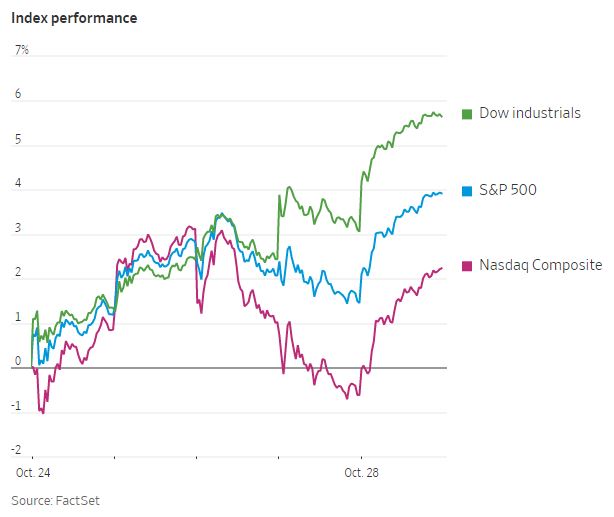

The mega cap technology companies that powered equity indexes higher during the pandemic have now shifted to being the laggards, with many major technology companies reporting disappointing earnings last week. Amazon projected that sales for the current quarter would be well shy of prior estimates, while sales growth in the cloud-computing sector slowed at both Microsoft and Amazon. Digital advertising sales declined for both Alphabet and Meta, which resulted in shares in the Facebook parent falling sharply to multi-year lows. Apple was the exception to the rule, reporting record revenue. However, those disappointments were offset by relatively strong results in other sectors, including real estate, financials and consumer staples. Exxon Mobil and Chevron reported some of their highest quarterly profits ever, while industrial giant Caterpillar also had strong results. So far for the quarter, blended projected and reported earnings results reported by FactSet are showing year-over-year earnings growth of 2.2%. While still positive, that is the slowest quarterly earnings growth since 2020. The Dow Jones Industrial Average recorded the strongest gains for the week, followed by the S&P 500. The strong results from Apple were sufficient for even the Nasdaq Composite to notch a gain for the week.

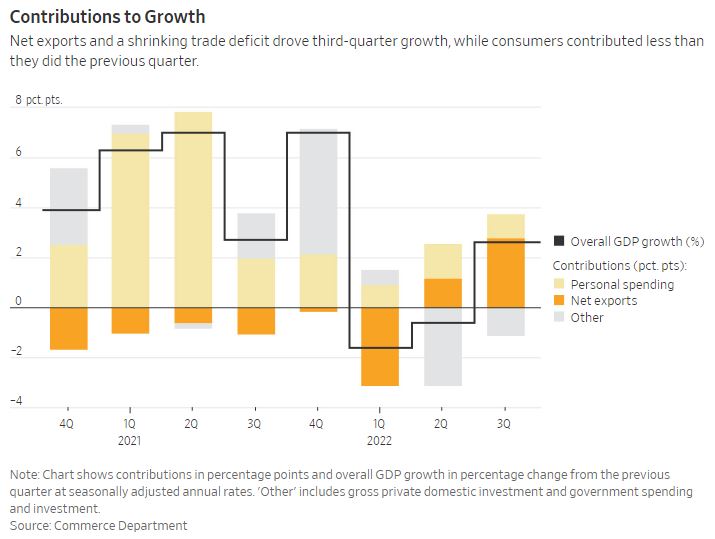

Last week also saw a flurry of updated macroeconomic data on the trajectory of the US economy. The US Commerce Department reported that gross domestic product (GDP) grew at an annualized rate of 2.6% in the third quarter, powered higher by strong net exports. Finals sales to private domestic purchasers, which measures combined consumer and business demand, was barely positive at 0.1%. That is a continued deceleration from an increase of 0.5% in Q2 and 2.1% in Q1. Consumer spending rose by a seasonally adjusted 0.6% in September but was accompanied by a lower savings rate and higher credit-card balances, indicating that consumer strength may be approaching its limits. Meanwhile, the core personal consumption expenditures index, which is the US Federal Reserve’s preferred gauge of inflation, rose 5.1% relative to a year ago. That marks an acceleration relative to the prior month. These data points make it likely that the Fed will raise interest rates by 75 basis points yet again this week. While it is still unknown if the Fed will be able to reign in inflation without triggering a recession, bond markets flashed an important recession indicator for the first time last week, as the spread on yields between the three-month US Treasury bill and the 10-year US Treasury note finally inverted. An inversion in that yield spread has preceded every US recession since 1950, except for one false alarm in 1967.