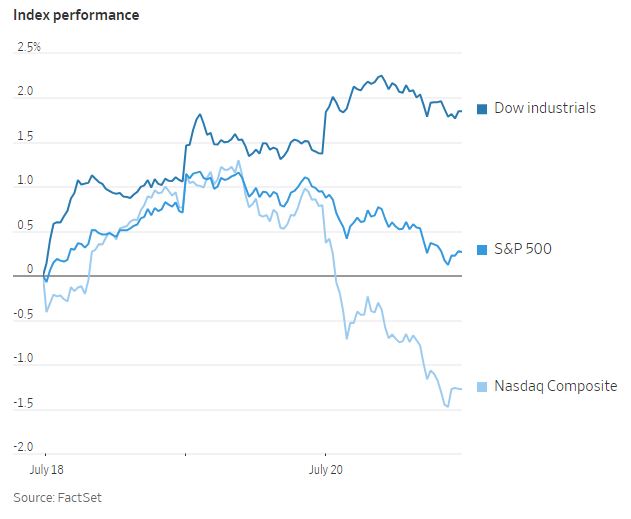

The Dow Jones Industrial Average extended its winning streak for the ninth consecutive session, displaying a notable 0.5% increase on Friday, the longest such streak since September 2017. Conversely, the S&P 500 dropped 0.7% and the tech-heavy Nasdaq Composite saw a more substantial pullback of 2.1%. The discrepancy in performance was influenced by a post-earnings selloff in Tesla shares which had a significant impact on the S&P 500 and Nasdaq's performance due to their market cap-weighted structure. The broader stock-market rally in 2023 has shown signs of diversification recently, but a considerable portion of this year's gains still rely on a small group of major tech companies, including Tesla. Such concentration poses a risk to the major indexes since the overall market could be vulnerable to a pullback if any of these heavyweights stumble. Netflix, another prominent tech-focused stock, slid 8.4% following its report of revenue falling short of its own projections. The PHLX Semiconductor Sector Index dropped by more than 3%, with U.S.-listed shares of Taiwan Semiconductor declining by 5%, while Intel and Nvidia both experienced a 3% decline.

Conversely, Johnson & Johnson experienced a surge of 6.1% after reporting better-than-expected earnings and raising its guidance. The stock's impressive performance significantly contributed to the healthcare sector of the S&P 500 and had a positive impact on the Dow by adding over 60 points to the index. The recent market dynamics have shifted toward a more fundamental approach, moving away from relying solely on sentiment. Investors are now anticipating the upcoming earnings reports from major tech companies in the U.S., such as Alphabet, Microsoft and Meta Platforms, which are expected to have significant implications for the market. Lastly, the benchmark 10-year U.S. Treasury note experienced a notable increase in yield, rising to 3.853% from 3.741% the previous day, making it the largest one-day yield increase of the month.

