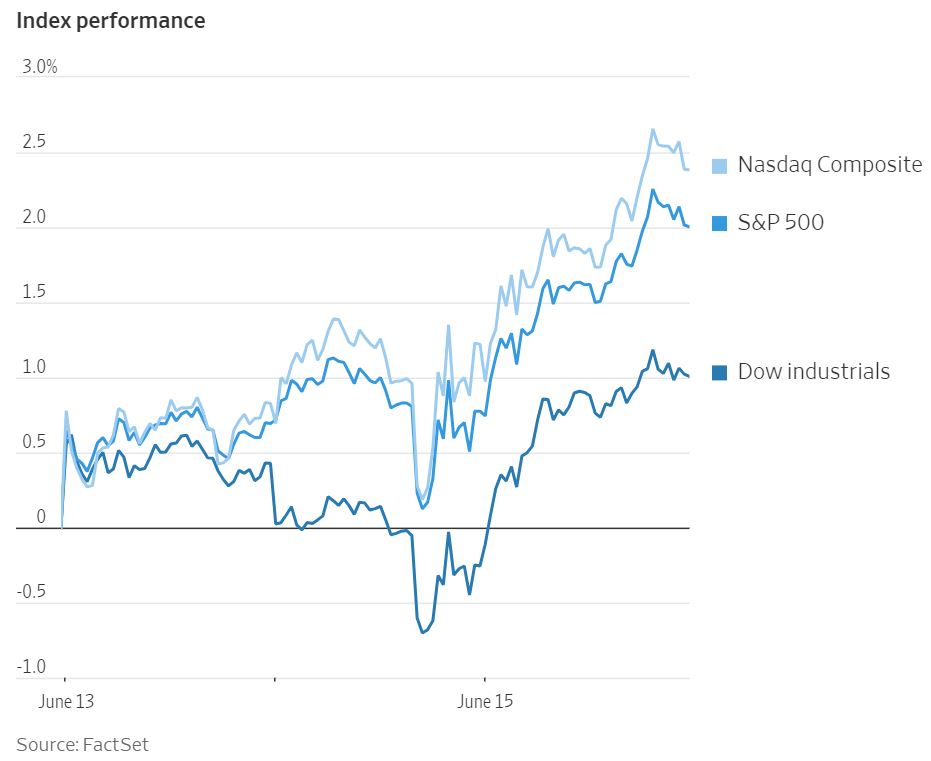

The momentum of the artificial intelligence (AI) sector in the stock market paused on Friday as Wall Street faced a significant options expiration test. The tech-heavy Nasdaq 100 underperformed, with losses in major companies like Microsoft and Apple, which had recently reached all-time highs. Chipmakers were affected by a warning from Micron Technology while Adobe climbed due to a bullish forecast. Although the S&P 500 ended its six-day winning streak, it still had its best week since March. Traders were caught between the fear of missing out on the market rally and concerns about an overbought market, further complicated by options contracts worth an estimated $4.2 trillion tied to stocks and indexes that were maturing. The impact of derivatives on trading was so significant that, at one point, the popular VIX volatility index was rising alongside the S&P 500. However, the VIX eventually gave in and erased its gains for the week. Market movements seemed disconnected from certain developments that could typically impact trading, such as consumer inflation expectations and geopolitical news, including Russia's delivery of tactical nuclear weapons to Belarus. Hawkish statements from the Federal Reserve also had little to no impact on Friday's trading. While the S&P 500 recently entered a technical bull market, some analysts including Michael Hartnett of Bank of America, remain skeptical that it marks the start of a sustained upward trend.

