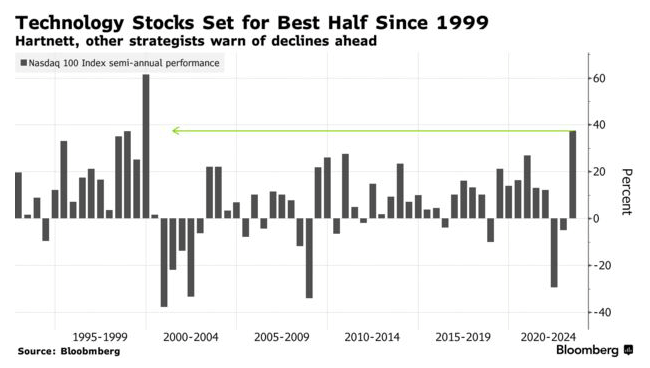

US stocks had their worst week since March due to concerns about central banks raising interest rates to combat inflation. The decline in stock benchmarks like the S&P 500 and Nasdaq 100 was attributed to profit-taking in the technology sector, particularly in AI-related stocks. The S&P 500 ended a five-week streak of gains, while the Nasdaq ended an eight-week run. The technology sector witnessed $2 billion in outflows, the largest in 10 weeks, as investors reacted to Federal Reserve Chair Jerome Powell's indication of possible interest rate increases. Despite the Nasdaq 100 Index's strong performance this year, Bank of America's Michael Hartnett warned of potential declines ahead, suggesting a higher chance of downside than upside this summer. Other strategists, including Chris Harvey of Wells Fargo Securities and Marko Kolanovic of JPMorgan Chase, have also expressed concerns about the market resembling the tech boom of the late-1990s and predict a turbulent second half of the year.

Bonds, on the other hand, rallied as investors speculated that excessive tightening would lead to economic downturns, leading to purchases in longer-dated bonds. They believe that central banks' efforts to control inflation will lead to stable returns on US debt. Despite the Federal Reserve's interest rate hikes, 10-year Treasury yields have actually fallen this year. However, there is a risk that inflation may persist, resulting in higher borrowing costs for a longer period. Analysts predict a decline in the 10-year US yield by year-end. Traders in forwards markets have adjusted their bets, reflecting confidence in central banks' inflation-fighting measures. The US dollar and gold futures rose last week, while Bitcoin experienced a rally.

