The September Consumer Price Index (CPI) print last week showed that higher interest rates from the US Federal Reserve are yet to have a meaningful impact in reigning in inflation. The headline CPI rate for September relative to a year ago came in at 8.2%. That continues the lower trending in headline CPI since it peaked in June at 9.1%, in part due to lower energy prices since this summer. However, the Fed is more concerned with core CPI, which strips out the effects of volatile food and energy prices and is regarded as a more reliable indicator for underlying price pressures. Core CPI rose 6.6% in September compared to a year ago, marking the largest increase in core CPI since 1982. Compared to the month prior, core CPI rose 0.6% in September, matching the monthly inflation rate in August. Meanwhile, the Producer Price Index (PPI), which measures the prices charged by suppliers, rose 0.4% in September compared to the month prior after falling by 0.2% in August. Core PPI, which excludes food, energy and supplier margins, rose 0.4% in month-on-month terms as well, also an acceleration from the 0.2% increase in August. Consumers are still keeping pace with inflation, shown by flat US retail spending in September compared to the month prior. Taken together, these data points paint the picture of an economy that is still running too hot, making it unlikely that the Federal Reserve will slow its campaign of interest rate hikes any time soon.

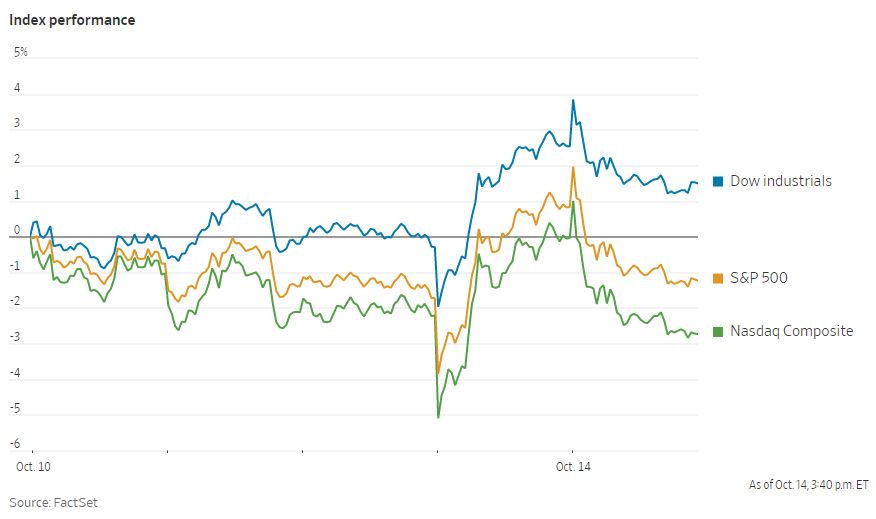

Domestic equities endured another volatile week of trading in the wake of updated inflation data. Stocks drifted between moderate gains and losses to start the week before selling off sharply after the September CPI release on Thursday. However, stocks then rallied back sharply in a counterintuitive move, likely due to investors covering crowded short positions. The wild swings in the market on Thursday were the first time that the Dow Jones Industrial Average had both fallen at least 500 points and risen at least 800 points in a single trading day. Ultimately, stocks fell again Friday to finish the week. The S&P 500 ended the week with a loss of 1.5% while the Nasdaq Composite fell by 3.1%. Meanwhile, the Dow held onto enough of its Thursday rally to end the week up 1.2%. Another hot inflation report prompted Fed officials to speculate that the terminal interest rate may need to go even higher to cool inflation. The prospect of higher interest rates weighed on bonds, with the yield on the 10-Year US Treasury note ending the week up at 4.005%. That marks the first time since 2008 that the 10-Year closed with a yield above 4%.