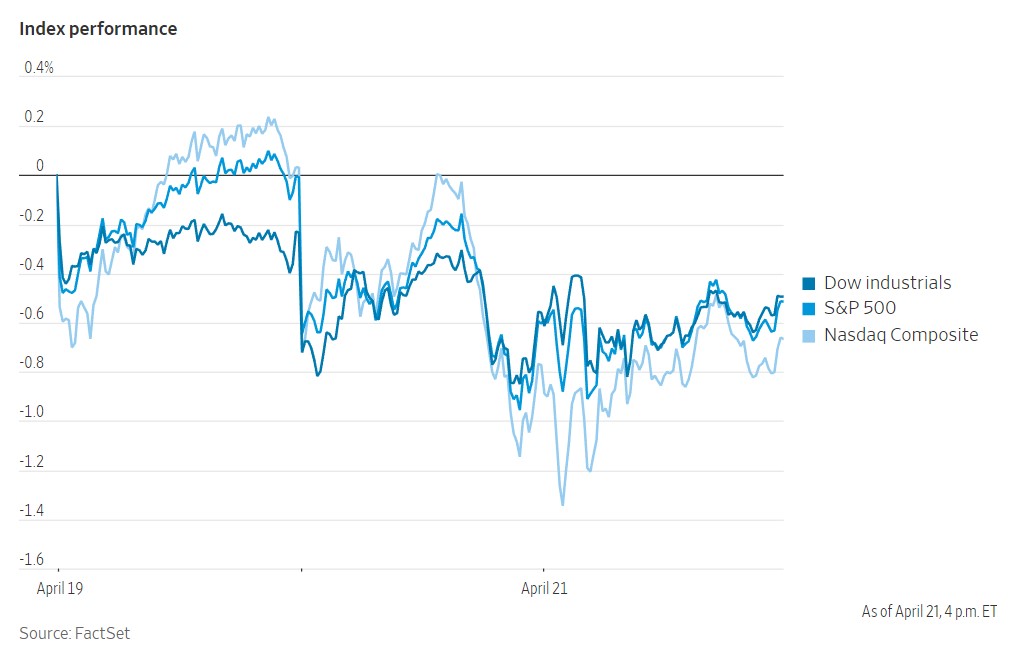

U.S. equity markets moved sideways for most of last week as investors digested the latest quarterly earnings results. The Dow Jones Industrial Average, S&P 500 and Nasdaq Composite ended the week down -0.5%, -0.5% and -0.7%, respectively. Treasuries were weaker across the curve, with yields ending up for the week. Gold ended down 1.4%, back below $2,000/oz. Bitcoin futures were down 3.6% and WTI crude settled up 0.6% but still posted a 5.8% decline last week. The market is dealing with a lot of moving pieces and conflicting signals. The Fed is the biggest area of debate with hawkish Fedspeak reiterating the higher-for-longer mantra while the market is expecting a quick pivot in the second half of the year. Soft landing is supported by a strong labor market, consumer resilience and housing rebound. However, hard landing is underpinned by the magnitude and velocity of the tightening cycle. Tight corporate bond spreads are a signal for the soft landing camp. Deep curve inversion, collapsing money supply growth, contractionary ISM manufacturing readings, and leading indicators are the key signals for the hard landing camp. Earnings are another area of debate as growth is expected to resume in Q3, while the more bearish strategists see 10-20% downside risk to consensus estimates.