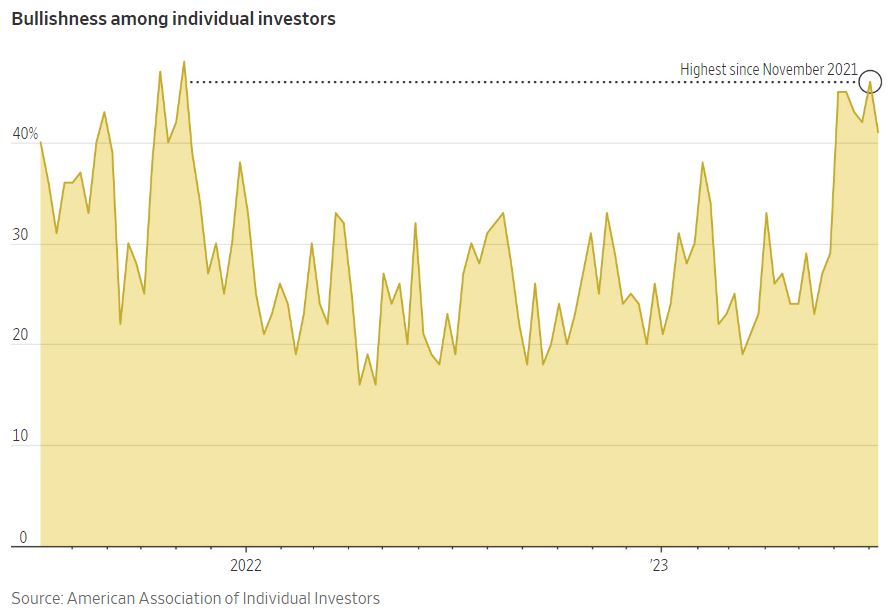

In 2023, the investment landscape appears to have disregarded the events of the previous year. There is a significant surge in risk-on investments, particularly in tech stocks and meme stocks. Speculative stocks are soaring, with the MEME ETF, tied to the Solactive Roundhill Meme Stock Index, rising 61% this year. Bitcoin has also defied expectations by climbing 80% in 2023. Retail traders are displaying heightened enthusiasm as bullish sentiment reaches its highest level since 2021. The bull-bear spread, indicating the difference between investors anticipating a market rise versus a decline, has been positive for six consecutive weeks, the longest streak since November 2021. Consumer confidence in the overall economy is growing, with sentiment surging to its highest level since September 2021. Notably, fear among investors seems to have dissipated as they are increasingly opting for bets that would benefit from further market rallies rather than seeking protection against potential downturns. This shift is reflected in the falling put-call ratio and the low Cboe Volatility Index (VIX), which measures options prices related to market declines.

Despite the current exuberance, some market contrarians warn of a brewing perfect storm that could lead to a crash. Drawing parallels to the euphoria seen in late 2021, they caution against complacency, emphasizing that even seemingly small factors can trigger significant downturns. Higher borrowing costs are also posing a threat to the economy. Increased rates on auto loans, mortgage, and credit cards could slow down economic growth and create challenges for businesses and households seeking loans. Furthermore, while inflation has eased slightly, it remains above the Federal Reserve's target rate, raising concerns about the potential impacts of prolonged elevated inflation. Given these factors, some experts are cautious about the sustainability of the current stock market rally and recommend monitoring potential risks closely.

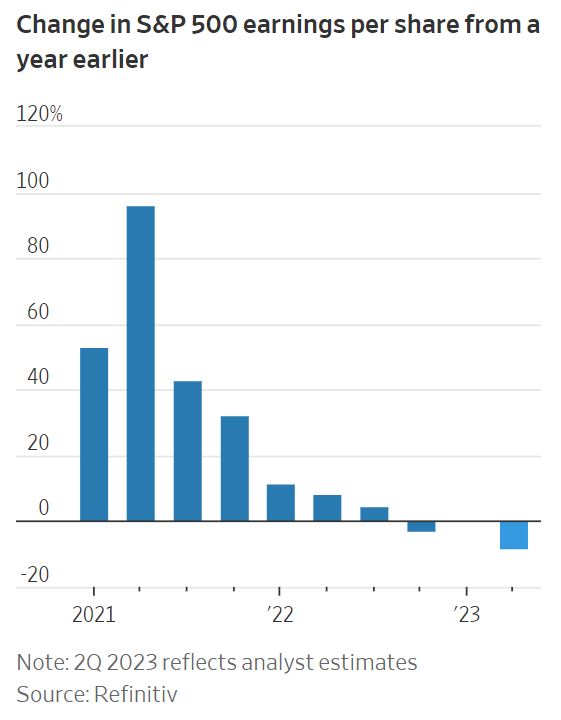

As the second-quarter results are being reported, it appears that this earnings season will be notably challenging, with estimates indicating a potential 8.1% decline in earnings per share for S&P 500 companies compared to the previous year. Although actual outcomes may not be as severe due to overly pessimistic estimates, a decline is still expected, with S&P 500 net income estimated to have fallen by 11.4%. Revenues have also experienced a decline, albeit less substantial at 0.9%, signaling a potential contraction in profit margins. The decline in revenues may be partially attributed to the energy sector, where fuel prices have significantly decreased. However, when excluding energy companies, S&P 500 revenues are expected to show only a modest 2.8% increase. A broader issue lies in the stock market's focus on goods-producing companies, while consumers redirect their spending towards services. Furthermore, goods inflation, apart from energy-related items, has decreased significantly, with consumer spending on goods rising by approximately 4%, while spending on services is projected to increase by around 8%. To address flagging sales, companies often seek to reduce costs, especially labor costs. While some have attempted layoffs, the tight labor market presents challenges, as many workers are now in high demand. This competition for labor with service providers has led to upward pressure on wages.

Another response to rising costs is raising prices, but for goods-oriented companies this proves challenging as customer spending moderates and competition intensifies due to steadier supply chains. Notably, makers of branded consumer staples, which initially benefited during the pandemic, are facing increased competition from private-label offerings as supply-chain issues ease. As the second quarter earnings season progresses, approximately 15% of S&P 500 companies have reported their results. Among them, 74% have exceeded analysts' consensus earnings estimates, which is slightly below the five-year average of 77%.