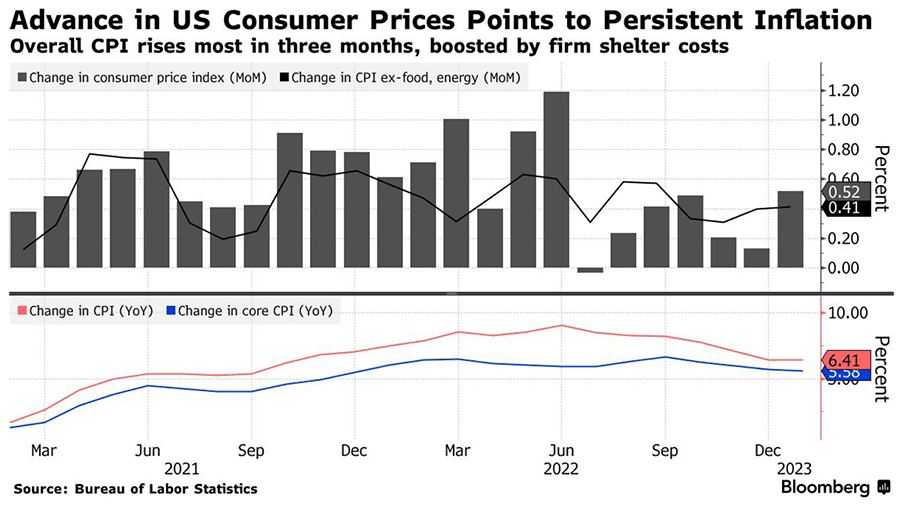

The US consumer price index increased by 6.4% in January from a year earlier, marking the seventh straight month of cooling in annual inflation since peaking at 9.1% in June. However, from a month earlier inflation firmed, with the CPI increasing by 0.5% in January compared to 0.1% the previous month. The cost of shelter was the largest contributor to the monthly gain and prices for food, gasoline and natural gas also rose in January. Core CPI, which excludes volatile energy and food prices, rose by 5.6% from a year earlier, down from 5.7% in December. Many economists see the core measure as a better predictor of future inflation. Compared to the month prior, core inflation rose by 0.4% in January, staying steady at the same rate recorded in December. The latest readings come as the Federal Reserve raised interest rates aggressively in the past year. Earlier this month, the central bank raised its benchmark rate to the highest level since 2007, though the increase was by the smaller amount of 25 basis points. The Fed is trying to combat inflation by slowing the economy, and officials indicated in February they anticipate lifting rates further in 2023. The January data includes annual updates to historical seasonal factors as well as a shift in the weights of goods and services in the calculation basket, which affect the one-month price change. Using the new seasonal adjustments, both overall and core inflation cooled less toward the end of 2022 than previously thought.

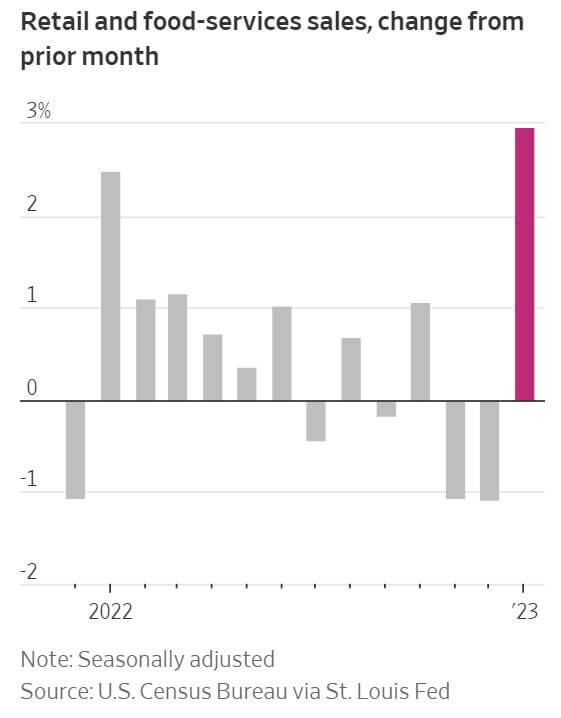

Retail sales increased by 3% in January according to the US Commerce Department, marking the biggest gain since March 2021. The surge in spending was largely driven by a boost in the purchase of vehicles, furniture, clothing, and dining out, after two months of declines in spending toward the end of last year. Strong wage gains and a solid January employment report indicate that the economy is rebounding after the uncertainty caused by rising prices, increased borrowing costs and pandemic-related restrictions led households to pull back on spending. Despite high inflation rates, which climbed to 6.4% in January from the previous year, consumers are still spending and economists believe that this could indicate that economic growth is picking up. Meanwhile, US factory production rose by 1% in January, the largest increase since February 2022 following a 1.8% decline in December. The data released by the Federal Reserve on Wednesday suggested that improving supply chains and demand were providing some relief for a challenged manufacturing sector. The rebound provided a welcome respite after two months of declining production. The increase was also higher than the 0.8% forecast in a Bloomberg survey of economists. The Fed’s report also indicated that capacity utilization at factories rose to 77.7%, following the lowest level in over a year in December. Although the latest figures provide a welcome boost, manufacturers still face headwinds, including elevated inventory levels, a tepid global economy and risks of a pullback in capital investment as interest rates rise. The Institute for Supply Management survey showed a gauge of factory activity had contracted for a fifth month, reaching the lowest level since May 2020, indicating that manufacturing was still struggling.

Investors had bet that the slowdown in inflation would lead the Fed to begin cutting interest rates later in the year, despite the central bank's insistence that it was too early to think about shifting policy. However, the latest jobs report and Tuesday's high inflation data shook traders last week, causing longer-dated wagers to adjust more in line with the central bank's latest forecasts. Wall Street's base case at the start of February was for the Fed to raise rates to between 4.75% and 5% around midyear before cutting them by 0.50 percentage point in the latter half of 2023. Following the latest consumer-price print, derivatives markets showed the federal funds rate peaking at 5.28% in August, with the benchmark rate forecast to end the year above 5.12%. Short-term bond yields jumped on Tuesday and the two-year Treasury yield rose to 4.62%, its highest level since November. Though equities at first resisted the pull of higher bond yields, hawkish comments from Fed officials later in the week took their toll. Two Federal Reserve officials said that they support a larger rate increase than the quarter-percentage-point increase that was implemented at the central bank's February meeting. On Friday, the yield on 10-year Treasuries rose to 3.895% from 3.842% on Thursday. The S&P 500 and Dow Jones Industrial Average ended the week with small losses, while the Nasdaq Composite hung on to a weekly gain of 0.6%. Rising expectations of higher interest rates have led to a boost in the dollar, with the ICE U.S. Dollar Index on track for a third straight weekly advance.