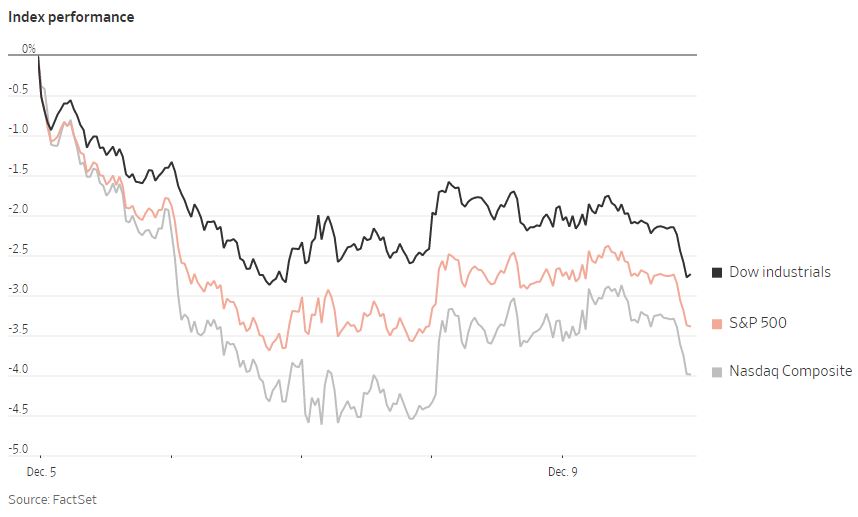

The supply side of the US inflation problem received an update last week with the release of the November Producer Price Index, which rose 7.4% in November compared to a year ago. That was above expectations, but represented a decrease from the 8.1% annual increase seen in October. Looking at PPI in month-on-month terms, November’s PPI rose 0.3%, holding steady at the same rate seen in the last two months. Services prices drove most of the increase, while goods rose by a smaller margin. Notably, core PPI, which excludes volatile food and energy prices as well as supplier margins, rose 0.3% in November compared to a month prior, an increase compared to the 0.2% core rate seen in October. The PPI figures were sobering for US equity investors, with all three major stock indexes falling for the week. The S&P 500 gave up 3.4%, while the yield on the US 10-Year Treasury note rose on Friday to end the week at 3.567%. The November Consumer Price Index figures will be released on Tuesday, giving a final data point in advance of the December US Federal Reserve meeting on Wednesday.

This has been a very difficult year for investors in Chinese equities due to the regulatory crackdown on technology companies, the troubles in the property market, and the government’s zero-Covid policy. However, equity markets have rallied recently based on speculation that the government would be easing its draconian approach to containing the pandemic. Since the beginning of November, the Hang Seng Index of Chinese stocks listed in Hong Kong has rallied more than 30% from its recent low, though it remains down around 17% year to date. After being pressured by rare protests against the continuing lockdowns, the government suddenly abandoned the major policies that underpinned its restrictive approach to the pandemic on December 7th. That about-face comes just as daily cases of COVID-19 stand at 30,000, a high level for China. The lunar new year is approaching, which may see many people travel to see their families, despite the fact that only 40% of the elderly are fully vaccinated. It remains to be seen if the government will remain committed to this shift in policy if cases and deaths soar. There have been many false starts and reversals in Chinese government policy this year, which will likely contribute to ongoing volatility for Chinese markets for the foreseeable future. Nomura recently downgraded its forecast for Q4 China GDP growth to 2.4% from 2.8% and lowered its estimate for growth next year to 4% from 4.3%.

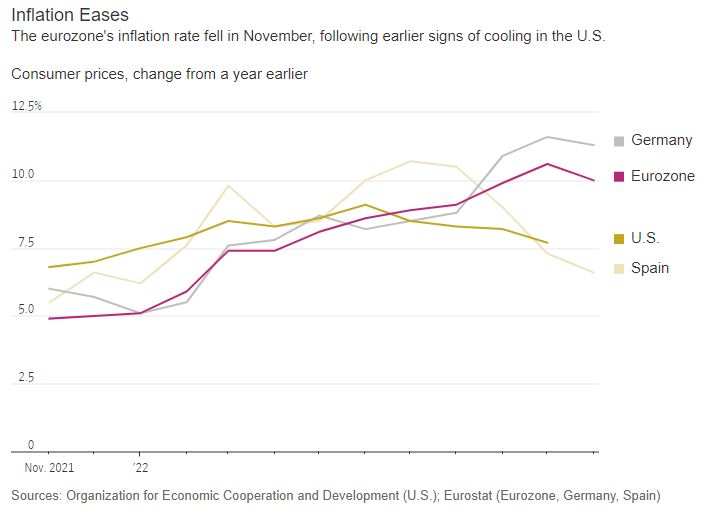

While the headline rate of inflation has been cooling in the US for some time, it had continued to soar in Europe through the summer and fall. That has been largely due to the shock of higher energy prices in the Eurozone because of the sudden discontinuation of energy supplies from Russia. Thankfully, the Eurozone saw its annual inflation rate fall to 10% in November in the first decrease since 2021. However, European Central Bank President Christine Lagarde indicated that she believed that this was just a blip and not a peak in inflation. Energy prices in Europe had eased in the fall in part due to lower than expected demand because of unseasonably warm weather. This most recent November was the fifth warmest on record, which enabled European Union gas inventories to reach a peak of 95% maximum capacity. Now as the weather turns colder in December, demand for natural gas is surging, as consumer demand for heating accounts for roughly 36% of gas demand in Europe. Last week, demand for natural gas rose by 44% in comparison to the prior month. This makes it likely that energy prices will begin to rise again and may result in higher inflation next month. Analysts are estimating that the ECB will raise its benchmark interest rate by 50 to 75 basis points at its next meeting on December 15, which would mark its fourth straight hike.