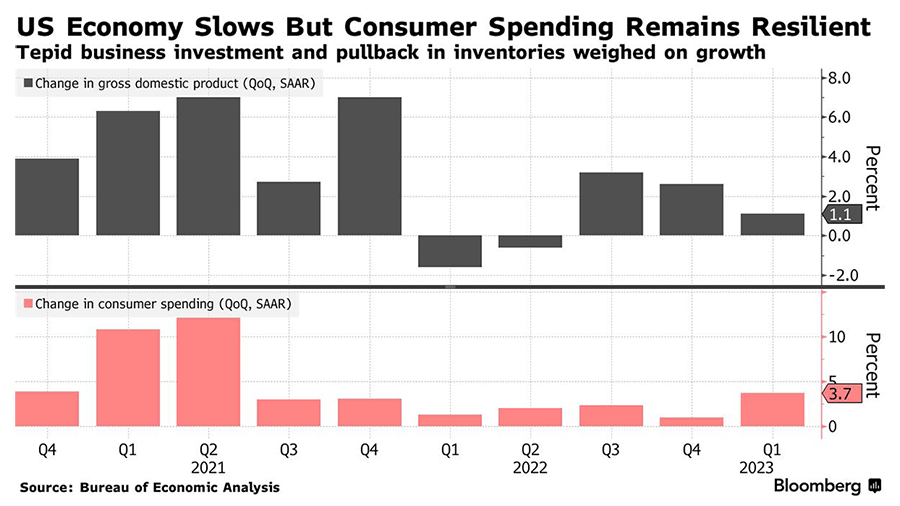

US economic growth slowed to an annualized rate of 1.1% in the first quarter in a sharp slowdown from the 2.6% annualized growth rate seen in the fourth quarter. This was due to a decline in business investment and a pullback in inventories, according to the Commerce Department’s initial estimate. However, the strongest consumer spending in almost two years helped support the GDP figure for the quarter, though more recent data suggests consumer spending may be slowing as well. Retail sales, homes sales and manufacturing output all decreased in March. The resiliency of the job market will determine the outlook, with low unemployment and wage gains allowing consumers to weather high inflation and maintain spending. The GDP data showed services spending rose 2.3%, led by healthcare and restaurants and hotels, while outlays on goods rose 6.5%, the most in almost two years. The economic slowdown is expected to be more evident in the second quarter, with economists predicting GDP to grow at a stall-speed pace of 0.2%.

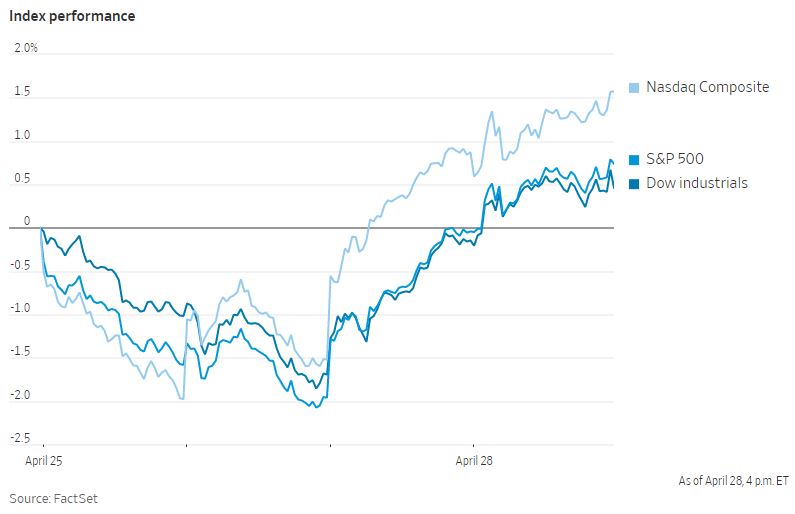

The stock market rebounded last Thursday after a downturn earlier in the week, propelled by a round of strong corporate earnings reports, with big tech earnings helping to mitigate mixed economic signals. According to FactSet data, 235 companies within the S&P 500 have reported results so far this earnings season, with first-quarter earnings expected to drop by 4.2%, which is less than Wall Street analysts had feared. However, Liz Young, head of investment strategy at SoFi, warned that positive surprises may not last as the year progresses, with profit margins falling despite companies still reporting revenue growth. US equities continued to rally on Friday, driven by better-than-expected earnings from Exxon Mobil and Intel. The S&P 500 was up by 0.6% on Friday, while the Nasdaq 100 rose 0.4%, although Amazon.com weighed on the latter index with a 3.4% loss following a warning over growth in its key cloud computing business. First Republic Bank fell 39% following reports that FDIC receivership is the most likely scenario for the bank after a run on deposits. The uncertainty of bank rules following the collapse of Silicon Valley Bank, as well as the prospect of further Federal Reserve rate hikes, have contributed to investor caution. The yield of the US 10-Year Treasury note fell to end the week at 3.478%. European markets have also been affected by a rise in consumer price gains, which points to more rate increases by the European Central Bank, but the Stoxx 600 still gained 0.6%.

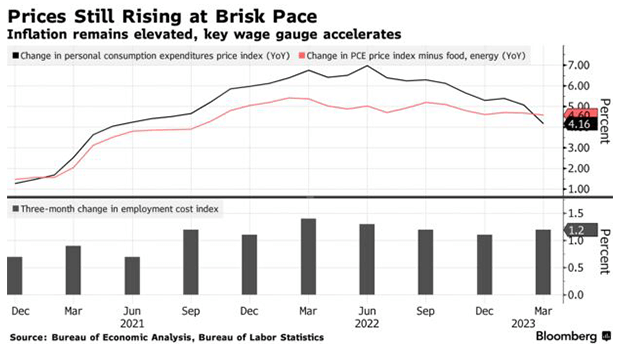

The latest US economic data indicates that inflation pressures remain persistent. The personal consumption expenditures price index (PCE), the Federal Reserve's preferred measure of underlying inflation, rose 4.2% in March compared to a year ago, slowing from February’s gain of 5.1%. However, the core-PCE index, which excludes volatile food and energy prices, rose 4.6% in March from a year earlier, barely slowing from February’s 4.7% increase. The Labor Department's employment costs measure also rose 1.2% in Q1 from the previous quarter, exceeding forecasts. However, a deceleration in a closely watched measure of services costs offers some relief. The report suggests that rising labor costs, particularly in the service sector, could keep price growth above the Fed's target for the foreseeable future. The data reinforce expectations that Fed policymakers will raise the benchmark interest rate another quarter percentage point at this week's meeting. While consumers are still enjoying a strong labor market and excess savings, the latest figures suggest they are beginning to cut back on discretionary purchases. A lack of growth in spending could make it difficult for the economy to keep expanding. Finally, a separate report showed that longer-term inflation expectations ticked up in April.