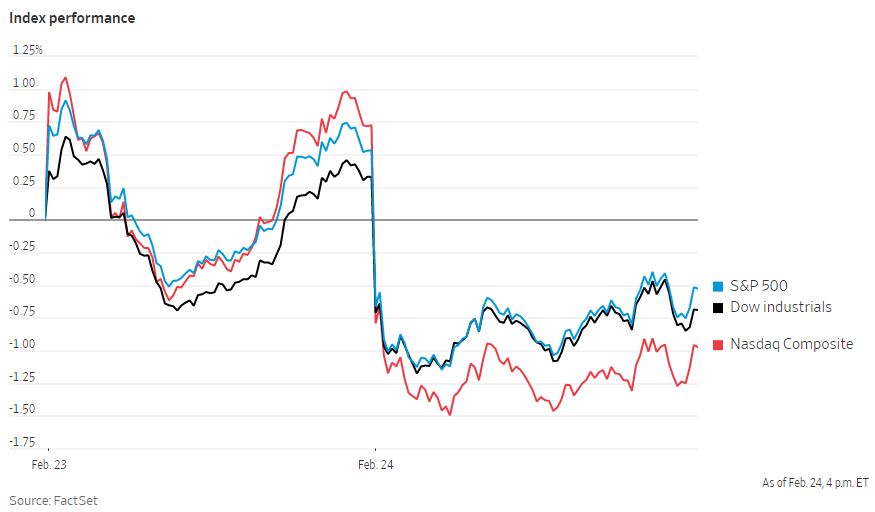

The US stock market closed out its worst week of 2023 as concerns about the Federal Reserve’s policy, inflation and a resilient economy weighed heavily on investor sentiment. The S&P 500 fell 1.1%, or 42.28 points, to 3970.04 while the Nasdaq Composite dropped 1.7%, or 195.46 points, to 11394.94, and the Dow Jones Industrial Average shed 1%, or 336.99 points, at 32816.92. All three indexes fell more than 2% for the week, marking their biggest weekly declines in 2023. Markets began 2023 on a high note, with investors betting that the moderation of inflation would prompt the Fed to cut interest rates later this year. However, investor enthusiasm has waned following reports of stickier-than-expected inflation and a resilient economy, indicating that the Fed may maintain aggressive monetary tightening measures to cool price pressures. The PCE price index for January, which overshot economists’ expectations, added to these worries on Friday. The strong inflation data also caused short-term Treasury yields to surge to levels not seen in more than a decade, with the two-year Treasury note yield reaching 4.803%, the highest since 2007. Despite the market’s recent turbulence, some investors are optimistic that the Fed could control inflation without inflicting too much economic pain, given the economy’s resilience in the face of higher interest rates.

