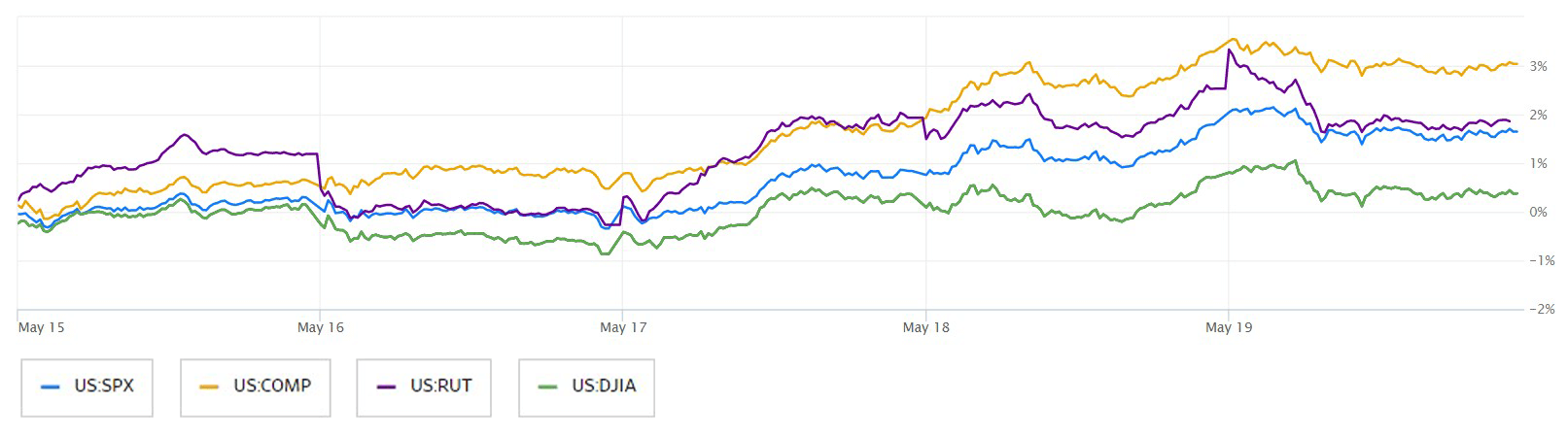

Equity markets finished last week in positive territory despite debt ceiling talks breaking down in Washington on Friday. The S&P 500, Nasdaq Composite, Russell 2000, and Dow Jones Industrial Average finished the week up 1.65%, 3.04%, 1.89%, and 0.38%, respectively. The S&P 500 notched its second-best week since March and briefly broke above the 4200 level for the first time since August. Early signs in the week that lawmakers were making progress on the debt ceiling helped fuel the risk-on sentiment. In a common trend for 2023, the Mega-Cap growth stocks continue to drive much of the returns as the Mega Cap Growth ETF (MGK) was up 3.2%, with similarly strong returns from the Philadelphia Semiconductor Index up 8.4% and the SPDR S&P Regional Banking ETF (KRE) up 9.8% last week.

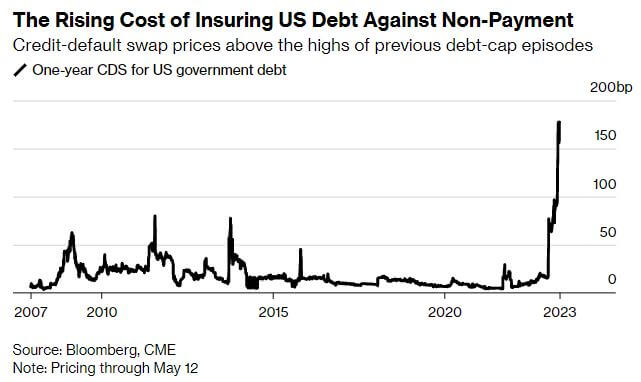

Concerns about the risk of a US government default are growing as bills maturing in early June show signs of worry and investors believe the risks of a default are greater this time than in the 2011 debt-limit crisis. Treasury Secretary Janet Yellen informed lawmakers that the department's ability to avoid breaching the statutory debt ceiling through accounting maneuvers could be exhausted around that time. The Treasury has been providing updates on its remaining reserves from extraordinary measures, which stood at approximately $88 billion as of last Wednesday. The diminishing window for a resolution is evident, with ongoing talks between President Joe Biden and House Speaker Kevin McCarthy yielding little progress. The potential default has led to increased yield premiums for T-bills maturing after the X-date, indicating concerns about non-payment. The cost of insuring US debt against default via credit-default swaps is now higher than countries like Greece, Mexico, and Brazil. Financial markets remain hopeful that a deal will be reached, as a default on US Treasuries is still considered unlikely, with the government planning on prioritizing bond payments over other expenses.

According to a survey by Bloomberg, gold is the top choice for protection if the US government defaults, with over half of financial professionals indicating they would buy gold in such a scenario. However, gold has already rallied this year from both luxury demand and investors seeking havens following banking sector concerns and currently stands just below its all-time high of $2,075.47 per ounce. US Treasuries, despite the irony of being the potential defaulting instrument, were the second most popular asset to buy in the event of a default. Other alternatives considered were traditional haven currencies like the Japanese yen, Swiss franc, US dollar and even Bitcoin.

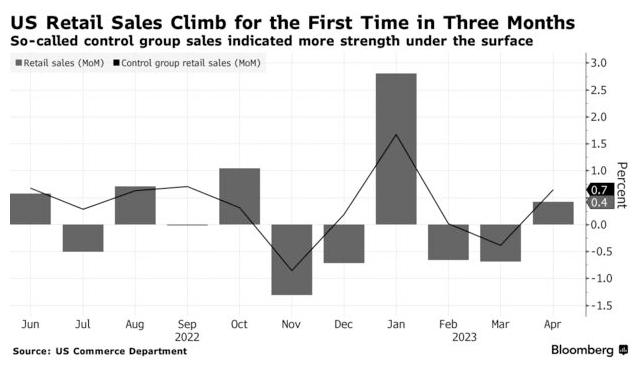

US retail sales in April showed an increase of 0.4%, suggesting that consumer spending remains resilient despite economic challenges such as inflation and high borrowing costs. When excluding auto and gasoline sales, the increase was 0.6%. Although the overall figure fell short of economists' expectations, sales excluding autos and gasoline exceeded forecasts. Low unemployment and steady wage growth were cited as factors supporting consumer demand. However, there are signs of a shift in consumer preferences toward services, and some sectors, such as furniture retailers and sporting goods stores, saw declines in sales. Credit card balances and financing rates continue to rise, which may pose challenges to further consumer spending. It should be noted that the retail sales data do not account for price changes and only include one service-sector category, making it challenging to draw definitive conclusions about the spending environment.

US factory production also rebounded in April, primarily driven by the automotive sector, indicating some stabilization in the demand for goods. Manufacturing output increased by 1% last month, with notable growth in motor vehicle production, primary metals, computers and electronic products, and chemicals. Stable supply chains and cheaper commodities have provided some relief to factories, however, the manufacturing sector is facing various challenges including tightening financial conditions, weaker goods demand and an uncertain outlook. Despite the rebound in factory output, survey data indicates that the sector is struggling to gain momentum, with the Institute for Supply Management's factory gauge indicating contraction for six consecutive months. Business equipment orders have also declined in recent months. The capacity utilization rate at factories rose to 78.3%, indicating increased potential output, while utility output dropped due to milder temperatures and mining increased primarily in oil and gas extraction.