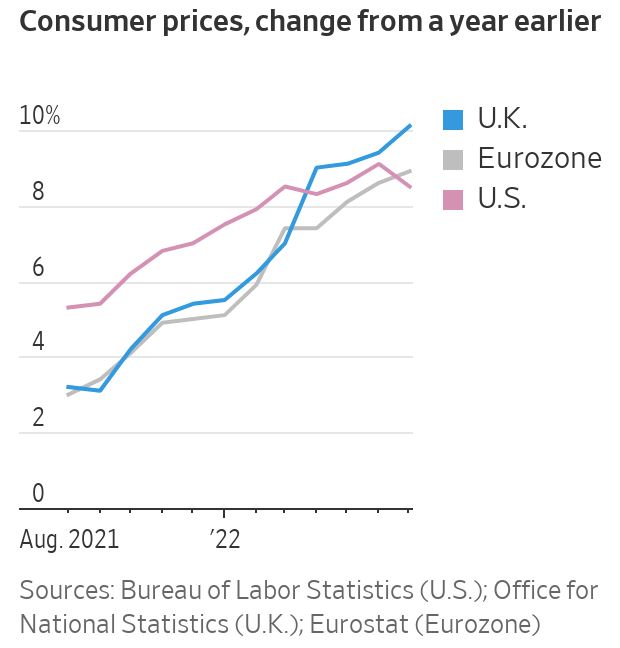

Inflation in the US eased slightly in July to an annual rate of 8.5%. However, inflation in Europe continues to accelerate, in large part due to surging energy prices. Eurozone inflation rose to 8.9% in July compared to a year ago, an increase relative to June’s annual rate of 8.6%. Energy prices alone rose 39.7% in July relative to last year across the Eurozone due to the region’s vulnerability to changes in the flows of Russian energy exports. The UK meanwhile saw inflation surge even higher to 10.1% in July. The Bank of England estimates that inflation will continue to accelerate to as high as 13% by the end of this year. The UK faces a particularly gloomy outlook for inflation due to the continuing effects of Brexit, which both increased the costs of imports and limited the availability of foreign workers, further pushing up wages. Other European countries including Spain and Greece have already seen inflation hit double digits as well. Eurozone governments came to a non-binding agreement to voluntarily reduce energy consumption by 15% through next spring, though it remains to be seen if that will be sufficient to keep heavy industry running. Russia supplied roughly 40% of Europe’s natural gas before the invasion of Ukraine, but that amount has since fallen to 15% as Russia has cut supplies to apply diplomatic pressure. The high inflation may force central banks to tighten monetary policy aggressively, risking tipping the region into recession.

New economic data out of China for July indicated a broad slowdown and fell short of economists’ estimates across the board. Retail sales, property sales, industrial output, and investment all fell for the month. This suggests that the combined pressures of the property slump and COVID-19 lockdowns may be snowballing into a broader crisis of confidence among consumers and businesses. Exports of goods had provided support to the Chinese economy over the last few years, but that momentum may be fading now as well. Many retailers overstocked on supply in the last year and consumers are increasingly shifting spending from goods to services. Factory orders in China from foreign customers are now seeing sharp reductions. Orders for clothing and textiles have been cut by as much as 30% in just the last month, while some furniture exporters have seen demand slashed by as much as 50% compared to last year. So far, the government’s policy response to the weakening data has been tepid at best. The central bank last week announced a surprise rate cut of 10 basis points to both its one-year and seven-day interest rates. However, with demand for credit already so weak, it is unlikely that such a limited easing of monetary policy will have a material impact. Local government entities have already issued most of the bonds they were allocated for the year for infrastructure spending and it is unclear if they will be permitted to issue additional debt by the central government. Total government debt in China as of the end of last year stood at 120% of GDP, indicating that government debt had doubled since just 2014. That large debt burden is making the government think twice about turning on the fiscal taps once again.