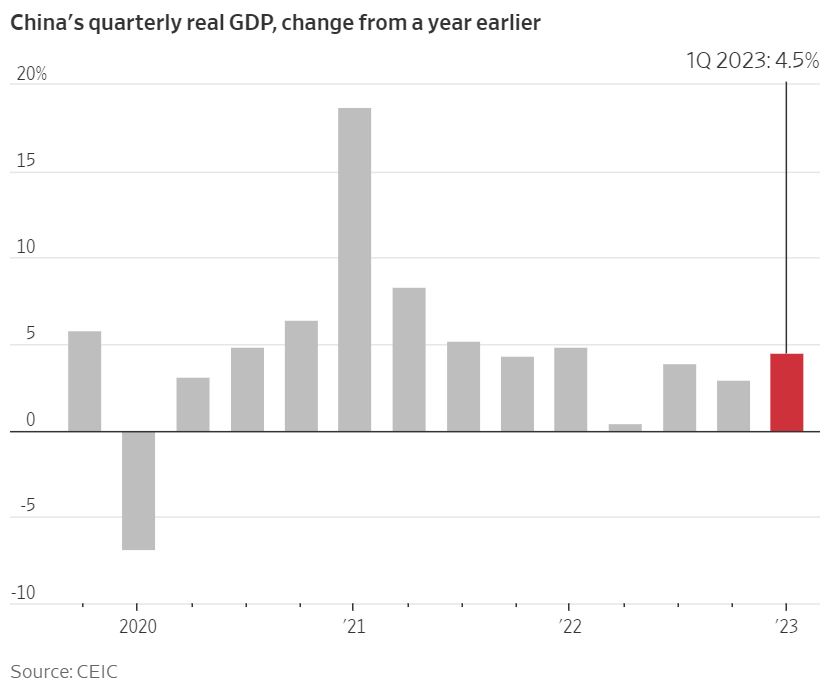

China’s economy grew by 4.5% in Q1 2023 compared to the same period a year earlier, according to Beijing’s National Bureau of Statistics. That beat economist estimates and marked the fastest rate of growth since Q1 2022 and was an improvement on Q4 2022’s 2.9% rate. Retail sales, which jumped more than 10% in March from a year earlier, played a significant role in the country’s economic recovery, offsetting a sharper-than-expected slowdown in real estate, infrastructure and other private-sector investments. This marked the first month in two years that the year-over-year gain in retail sales outpaced the increase in both industrial production and fixed-asset investment. The rebound in consumer spending is largely organic and not reliant on stimulus, leading economists to believe that economic momentum will improve in the second quarter and for gross domestic product growth to surpass 6% this year—comfortably above the official government target of around 5%. In another sign of recovering economic activity, oil demand is rebounding, with China's apparent petroleum demand rising nearly 10% year over year in March. However, investment in the property sector, which has played a significant role in driving China’s economic growth over the past decade, has yet to stabilize, with property investment dropping 5.8% in Q1 compared with a year earlier. The big question for the economy this year is whether the jump in consumer spending is merely ephemeral, known as “revenge spending,” or whether it heralds a more lasting shift toward consumers playing a greater role in driving overall growth. Although China still has a significant economic hole to climb out of, the latest figures show that it is back in business and remains a formidable global economic force. On Tuesday, both UBS and Citigroup raised their GDP forecasts for China this year to 5.7% and 6.1%, respectively, well above the official growth target of around 5%.

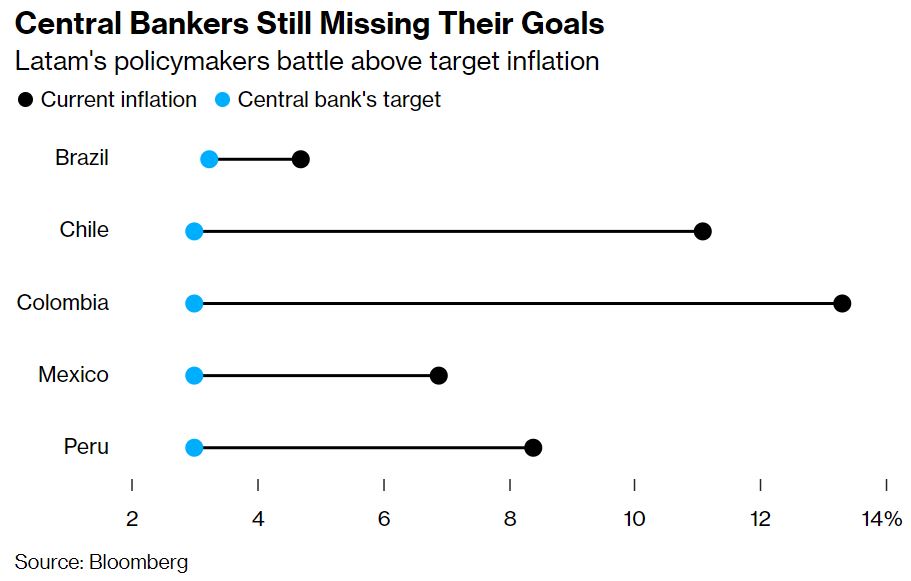

Though Latin America stands to benefit from renewed demand from China for commodity exports, the region is still saddled with high interest rates enacted to combat inflation. Latin American policymakers are warning investors that their battle against inflation will take longer than expected, despite aggressive interest rate hikes. During the International Monetary Fund’s Spring Meetings, officials from Brazil, Chile and Peru expressed the need for more proof that price pressures are easing before cutting borrowing costs. The region’s top economic authorities are asking for patience from the market as they hold rates higher. The message is a sharp turnaround from the previous round of IMF meetings in October, when disinflation was expected. Core measures of inflation that strip out volatile items like food and energy are still accelerating in the region, making it harder to cut rates without the risk of having to reverse course and lift them again. Latin America’s inflationary pressures are getting an additional jolt from a backdrop of steadily higher borrowing costs in the world’s main economies. Despite some heads of state criticizing policymakers’ positions, regional central bankers are doubling down on their fight against inflation. Growth forecasts for the region have been revised down as credit flows slow down and households struggle with indebtedness. Many countries are also facing drastic weather events that hinder activity, pushing authorities to find alternative sources of financing. The region has some structural issues to deal with, including infrastructure, education and health, and it can’t make a big dent in poverty at economic growth rates of around 2%, as most multilateral organizations expect.