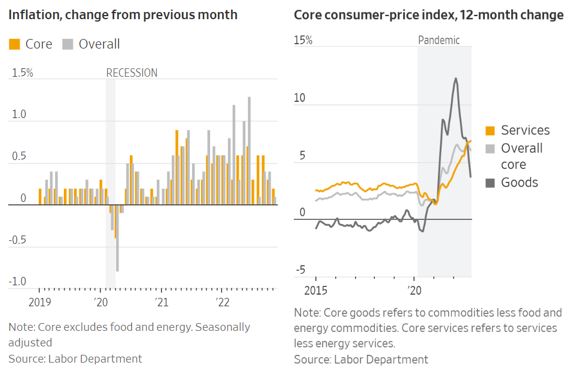

The release of the November Consumer Price Index (CPI) figures last week showed that US inflation continued its recent easing trend. Headline CPI rose 7.1% last month compared to a year ago in a significant slowdown from October’s 7.7% annual rate. Core CPI, which excludes volatile food and energy prices, rose 6% compared to a year ago, its second consecutive month of cooling since peaking at 6.6% in September. It is valuable to look at the changes in inflation in month-on-month terms as well, as that strips out noise to provide a clearer view of the current inflation dynamics. CPI rose just 0.1% in November compared to the prior month, slowing form 0.4% in October. Core CPI rose 0.2% in November compared to a month ago, also a slowdown from the 0.3% rate seen in October. The makeup of core CPI gives reasons for optimism as well. Goods prices are rising at a much slower pace as supply chain bottlenecks resolve and consumer demand normalizes. Goods prices may soon be falling outright. Services outside of housing and health insurance added less to core inflation in November compared to prior months. Shelter costs are still rising but are calculated with a lag in CPI. Current indicators show housing prices and rents are falling, suggesting that shelter costs will eventually add disinflationary pressure to CPI in the coming year. These are all welcome trends, but the tight labor market and rising wages may put a floor under inflation for the foreseeable future.

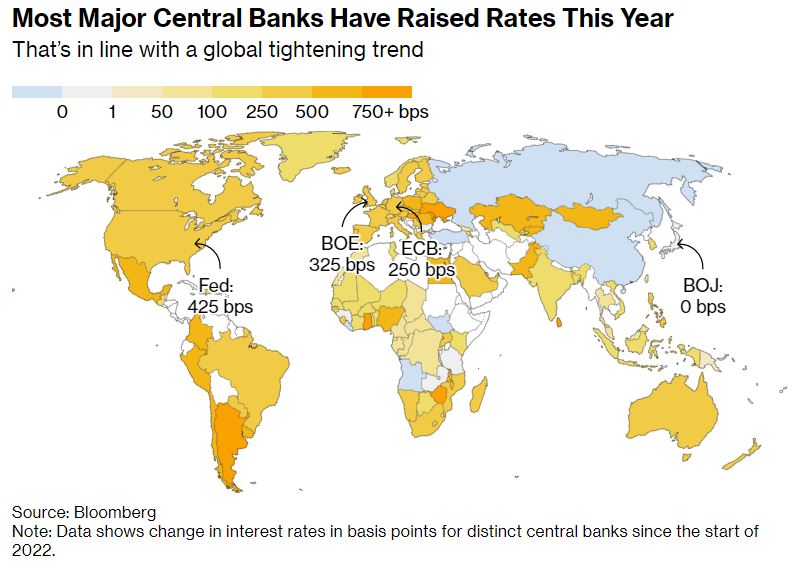

Major central banks in the US and Europe all raised interest rates last week, but their trajectories may diverge moving forward. The US Federal Reserve raised the benchmark federal funds rate by 50 basis points as was widely expected. This was a less aggressive increase than the 75 basis point hikes seen in the last four meetings. Given the historically rapid pace of monetary tightening so far, Federal Reserve Chairman Jerome Powell indicated it may be appropriate to hike by only 25 basis points at the next policy meeting at the end of January. Fed officials are now estimating that interest rates will peak at the range of 5% to 5.5% next year.

Meanwhile, the central banks of the Eurozone, UK, and Switzerland all matched the Fed in hiking by 50 basis points as well. The Bank of England expressed caution about future interest rate increases, as the UK is facing more severe economic headwinds than either the US or continental Europe. In fact, recent data out of the Eurozone suggest that it may be weathering its energy shock better than had been previously feared. However, that relative improvement may only give the European Central Bank (ECB) more leeway to hike interest rates further. ECB President Christine Lagarde indicated continued rate hikes at the pace of 50 basis points were likely, citing the fact that the EU began tightening monetary policy later than the US. The ECB’s policy rate now stands at a range of 1.5% to 2%, with investors currently estimating that rates will peak at 3.8%. However, the outlook for Europe is highly variable and contingent on the dynamics of the energy market.

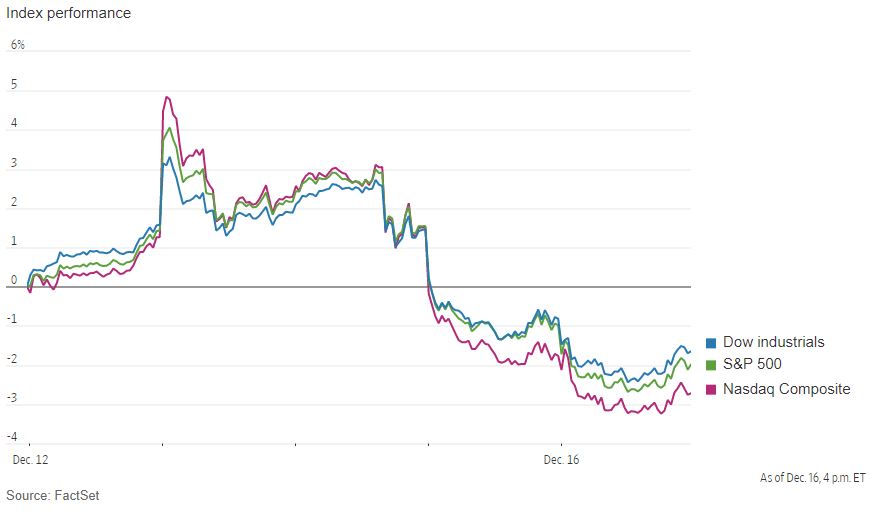

US stocks rallied to start the week as investors reacted with relief to another CPI print that headed in the right direction. However, that brief surge of bullishness was ultimately overcome by concerns regarding the economic impact of higher interest rates. The delayed effects of higher borrowing costs began to show up in the US economic data on Wednesday, when it was shown that retail sales for November fell by 0.6% from the prior month. Though consumers spent less on typical holiday goods, spending on staples and services grew. It is important to note that retail sales figures are not adjusted for inflation. The November decline could in part reflect lower prices for goods as retailers look to offload their glut of inventory. However, manufacturing output also fell by 0.6% last month in its weakest monthly showing since June. These sobering data points were sufficient to send stocks lower over the last three days of the week. The Nasdaq Composite, S&P 500, and Dow Jones Industrial Average all ended with week with losses greater than 1.5%. Oil prices also fell over concerns of weakening demand, with Brent crude ending the week at $79.04 per barrel. The yield on the 10-Year US Treasury note ended the week at 3.48%.