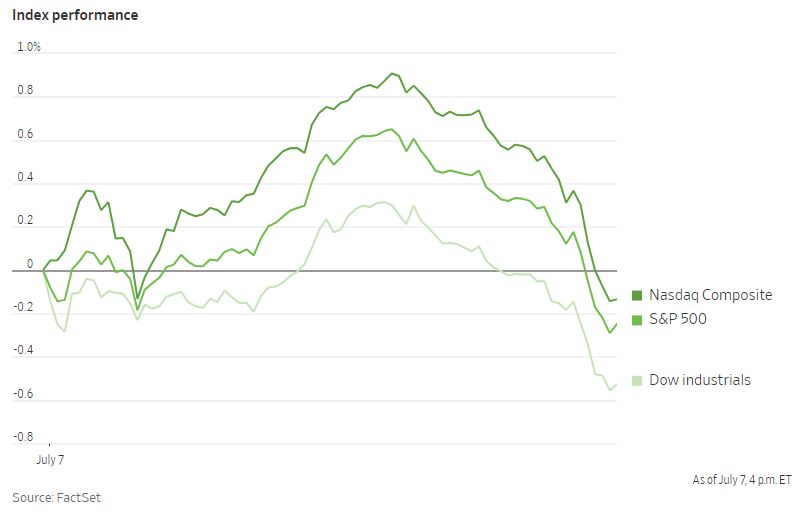

In thin afternoon trading Friday, US stocks reduced their gains, while Treasuries and the dollar experienced fluctuations following the release of June hiring data. The S&P 500 traded lower than its session highs and the dollar was on track for its biggest one-day drop since February 1. Notable stock movements included Levi Strauss & Co. falling due to a lowered outlook, and Rivian Automotive Inc., an electric-vehicle manufacturer, climbing for the eighth consecutive session. Stock markets have been declining in July, driven by hawkishness from central banks which has dampened hopes of a smooth global economic recovery. Bank of America Corp. strategists warned that investors who heavily invested in the technology sector risk being caught off guard by the selloff caused by rate hikes. Oil prices recorded a second consecutive weekly gain as evidence showed that the decision by OPEC+ leaders to reduce oil supplies was having an impact on physical markets. West Texas Intermediate (WTI) settled near $74, reaching its highest level in over a month, supported by positive market sentiment. This marked the first back-to-back weekly increase in crude prices since May, with near-term time spreads exhibiting a bullish pricing pattern by flipping into a narrow backward-dated structure. Although crude prices are still down around 10% for the year, factors such as tighter monetary policy, China's slow economic recovery and resilient Russian exports have put pressure on oil futures. Despite a broader decline in other risk assets, oil prices rose this week due to robust US jobs data, which reinforced expectations of the Federal Reserve continuing to raise interest rates.

