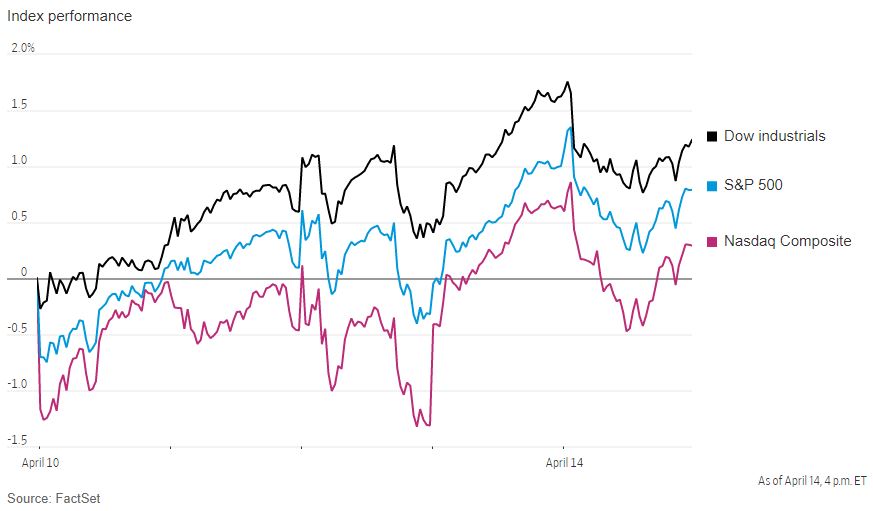

Big banks posted stronger-than-expected earnings last week, which provided a bright spot for stock markets, but executives warned that stress in the sector is still darkening their outlook for the US economy. The Dow Jones Industrial Average dropped 0.7% on Friday, while the Nasdaq Composite Index fell 0.8% and the S&P 500 was down 0.6%. Every sector of the S&P 500, except for finance, traded lower, with real-estate stocks declining 1.9%. Despite this, strong earnings from big banks have indicated that size increasingly matters in a US financial system responding to interest-rate hikes that many investors expect to continue. Citigroup shares rose 4.9% on Friday, while JPMorgan jumped 7.3% following its report of record quarterly revenue and a 52% jump in quarterly profit. However, Jamie Dimon, JPMorgan's CEO, warned that fallout from the collapse of Silicon Valley Bank and Signature Bank last month could weigh on lending, potentially cutting off capital that businesses need for investments, deals and hiring. Other interest-rate increases at the Fed’s next meeting could further tighten credit markets, as well as bring more risk to certain lenders’ balance sheets. The big banks’ earnings appeared to soothe investors’ concerns that the stress at regional banks could metastasize into a full-on financial crisis. Bank of America gained 3.5%, Morgan Stanley rallied 1.4% and Goldman Sachs rose 1.2%. Wells Fargo slipped 0.5% in afternoon trading after the company said it set aside more money for bad loans. Benchmark U.S. crude futures, which have stagnated alongside darkening economic forecasts, rose 2.3% last week to $82.52 a barrel. The 10-year U.S. Treasury yield edged up to 3.517% Friday from 3.450% Thursday.

