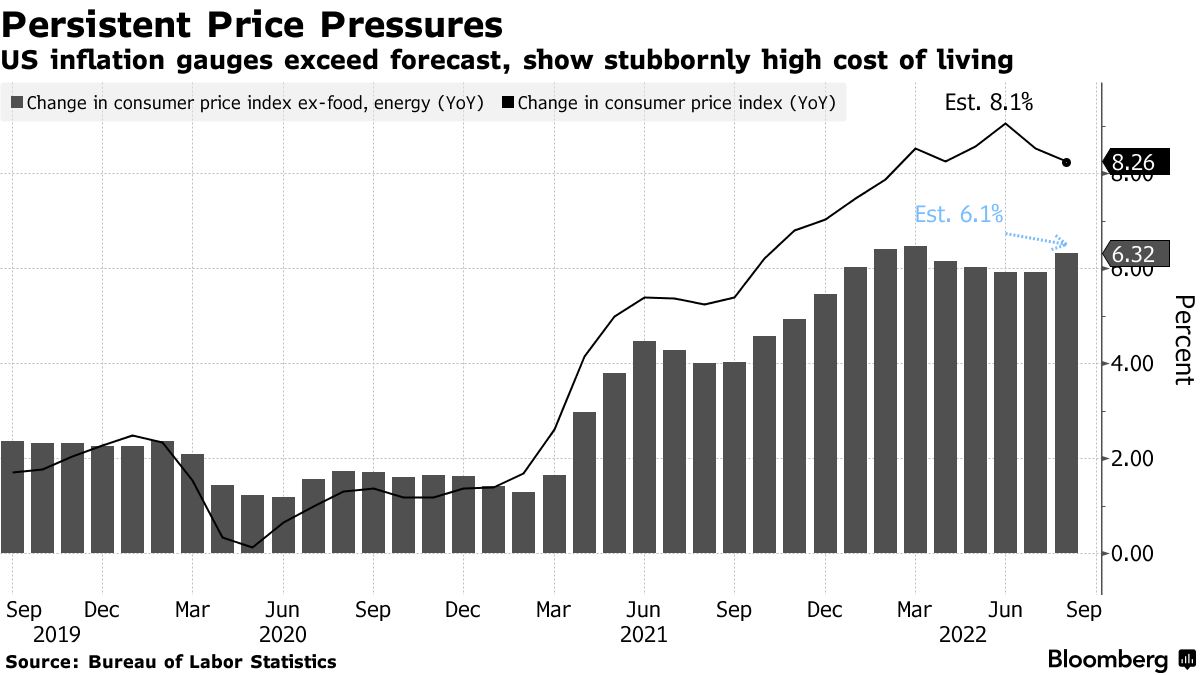

The latest release of the Consumer Price Index (CPI) by the US Labor Department last week was a negative surprise for markets, when CPI rose 8.3% in August compared to a year ago. This was the second month of decline in the headline inflation rate since it peaked in June at 9.1%, in part due to easing energy prices. However, core CPI, which excludes volatile food and energy prices, surpassed expectations with a 6.3% increase in August relative to a year ago. Core CPI rose by 0.6% in August compared to the prior month, doubling July’s monthly rate and the median economist estimate. Core CPI is typically seen as a more reliable indicator for underlying price pressures and is more closely watched by central banks. A major contributing factor last month was a 0.7% increase in shelter costs, the largest monthly jump since 1991. Though some leading indicators suggest rents may plateau in the coming months, they are likely to remain elevated at least through next year. That will likely push up inflation, as shelter costs comprise roughly one-third of the Consumer Price Index. Meanwhile, initial jobless claims fell for the fifth straight week showing that demand for labor remains strong. Consumer spending rose 0.3% in August compared to the prior month in an indicator that spending remains robust in the face of high inflation. Taken together, the August data suggest that the US economy is still running too hot.

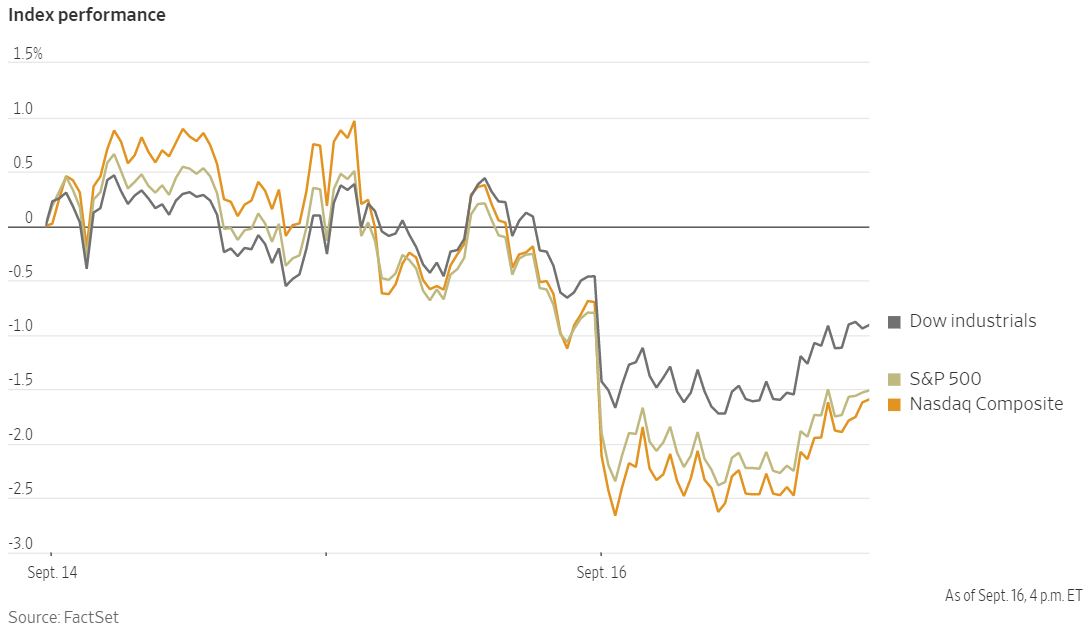

The bad news on inflation increased expectations that the US Federal Reserve will be forced to hit the brakes harder and longer to bring inflation under control, risking damage to the economy. The market is now fully pricing in an interest rate hike of at least 75 basis points at the next Federal Open Market Committee meeting this week. The yield on the two-year US Treasury note rose to its highest level since 2007 on Thursday and finished the week at 3.859%. The yield on the 10-year US Treasury note ended the week at 3.45% and remains lower than the yield on the two-year note. This inversion of the yield curve has historically been a reliable leading indicator for an impending economic recession. The impact on US equity markets was severe and major indices had their largest weekly losses since June. The Dow Jones Industrial Average fell 4.1% for the week, while the S&P 500 lost 4.8%. All 11 sectors of the S&P 500 had substantial losses for the week, with materials, communication services and technology services all losing at least 6%. The Nasdaq Composite dropped 5.5% for the week.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

LF1996