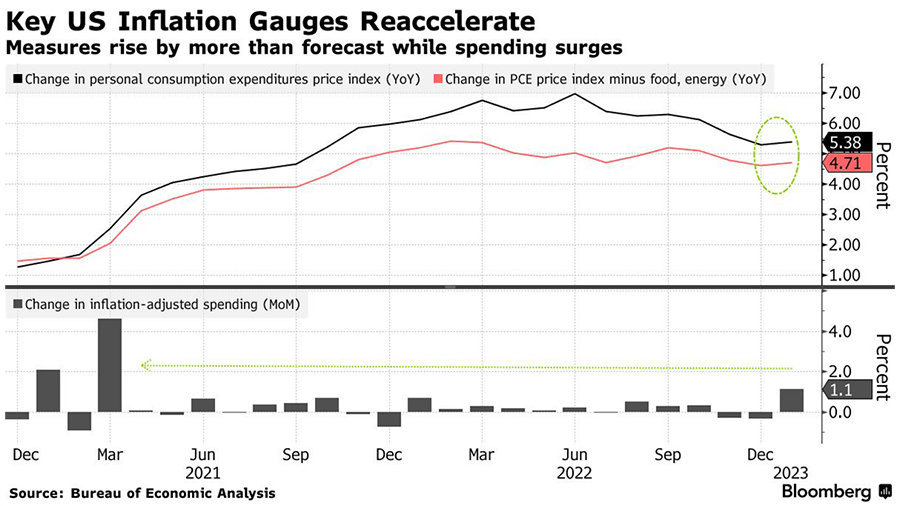

In January, the US Federal Reserve’s preferred inflation gauge, the personal consumption expenditures (PCE) price index, accelerated unexpectedly after several months of decline. The PCE price index rose 5.4% from a year earlier, while the core metric increased by 4.7%, both exceeding projections. Both headline and core PCE accelerated to a substantial 0.6% increase from the prior month. Meanwhile, consumer spending surged after a year-end slump, with spending adjusted for prices jumping 1.1% from the previous month after consecutive monthly declines, the most in nearly two years. The increase in personal spending in January reflects a pickup in outlays for goods and services, including motor vehicles, food services and accommodation. With the unemployment rate at its lowest level in over 53 years and intense competition for a limited supply of workers, higher wages paired with excess savings have allowed consumers to keep spending for a variety of goods and services despite the rapid price increases. Incomes also rose 0.6% in January, bolstered by an acceleration in wage growth. Inflation-adjusted disposable income surged 1.4%, the biggest advance since March 2021, while wages and salaries, unadjusted for prices, increased 0.9%, the most since July. Resilient consumer spending, paired with the exceptional strength of the labor market, will also make it more difficult for the Fed to achieve its inflation goal.

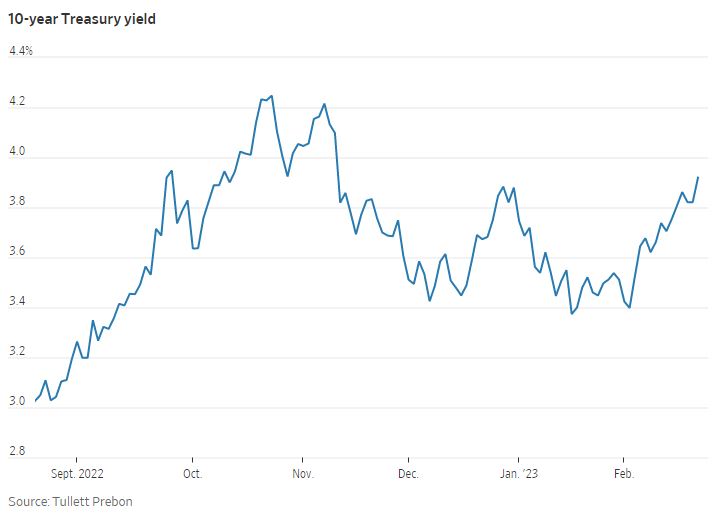

Treasury yields have reversed their early-year rally and are higher than where they finished 2022, thereby ending a brief reprieve for stocks and riskier types of bonds. The yield on the benchmark 10-year Treasury note has raced back toward 4% over the past month. The benchmark 10-year Treasury yield rose to 3.948% on Friday from 3.879% on Thursday, and Federal-funds futures reflected bets that the central bank would bring interest rates significantly higher than most investors expected a month ago. The current yield on the 10-year US Treasury note is well above its 3.374% January low and higher than the 3.826% yield where it ended 2022. This has occurred due to traders’ fast-changing expectations for how the Federal Reserve might respond to new data suggesting the economy is still growing. Derivatives markets show that traders now expect the terminal rate this summer to be above 5.25%. A month ago, they were betting on a peak rate of about 4.9%. The Fed’s rate target currently stands at 4.5% to 4.75%.

As they were for much of last year, investors are once again hanging on any indication of how the Fed will respond to a stronger-than-expected economy. Rising Treasury yields erode investors’ willingness to pay up for stocks and corporate bonds because buying Treasurys lets investors lock in attractive returns with lower risk. After raising interest rates by three-quarters of a percentage point at four straight meetings last year, the central bank downshifted to a half-percentage-point increase in December and followed that with a quarter-point rise in February. Coming into this year, many investors assumed that declining inflation and a slowing economy would give the Fed the go-ahead to ease off, but strong data have now shaken that assumption.