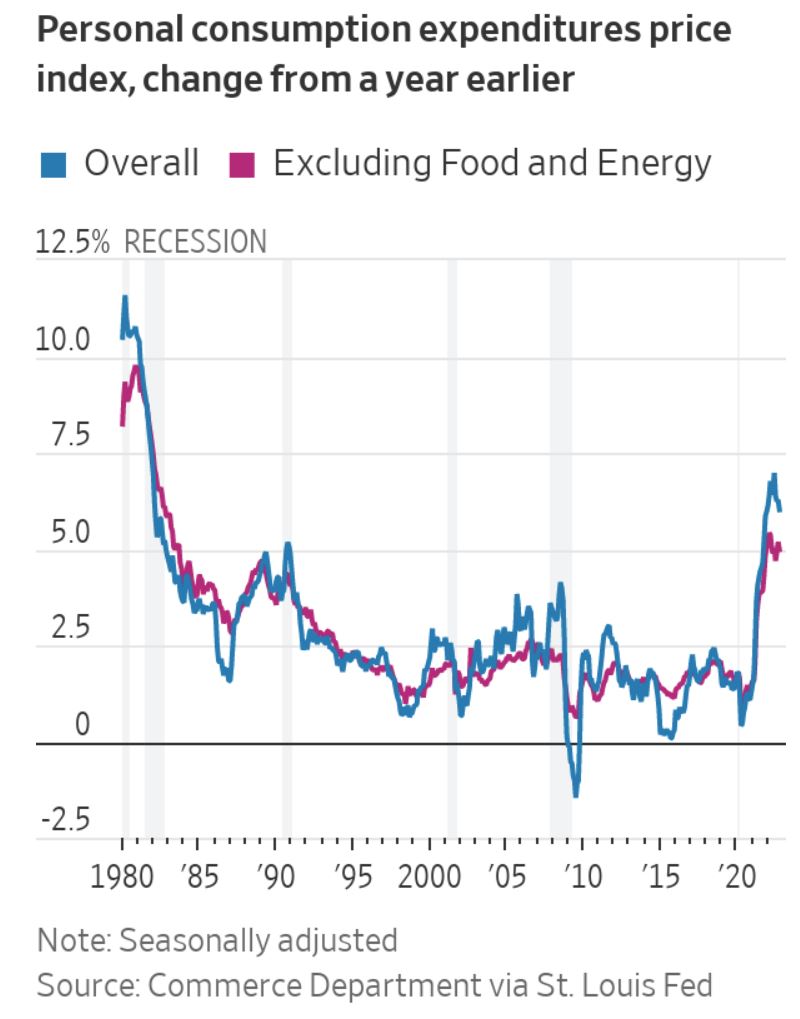

A flurry of new economic data releases last week gave investors and Fed watchers a mix of good and bad news regarding the path of interest rates. US GDP growth for the third quarter was revised upward from 2.6% to 2.9% as the economy continues to withstand higher borrowing costs. Consumer spending for October rose 0.8% compared to the prior month, showing US households are still able to spend despite high inflation. The Personal Consumption Expenditures (PCE) Index, which is the Fed’s preferred measure of inflation, rose 6% in October compared to a year ago, slowing from 6.3% in September. Core PCE, excluding volatile food and energy prices, rose 5% in October compared to a year ago, also a welcome deceleration from the prior month’s 5.2% annual rate. Federal Reserve Chairman Jerome Powell gave investors further cheer in a speech Wednesday when he suggested that the Fed may increase interest rates by only 50 basis points at its December meeting, after four consecutive hikes of 75 basis points. Through the middle of the week, the various data points boosted the narrative that the Fed might be able to engineer a soft landing as some inflation pressures ease, though that thesis very much remains up for debate.