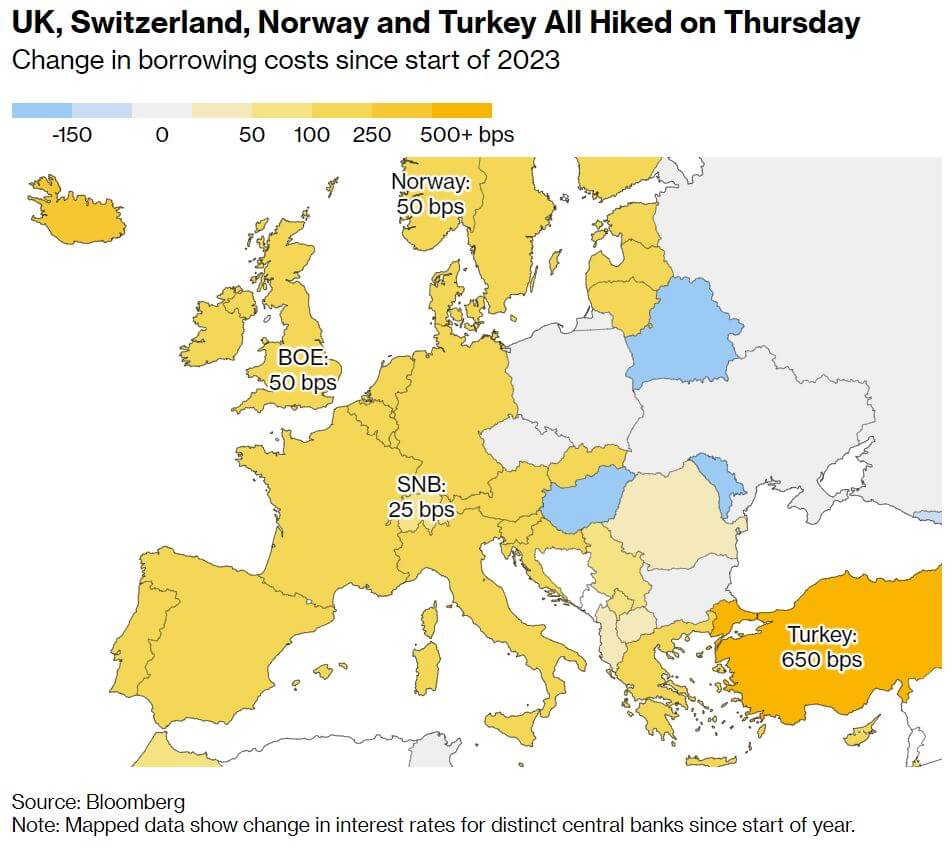

Central bankers around the world are intensifying their efforts to combat persistent inflation, leading to a new phase of monetary tightening. The Bank of England, the Norwegian central bank and the Swiss National Bank all raised interest rates by 0.5% in response to inflation concerns. This comes after Fed Chair Powell's warning of further rate increases. The tightening measures indicate a growing global alarm over inflation and suggest a prolonged period of economic uncertainty due to escalating borrowing costs. Turkey is cited as an example of the need for aggressive monetary action, as it experiences rampant inflation of nearly 40%. The UK also faces significant inflationary pressures, with consumer-price gains above 8%. Bank of England Governor Andrew Bailey emphasized the necessity of raising rates despite the challenges it poses for borrowers. The UK's decision to double the pace of rate hikes was unexpected but justified by the recent surge in inflation. This move, along with actions taken by other central banks, reflects a series of global monetary policy shifts in response to inflation concerns. The European Central Bank and the Norwegian central bank have also projected future rate increases, and the Swiss National Bank has indicated that more rate hikes may be necessary. The market response to these measures has been mixed, as the Turkish lira declined and Turkish dollar bonds experienced losses. In contrast, the Swiss National Bank's quarter-point rate increase was viewed as cautious, but officials noted the possibility of additional hikes. The ongoing concern over inflation and the need for further tightening measures suggest a challenging economic outlook in the coming months.

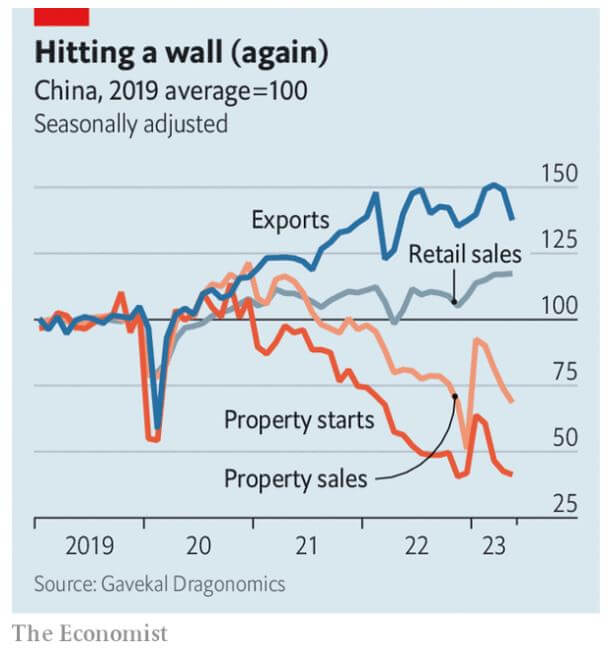

The Chinese economy grew faster than expected due to a sudden easing of COVID-19 restrictions earlier this year, but in April and May it experienced slower-than-anticipated recovery. Retail sales, investment and property sales all fell short of expectations, with the unemployment rate among urban youth reaching a record high. Some experts now believe that China's economy may not grow at all in the second quarter. The slowdown in China's economy can be attributed in large part to its property market, which initially showed signs of recovery but has since faltered. The price of new homes has fallen, property sales have declined and housing starts are significantly lower than before. The Chinese government has responded to these challenges by taking measures to stimulate the economy. The People's Bank of China asked major lenders to lower their deposit rates, paving the way for a reduction in the policy rate. Further interest rate cuts and relaxation of restrictions on home purchases in certain cities are expected. Policy banks may provide more loans for infrastructure projects and local governments may be allowed to issue more bonds, though they are already heavily indebted. Some economists are optimistic that the government's measures will be sufficient to meet the growth target, expecting a rebound in employment and increased consumer spending. However, others are less hopeful, suggesting that further monetary easing may not be effective given the limited demand for loans from property developers. If monetary easing proves inadequate, fiscal stimulus may be necessary. China's fiscal authorities, however, tend to prioritize durable assets over short-term handouts, which may limit the scope of fiscal measures in booting consumer spending. It may be difficult for China to reboot its economic growth, given battered consumer confidence and a slowing export market.