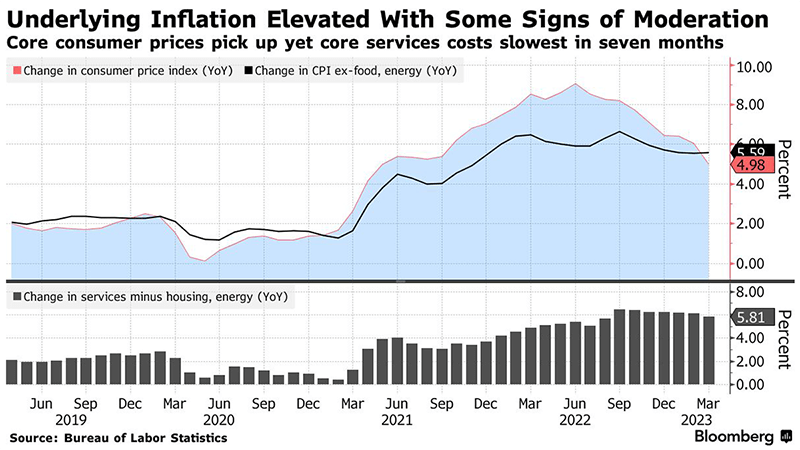

US inflation eased to its lowest level in nearly two years in March. The Consumer Price Index (CPI), which measures what consumers pay for goods and services, rose 5% year-on-year, down from February's 6% increase and the smallest gain since May 2021. However, core prices, a measure of underlying inflation that excludes volatile energy and food categories, increased 5.6% YoY, accelerating slightly from 5.5% the prior month. This was the first time in over two years that the core came in above the overall measure. Core inflation, which economists see as a better predictor of future inflation, has stayed stubbornly high due to inflationary pressures from shelter costs. Because of the way housing metrics are calculated, there is a significant lag between real-time price changes and government statistics. Economists are expecting shelter inflation to trend significantly lower later this year. The US Federal Reserve raised interest rates by a quarter percentage point in March, bringing it to a range between 4.75% and 5%, and indicated that another increase could happen at its early May meeting. With core inflation easing only slightly in month-on-month terms to 0.4% in March compared to the 0.5% increase seen in February, the Fed is still likely to raise interest rates again at its May meeting. Swaps pricing currently implies an 80% chance of a quarter-point rate increase in May. Most expect the Fed to pause rate hikes after the May meeting, provided the economy grows slower this year and labor demand cools.

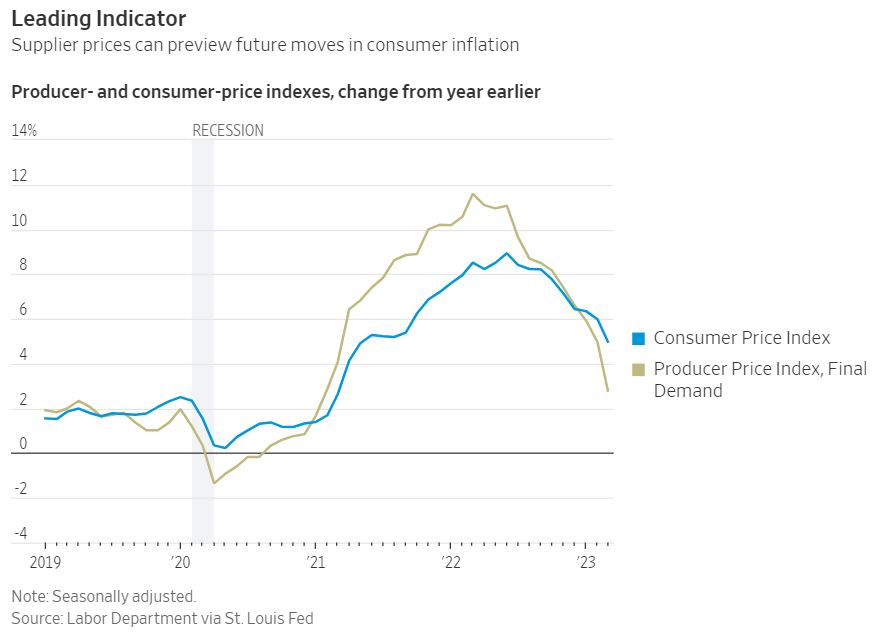

U.S. supplier prices fell by 0.5% in March compared to the prior month, the largest monthly decrease since April 2020, indicating a moderation in inflation. From a year earlier, supplier prices rose by 2.7% in March, a significant slowdown from highs reached last year. Cooling supplier prices can signal a future fading of consumer inflation (CPI). The decline in goods prices was the main factor in the cooling of supplier prices in March. Meanwhile, initial jobless claims increased by 11,000 to a seasonally adjusted 239,000 last week, but the labor market remains solid despite stresses in the banking sector. American retail spending decreased for the second consecutive month in March, with consumers cutting back on purchases of items including vehicles, furniture and appliances due to rising interest rates. The Commerce Department has stated that overall purchases at stores, restaurants and online declined a seasonally adjusted 1% in March from the prior month. The decline in retail sales could suggest that higher interest rates are working to slow down the economy, which Federal Reserve officials have intended. Manufacturing output, which is also sensitive to interest rates, declined 0.5% in March from the prior month and is down from a year earlier, the Fed said in a separate report Friday.