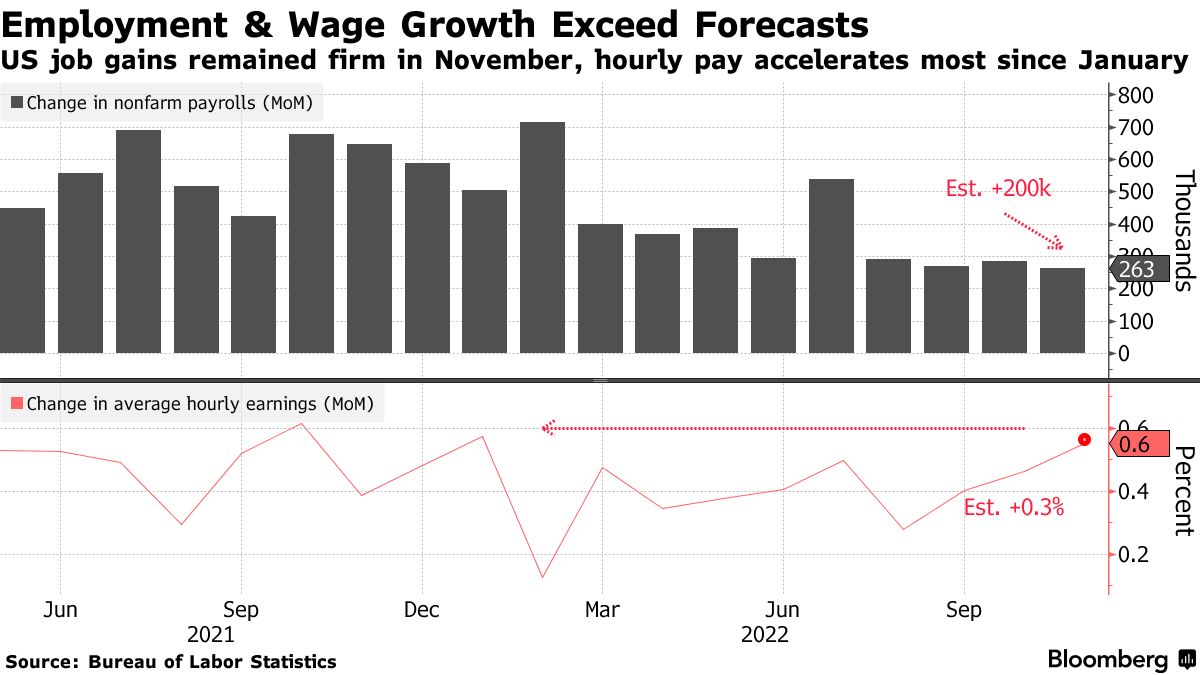

The November jobs report released on Friday delivered a sobering view of the current state of the labor market. Despite recent headlines of layoffs in the tech industry, employers added 263,000 new positions last month, well above consensus estimates. The unemployment rate held steady at 3.7% while average hourly earnings surged by 0.6% compared to the prior month, again well above estimates. Wages rose 5.1% compared to a year ago. Tellingly, the labor force participation rate decreased to 62.1%, its lowest rate in four months. For comparison, the labor force participation rate stood at 63.4% in February of 2020. Powell highlighted the issue of lower labor force participation in a speech last Wednesday, indicating that there is currently a shortfall of roughly 3.5 million workers following the COVID-19 pandemic. Fed economists indicated that roughly 2 million of those missing workers can be attributed to early retirements. The remaining 1.5 million of the shortfall in workers was attributed to the surge in deaths during the pandemic and lower net immigration. Net immigration slowed drastically as result of government policy under the Trump administration, and then collapsed further during the pandemic. Net immigration to the US during the 12 months ending on June 30th 2021 fell to just one quarter of its level in 2016. The fundamental shortage of workers now seen in the US is a structural issue that will be difficult to solve with the blunt instrument of monetary policy. Higher wages for scarce workers may prove to serve as a floor for inflation for some time, even as other sources of price increases such as demand for goods and supply chain issues ease.

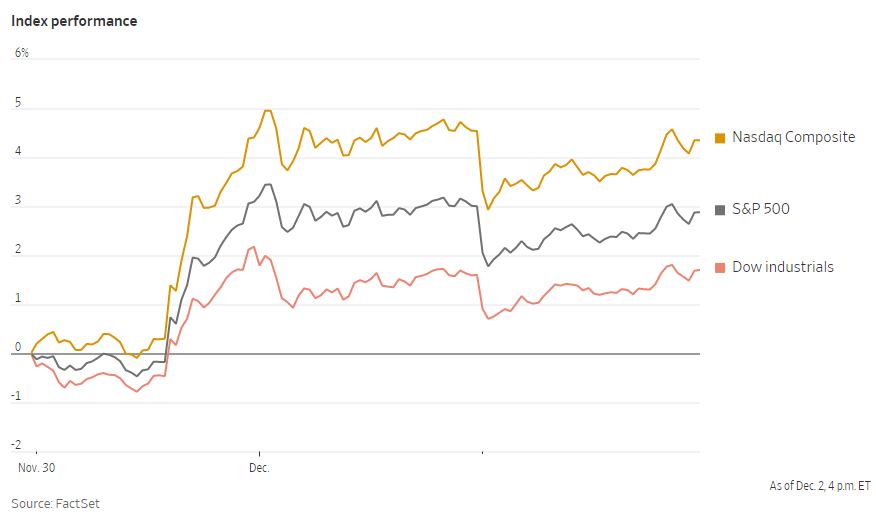

Markets rallied strongly last Wednesday following Powell’s speech on increased expectations that the Fed would begin slowing the pace of interest rate increases at its next meeting later this month. The Dow Jones Industrial Average rallied by 2.2%, pushing it back into a bull market after rising 20% from its prior low. The interest-rate sensitive stocks in the Nasdaq Composite reacted even more emphatically, surging by around 5%. The reality check delivered by the strong jobs report saw stocks and bonds sell off on Friday, though they clawed back those losses in the afternoon and ended the day roughly flat. Despite the turbulence, equities held onto a gain for the week. The yield on the 10-year US Treasury note ended the week at 3.517%. Though the robust jobs report is unlikely to change the outcome of the next Fed policy meeting, traders did adjust the implied terminal interest rate upward to as high as 4.98% before pulling back slightly. The Fed policy rate is currently set at the range of 3.75% to 4%.