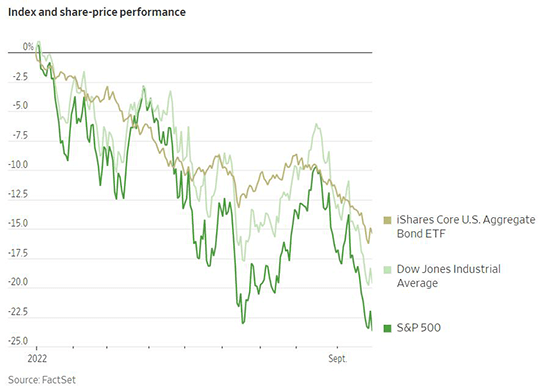

The final day of the third quarter saw the most recent release of the Personal-Consumption Expenditures price index, which is the US Federal Reserve’s preferred gauge of inflation. Headline PCE rose 6.2% in August compared to a year ago, slower than July’s 6.4% rate. However, core PCE, which excludes volatile food and energy prices, accelerated to 4.9% in August compared to last year. This represents a worrying increase in price pressures in comparison to the 4.7% core PCE rate in July and mirrored trends in the Consumer Price Index. The continued increase in core inflation makes it more likely that the Fed will continue to raise interest rates for the near future, despite risking damage to the economy in the process. This final bit of unwelcome news pushed major equity indexes down for the week. The Dow Jones Industrial Average entered a bear market last Monday and is now down 21% for the year. Meanwhile, the S&P 500 fell below its prior low from before the short-lived summer rally and is now down 25% year to date. The Nasdaq Composite, whose technology companies are particularly sensitive to interest rates, has fallen 32% so far this year. International stocks have not fared any better, as an MSCI index of global equities outside the US also fell 11% during Q3 and is down 28% YTD. Bonds have also sold off again alongside stocks in the recent downward trend in financial markets. The iShares Core US Aggregate Bond ETF fell 5% during the quarter and is down 15% so far this year.

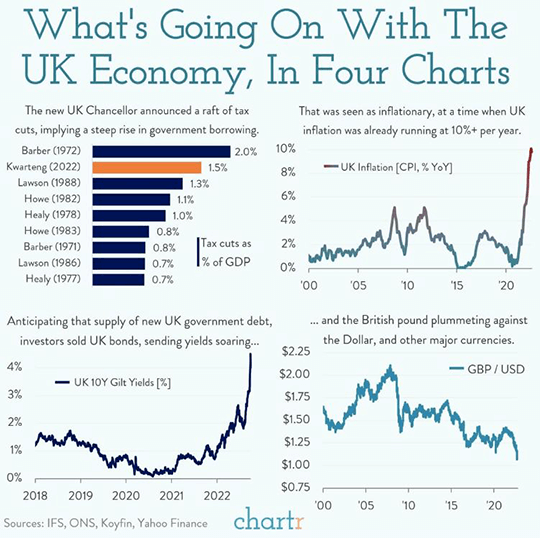

While the United Kingdom certainly is not alone among countries in facing serious macroeconomic headwinds, its position has been uniquely precarious due to a series of political missteps. Investor concerns about the trajectory of the UK economy escalated into a full crisis of confidence last week following the announcement of a budget plan by the administration of new Prime Minister Liz Truss. Despite the economy already being saddled with double-digit inflation, the new budget called for large tax cuts that would require some of the largest increases in debt issuance in the history of the UK. Such large tax cuts would act to stimulate the economy at a time when the central bank is already trying to slow the most serious outbreak of inflation in decades. Investors headed for the exits in spectacular fashion, with selling pressure sending the British Pound to near parity with the US dollar. UK government bonds also sold off dramatically, with the yield on the 10-year gilt soaring to near 5%. The 30-year gilt fell by an astounding 24% over the course of the week, threatening financial contagion through UK pensions’ exposure to long government bonds. The severe selloff also had spillover effects outside the UK, with selling in US government bonds sending the yield on the 10-year US Treasury note above 4% for the first time in more than a decade. The Bank of England was forced to intervene on Wednesday, pledging to buy long UK government bonds at whatever scale necessary to restore stability in financial markets. That extreme emergency measure proved sufficient to calm the bond rout for the time being, and the 30-year gilt recovered much of its losses by the end of the week. The 10-year gilt finished the week with a yield back near 4%, while the 10-year US Treasury note ended the week with a yield of 3.73%.

The representations and opinions herein are the opinions and views of EQIS Capital Management, Inc. ("EQIS"), a registered investment adviser. The information is believed to be reliable but is not guaranteed by EQIS. The information contained herein is for informational and comparison purposes only and should not be relied upon as research or investment advice. When applicable, sources used in forming EQIS’s opinion are cited, however other sources may be available which contradict EQIS’s opinion, process and methodology. While EQIS believes the data to be reliable, no representation is made as to, and no responsibility, warranty or liability is accepted for the accuracy or completeness of such information. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future events. EQIS does not provide legal or tax advice.

MT-305281