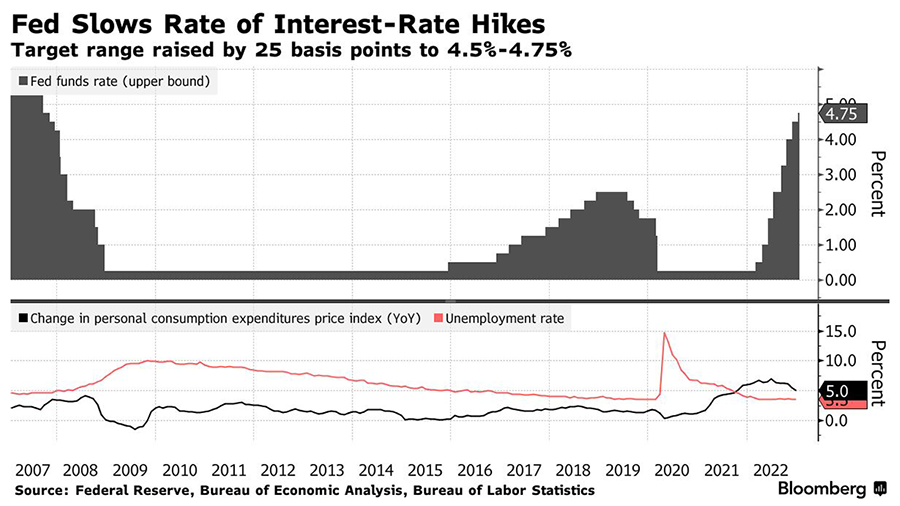

The Federal Open Market Committee (FOMC) unanimously voted at its February 1st meeting to raise the benchmark US Federal-funds target rate by a smaller increment of 25 bps, a widely expected move following a 50 bps increase at the FOMC’s December meeting. That puts the current benchmark interest rate at a range of 4.5%-4.75%. Most Fed officials expected a terminal interest rate of 5%-5.25% in December, implying that there would be another two quarter-point interest rate increases at the next two meetings before the Fed would pause. Core inflation rose 4.4% in December compared to a year ago, as measured by the personal consumption expenditures index, the Fed’s preferred measure of inflation. Though that reading is still above the Fed’s long-term goal of 2% inflation, it is significantly closer than just a few months ago. Meanwhile, the European Central Bank raised its key interest rate last week by 50 bps to 2.5%. The ECB indicated that it intended to raise interest rates again at its March meeting by a further 50 basis points as Eurozone inflation remains at a high 8.5%. The Bank of England also hiked last week by 50 bps to 4%, though the BOE struck a more dovish tone on the path of further interest rate hikes moving forward than the other major central banks.

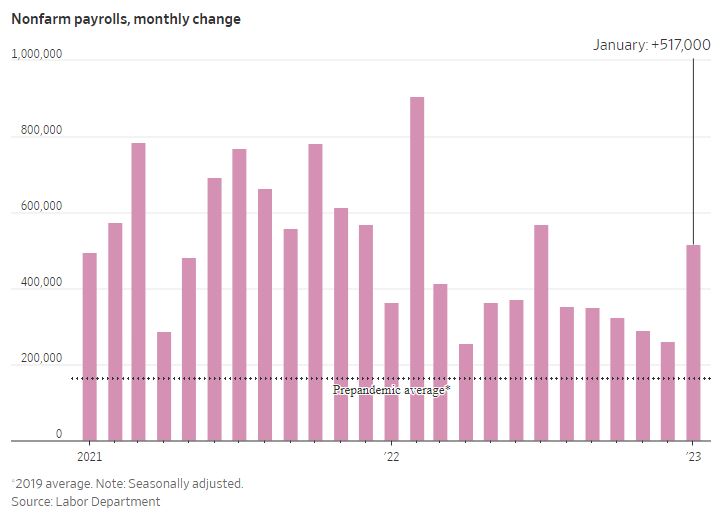

While the prices of goods and energy have declined in recent months, the path of inflation in the US moving forward will be highly contingent on the dynamics of the labor market. The signals for the jobs market have been decidedly mixed, with the Labor Department reporting last week that the employment cost index rose by 1% in the fourth quarter. This was below the consensus forecast for an increase of 1.1% and suggested that labor market pressures on inflation may be easing. However, the January nonfarm payrolls report released on Friday provided a stunning contrast to the slowing trend seen in other figures. The US added 517,000 new jobs in January, far and away above the consensus forecast for 187,000 new jobs. The unemployment rate also dipped even lower to 3.4%, while job openings rose by 600,000 in December to 11 million, or roughly 1.9 open jobs per unemployed worker. Thankfully, wage growth continued to ease last month despite the strong hiring activity. Average hourly earnings rose 4.4% in January compared to a year ago, slowing from December’s rate of 4.8%. While recent data on consumer spending had suggested a weakening trend, an updated gauge of services spending also surprised to the upside on Friday. The ISM non-manufacturing index snapped back into strong expansion in January after a weak reading in December. The robust spending on services challenges the narrative that consumer spending is running out of gas and suggests instead that spending is shifting from goods to services. These surprisingly strong economic readings challenge the narrative that inflation is likely to ease further and complicate the Fed’s task of achieving a soft landing for the economy.

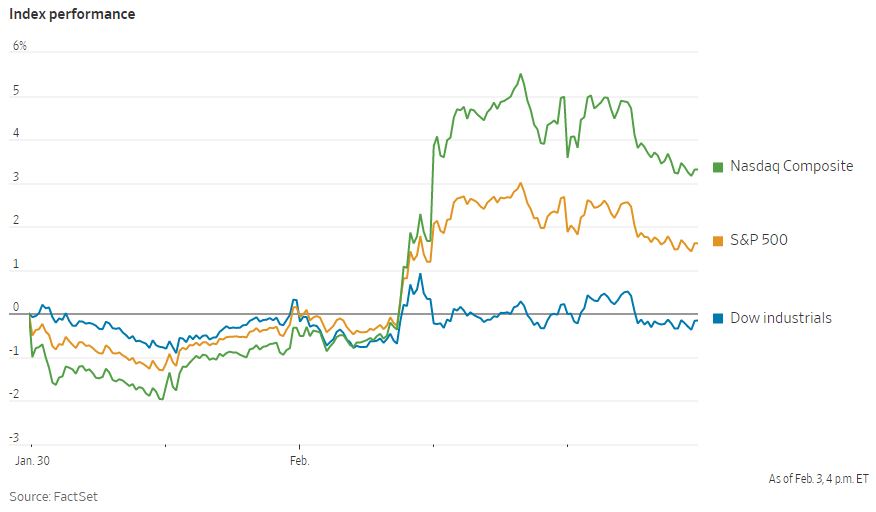

The market was quiet for the first half of the week as investors waited for the conclusions of the FOMC. Equities rallied following the Fed decision for a smaller rate hike, with the longer duration growth stocks in the Nasdaq Composite and S&P 500 responding more positively. Markets drifted lower on Friday following the blockbuster jobs report due to concerns that the Fed may have to raise interest rates further to bring inflation under control. Despite the losses on Friday, the S&P 500 and Nasdaq ended the week with gains, while the Dow Jones Industrial Average ended roughly flat. The communication services and technology sectors had the strongest showing and ended the week with gains near 4%. The energy sector was easily the laggard last week with a loss of around 4.5%. Energy equities have rallied strongly to start the year, with the S&P 500 up roughly 9% to date while the beaten-down Nasdaq had gained roughly 17%. The yield on the US 10-year Treasury note fell to as low as 3.358% following the FOMC meeting but surged again in the wake of the jobs report back up to 3.512%.