The possibility that the Federal Reserve may have the leeway to slow the pace of interest rate hikes moving forward sparked a ferocious rally across markets last Thursday. Prices of US government bonds surged, with the yield on the two-year US Treasury note falling to 4.324% from 4.628%, its largest one day move since 2008, and the yield on the benchmark 10-year US Treasury dropping from 4.149% to 3.828%, marking its best single-day performance since 2009. Stocks staged a dramatic rally as well, with the S&P 500, Dow Jones Industrial Average and Nasdaq Composite all recording their best single-day gains since 2020. The S&P 500 surged by 5.5% on Thursday alone, while the Nasdaq Composite jumped by 7.4%. US stocks added to those gains on Friday, powering higher despite news of the bankruptcy of major cryptocurrency exchange FTX. The technology sector of the S&P 500 saw a gain of 10.89% for the week, while communication services and basic materials both had weekly gains above 8%.

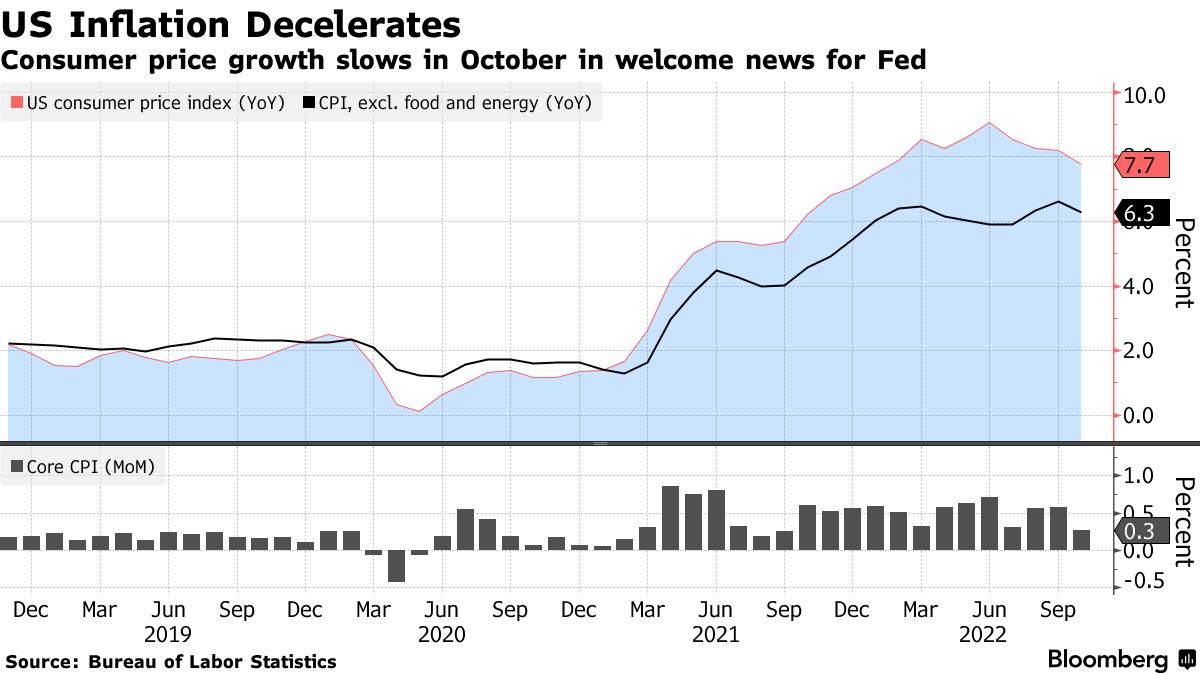

There was finally some good news on the inflation front last week, as the October Consumer Price Index (CPI) data showed that prices rose less than had been forecasted. The US CPI rose by 7.7% in October compared to a year ago. Though that is still a rapid clip, it constituted a significant deceleration from September’s 8.2% annual increase. The core CPI, which excludes volatile food and energy prices, rose 6.3% compared to a year ago. That was also a deceleration from September’s 6.6% increase, which represented the largest annual increase since 1982. One of the most promising data points was the month-on-month core inflation rate, which came in at 0.3%, much lower than the 0.5% forecast and was a welcome relief from the 0.6% increase seen in both September and August. Goods prices continued to ease last month, while the prices of services rose, in part due to a large increase in shelter costs. However, shelter costs have a significant lag in the Labor Department data, and more current indicators suggest rents are stabilizing or even starting to decline. That suggests that shelter inflation may eventually ease as well, though it may not come through in the CPI data until next year. The October CPI report was an encouraging step in the right direction after months of inflation surprises to the upside of forecasts. Though inflation is still too high for comfort for the US Federal Reserve, futures prices now imply that a smaller interest rate hike of 50 basis points is much more likely in December than another hike of 75 basis points.