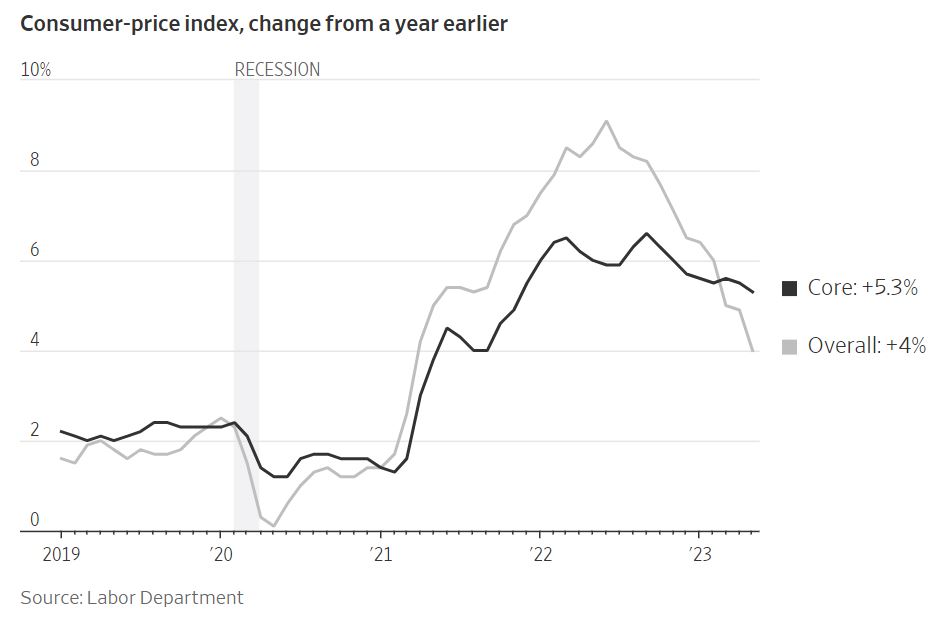

Inflation in May dropped to approximately half of last year's peak but remained high, indicating progress in reducing price pressures but suggesting that more work needs to be done by Federal Reserve officials. The consumer-price index rose by 4% compared to the previous year, significantly lower than the peak of 9.1% in June 2022 and slightly lower than April's increase of 4.9%. Core consumer prices, which exclude the volatile food and energy categories, rose by 5.3% in May compared to the previous year. The increase in core prices is partly due to the previous surge in housing-rental prices, which takes time to reflect in inflation data. Overall consumer prices increased by 0.1% in May compared to the previous month, driven by rising housing, used-vehicle, and food prices. The Federal Reserve has been monitoring labor-intensive services prices as an indicator of wage pressures affecting consumer prices. Despite inflation cooling down, higher prices for goods and services are impacting household spending decisions. However, inflation pressures in the property market may be cooling. Apartment rent growth has significantly slowed down. A fall in rents would follow recent price declines in the housing market. The national median existing-home price fell 1.7% in April from a year earlier, the biggest year-over-year price decline in more than 11 years. Over the 12 months ending in May, new-lease asking rents rose by less than 2%, a significant deceleration compared to the double-digit increases observed a year ago. One of the rent measures, from real-estate brokerage Redfin, already shows asking rents turning negative with a decline of 0.6% in May, compared with the same month last year. This decline in rent prices could help ease inflation as housing costs are a major component of the consumer-price index. The slowdown in the rental market is due to weakening demand and increased competition among landlords, as well as a historic number of new apartments under construction.

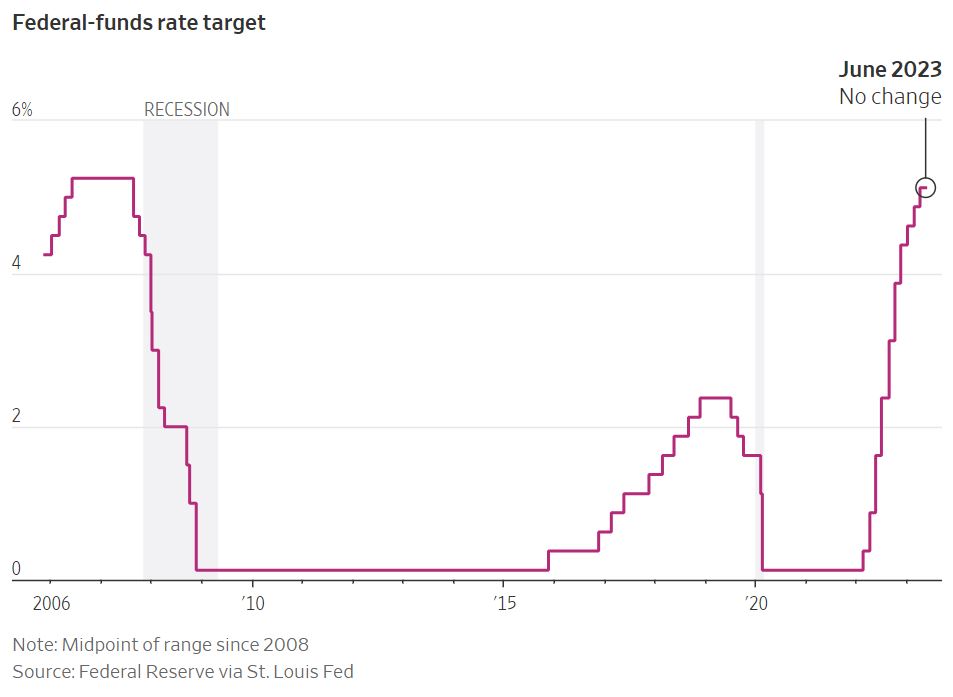

Federal Reserve officials decided last week to keep interest rates unchanged after a series of 10 consecutive increases, but they have indicated that they are inclined to raise rates next month if the economy and inflation do not cool down further. Most officials have projected two more rate increases this year and have revised their expectations for growth and inflation upward. The Fed's decision to maintain the current benchmark federal funds rate range of 5% to 5.25% might be temporary, according to its statement. While some officials are confident about the need to continue raising rates, concerns about recent bank failures and potential credit tightening have made others less certain. Chair Jerome Powell emphasized that the rate decision reflects the progress made in tightening policy, the time lag in the impact of monetary policy on the economy, and the potential challenges from credit tightening. Projections from Fed officials suggest that rates may need to rise to between 5.5% and 5.75% this year, with the majority of committee participants expecting further rate hikes by the end of the year. The Fed is adjusting its tactics to manage the risk of raising rates excessively or too quickly, given concerns about high inflation.