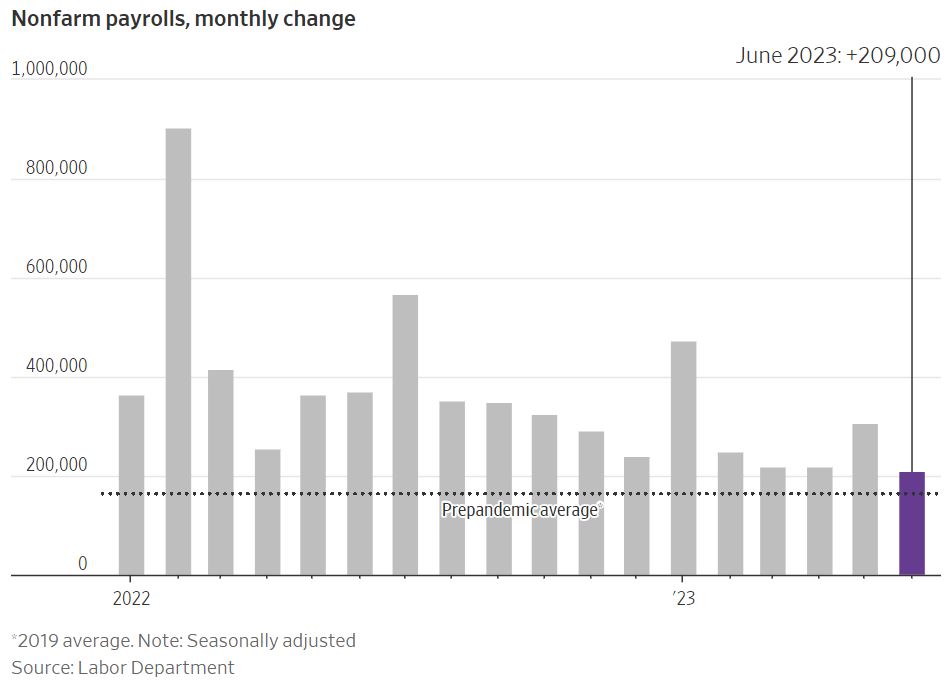

Hiring in the United States experienced a slowdown In June, with employers adding 209,000 workers compared to May's revised figure of 306,000. Despite the decrease, this remains a solid monthly gain. Despite the moderation in hiring, wages have continued to rise as employers compete for a limited pool of workers. Average hourly earnings grew by 4.4% in June compared to the previous year, maintaining a robust pace above the levels seen before the pandemic. The decline in unemployment also contributed to the wage growth trend, as the unemployment rate dropped from 3.7% in May to 3.6% in June. Various industries have contributed to job growth, with healthcare, construction and government sectors adding jobs in June. However, the leisure and hospitality sector experienced a slower pace of hiring, while retailers cut jobs. These patterns reflect a continuation of the overall positive trend in job creation, which has been sustained for the past two and a half years. However, there are signs of cooling in certain areas of the labor market. The number of people working part-time due to the unavailability of full-time work increased by almost half a million in June. Additionally, the labor force participation rate, which measures the proportion of Americans actively seeking employment, remains below pre-pandemic levels due to the aging population, leading to ongoing labor shortages. The latest employment and wage data suggests that economic activity has not slowed down as much as anticipated by Federal Reserve officials. As a result, it is highly likely that interest rates will be raised to their highest level in 22 years during the Federal Reserve's upcoming meeting on July 25-26.

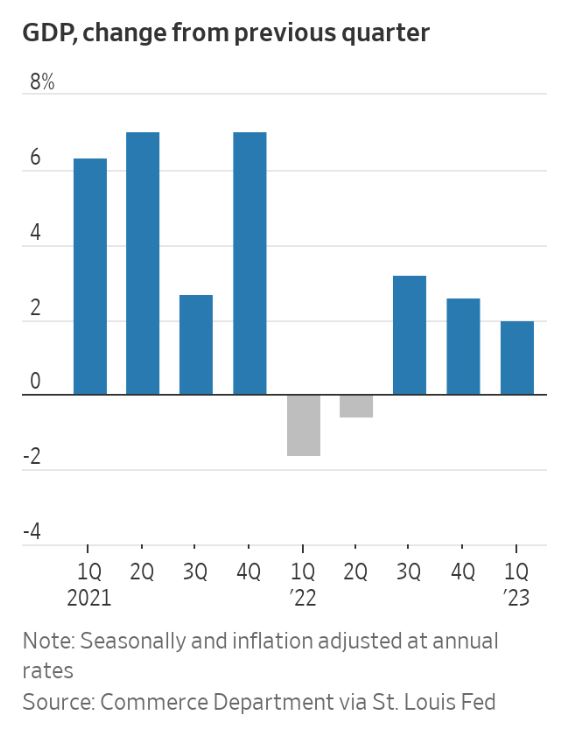

Recent data releases in the US have shown surprising strength in various sectors of the economy, signaling resilience and dispelling immediate concerns of an impending recession, despite rising interest rates. Reports on new home purchases, durable goods orders and consumer confidence all revealed positive trends. The housing market has flourished despite historically low inventory levels of existing homes. Government data revealed a 12.2% increase in purchases of new single-family homes, marking the third consecutive monthly advance and surpassing economists' estimates. Americans have increased their spending on durable goods such as cars and services like healthcare and dining out. June also saw an increase in consumer confidence, driven by greater optimism about the labor market and the overall economic expansion. The Commerce Department also revised the first-quarter GDP growth rate up to 2% from 1.3%, attributing the upward revision to stronger consumer spending. S&P Global Market Intelligence now predicts a 1.7% annual growth rate for the second quarter, a significant increase from its previous estimate of 0.8%. Economists and market analysts have taken note of this robust data, indicating that while a recession in the coming year cannot be completely ruled out, the current economic indicators suggest that a downturn is not imminent. As a result, most Fed officials are projecting two more interest rate hikes for this year. The Fed has been actively raising rates to combat inflation and cool down the economy, but it decided to leave rates unchanged at its most recent meeting. Consumer prices and spending in the United States experienced slower growth in May, indicating a possible deceleration in economic activity. According to the Commerce Department, the personal-consumption expenditures price index, the Fed's preferred measure of inflation, increased by 3.8% compared to the previous year, marking its lowest reading in two years. The rise in consumer prices, excluding volatile food and energy categories, was slightly lower in May at 4.6% compared to the previous year. Economists consider this core inflation measure a more reliable predictor of future inflation than overall inflation.